Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Robert Brenner: The Trajectory of the US Economy

NEW BOOM OR NEW BUBBLE?

The Trajectory

of the US Economy

By Robert Brenner

First Published - New Left Review 25 - Jan Feb 2004 [1]

Distributed by email on the Scoop Eco-Economy list

In early 2002 Alan Greenspan declared that the American recession which had begun a year earlier was at an end. By the fall the Fed was obliged to backtrack, admitting that the economy was still in difficulties and deflation a threat. In June 2003 Greenspan was still conceding that the ‘the economy has yet to exhibit sustainable growth’. Since then Wall Street economists have been proclaiming, with ever fewer qualifications, that after various interruptions attributable to ‘external shocks’ - 9/11, corporate scandals and the attack on Iraq - the economy is finally accelerating. Pointing to the reality of faster growth of gdp in the second half of 2003, and a significant increase in profits, they assure US that a new boom has arrived. The question that therefore imposes itself, with a Presidential election less than a year away, is the real condition of the US economy.[1]

What triggered the slowdown that took place? What is driving the current economic acceleration, and is it sustainable? Has the economy finally broken beyond the long downturn, which has brought ever worse global performance decade by decade since 1973? What is the outlook going forward?

******* notes *******

1 I wish to thank Aaron Brenner and Tom Mertes for much help on both content and style. I am also grateful to Andrew Glyn for data on inventories for Germany and Japan and Dean Baker for very useful advice on data sources.*********

In mid-summer 2000, the US stock market began a sharp descent and the underlying economy rapidly lost steam, falling into recession by early 2001. [2] Every previous cyclical downturn of the post-war period had been detonated by a tightening of credit on the part of the Federal Reserve, to contain inflation and economic overheating by reducing consumer demand and, in turn, expenditure on investment. But in this case, uniquely, the Fed dramatically eased credit, yet two closely interrelated forces drove the economy downward. The first of these was worsening over-capacity, mainly in manufacturing, which depressed prices and capacity utilization, leading to falling profitability - which in turn reduced employment, cut investment and repressed wage increase. The second was a collapse of equity prices, especially in high technology lines, which sent the ‘wealth effect’ into reverse, making it harder for corporations to raise money by issuing shares or incurring bank debt, and for households to borrow against stock.

i. the end of the boom

The recession brought an end to the decade-long expansion that began in 1991 and, in particular, the five-year economic acceleration that began in 1995. That boom was, and continues to be, much hyped, especially as the scene of an ostensible productivity growth miracle. [3] In fact, it brought no break from the long downturn that has plagued the world economy since 1973. Above all, in the us, as well as Japan and Germany, the rates of profit in the private economy as a whole failed to revive. The rates for the 1990s business cycle failed to surpass those of the 1970s and 1980s, which were of course well below those of the long post-war boom between the end of the 1940s and end of the 1960s. As a consequence, the economic performance during the 1990s of the advanced capitalist economies taken together (g7), in terms of the standard macro economic indicators, was no better than that of the 1980s, which was in turn less good than that of the 1970s, which itself could not compare to the booming 1950s and 1960s. [4]

******* notes *******

2 The National Bureau of Economic Research declared a recession to have begun in February 2001 and to have ended in November 2001. In this text, I use the term recession only in the formal sense of the nber. Otherwise, I generally speak of slowdown, to refer to the economic slackening that was set off by developments in the second half of 2000 and continued till mid-2003, at least.3 Typical in this respect is Joseph Stiglitz, ‘The Roaring Nineties’, The Atlantic Monthly, October 2002. Despite his self-described role of critic of the bubble economy, this much-admired Nobel Prize winning economist is in fact exemplary of the Wall Street publicity machine in refusing to be moved by mere numbers. As chair of the Council of Economic Advisers, he would appear to have been well placed to discover basic government data on the economy. But he states, preposterously, that ‘the height of the 1990s boom’ was ‘a period of unprecedented growth’ with ‘productivity levels that exceeded even those of the boom following World War ii’. In reality, in terms of all the standard economic variables, economic performance in the half decade 1995–2000 was less good than in the entire quarter century 1948–73. The average annual rate of labour productivity growth in the non-farm business economy for 1995–2000, at 2.5 per cent, was well below that for 1948–73, at 2.9 per cent. ‘Multifactor Productivity Trends, 2001’, bls News, 8 April 2003, p. 6, Table b (available on the bls website). See also The Boom and the Bubble, London 2002, p. 221, Table 9.1.

4 See The Boom and the Bubble, p. 47, Table 1.10.

*********

What continued to repress private sector profitability and prevent any durable economic boom was the perpetuation of a long-term international - that is, systemic - problem of over-capacity in the manufacturing sector. This found expression in the deep dip of - already much reduced - manufacturing profitability in both Germany and Japan during the 1990s, and in the inability of US manufacturers to sustain the impressive recovery in their rates of profit between 1985 and 1995 much past mid-decade. It was manifested too in the series of increasingly deep and pervasive crises that struck the world economy in the last decade of the century - Europe’s erm collapse in 1993, the Mexican shocks of 1994–95, the East Asian emergency of 1997–98, and the crash and recession of 2000–2001.

The roots of the slowdown, and more generally the configuration of the us economy today, go back to the mid-1990s, when the main forces shaping the economy of both the boom of 1995–2000 and the slowdown of 2000–2003 were unleashed. During the previous decade, helped out by huge revaluations of the yen and the mark imposed by the US government on its Japanese and German rivals at the time of the 1985 Plaza Accord, US manufacturing profitability had made a significant recovery, after a long period in the doldrums, increasing by a full 70 per cent between 1985 and 1995. With the rate of profit outside of manufacturing actually falling slightly in this period, this rise in the manufacturing profit rate brought about, on its own, a quite major increase in profitability for the US private economy as a whole, lifting the non-financial corporate profit rate by 20 percent over the course of the decade, and to its level of 1973 for the first time since 1969. On the basis of this revival, the US economy began to accelerate from about 1993, exhibiting, at least on the surface, greater dynamism than it had in many years.

Nevertheless, the prospects for the American economy were ultimately limited by the condition of the world economy as a whole. The recovery of US profitability was based not only on dollar devaluation, but a decade of close to zero real wage growth, serious industrial shake-out, declining real interest rates, and a turn to balanced budgets. It therefore came very much at the expense of its major rivals, who were hard hit both by the slowed growth of the US market and the improved price competitiveness of US firms in the global economy. It led, during the first half of the 1990s, to the deepest recessions of the post-war epoch in both Japan and Germany, rooted in manufacturing crises in both countries. In 1995, as the Japanese manufacturing sector threatened to freeze up when the exchange rate of the yen rose to 79 to the dollar, the US was obliged to return the favour bestowed upon it a decade earlier by Japan and Germany, agreeing to trigger, in coordination with its partners, a new rise of the dollar. It cannot be overstressed that with the precipitous ascent of the dollar that ensued between 1995 and 2001 the US economy was deprived of the main motor that had been responsible for its impressive turnaround during the previous decade - viz. the sharp improvement in its manufacturing profitability, international competitiveness, and export performance. In so doing, it set stage for the dual trends that would shape the American economy throughout the rest of the decade and right up to this day. The first of these was the deepening crisis of the US manufacturing sector, of exports, and (after 2000) of investment; the second was the uninterrupted growth of private sector debt, household consumption, imports, and asset prices, which would make for the sustained expansion of a significant portion of the non-manufacturing sector - above all finance, but also such debt-, import-, and consumptiondependent industries as construction, retail trade, and health services.

Stock market Keynesianism

As the dollar skyrocketed after 1995, the burden of international overcapacity shifted to the US. Matters were made much worse for us manufacturers when the East Asian economies entered into crisis in 1997–98, leading to the drying up of East Asian demand, the devaluation of East Asian currencies, and East Asian distress selling on the world market. From 1997, the US manufacturing profit rate entered a major new decline. Yet, even as manufacturing profitability fell, the us stock market took off. It was initially driven upward by a precipitous decline of long term interest rates from 1995, which resulted from a huge influx of money from East Asian governments into US financial markets, pushing up the dollar. It was systematically sustained to the end of the decade by the loose money regime of Alan Greenspan at the Fed, who refused to raise interest rates between early 1995 and mid 1999 and came vigorously to the aid of the equity markets with injections of credit at every sign of financial instability. Greenspan was acutely conscious of the depressive impact on the economy of both Clinton’s moves to balance the budget and the new take-off of the dollar. He therefore looked to the wealth effect of the stock market to offset these by jacking up corporate and household borrowing and thereby investment and consumer demand. In effect, the Federal Reserve replaced the increase in the public deficit that was so indispensable to US economic growth during the 1980s, by an increase in the private deficit during the second half of the 1990s, a kind of ‘stock market Keynesianism’. [5]

******* notes *******

[5] Greenspan’s deliberate reliance on the wealth effect of the stock market can be seen in his public statements of the period, especially his testimonies before the Joint Economic Committee of Congress in June and July 1998.*********

Once equity prices took off, corporations - especially in information technology - found themselves with unprecedentedly easy access to finance, either through borrowing against the collateral ostensibly represented by their stock market capitalization or the issuance of shares. As a consequence, the indebtedness of non-financial corporations skyrocketed, approaching record levels by the end of the decade. Whereas throughout the post-war epoch, corporations had financed themselves almost entirely out of retained earnings (profits after interest and dividends), now firms that could not borrow cheaply turned to the equity market for funds to an extent that had been previously inconceivable. On these foundations, investment exploded upwards, increasing at an average annual rate of about 10 per cent and explaining, in growth accounting terms, about 30 per cent of the increase in gdp between 1995 and 2000.

Rich households also benefited from the wealth effect of runaway equity prices. As they saw their paper assets soar, they felt justified in raising their annual borrowing, as well as their debt outstanding, to near record levels as a fraction of household income. They also felt free to raise their household consumption as a proportion of personal income to near 100 per cent, bringing about a parallel reduction in the US household savings rate from 8 per cent to near zero over the course of the decade. [6]

******* notes *******

6 The top 20 per cent of families by income were entirely responsible for the fall in the household savings rate during the 1990s. See D. M. Maki and M. G. Palumbo, ‘Disentangling the Wealth Effect: A Cohort Analysis of Household saving in the 1990s,’ Federal Reserve Finance and Discussion Series, April 2001 (Federal Reserve website)*********

Consumer expenditures jumped sharply, helping mightily to soak up the increased output generated by rising investment and productivity. Between 1995 and 2000, a powerful boom took shape, marked by an acceleration of output, productivity, employment and, eventually, real wage growth. But this boom was almost entirely dependent upon a stock market run-up that had no basis in underlying returns to corporations.

Occurring as it did in the face of the downward trend in profitability - and made possible by increases in corporate borrowing and household consumption that were both dependent upon the stock market bubble - much of the growth in investment of the second half of the decade was inevitably misallocated. The scope and depth of over-capacity was thus very much extended, especially into high-technology industries both within and outside of the manufacturing sector, exacerbating the decline in profitability. Across the economy, the reductions in the growth of costs that resulted from increased productivity were more than offset by the deceleration of price increases that stemmed from the outrunning of demand by supply. Consumers thus ended up as the primary - if only temporary - beneficiaries of a self-undermining process that brought inexorably increasing downward pressure on profits. Between 1997 and 2000, as both the boom and the bubble reached their apogee, the non-financial sector as a whole sustained a fall in profit rate of almost one-fifth.

ii. crisis of manufacturing and hi-tech

But the ascent of neither the real economy nor its on-paper representation in the form of asset prices, could long defy the gravitational pull of falling returns. From July 2000, a series of ever-worsening corporate earning reports precipitated a sharp cyclical downturn, both by reversing the wealth effect and by revealing the mass of redundant productive capacity and mountain of corporate indebtedness that constituted the dual legacy of the bubble-driven investment boom. With their market capitalization sharply reduced, firms not only found it more difficult to borrow, but less attractive to do so, especially since declining profits and the growing threat of bankruptcy led them to try to repair balance sheets overburdened by debt. Having purchased far more plant, equipment, and software than they could profitably set in motion, they were obliged either to reduce prices or leave capacity unused, sustaining falling profit rates either way. To cope with declining profitability, firms cut back on output and capital expenditures, while reducing employment and wage growth so as to bring down costs. Across the economy these moves radically reduced aggregate demand, pushing the economy downward, while exacerbating profitability decline by depressing capacity utilization and productivity growth. The relentless burden of interest payments on the huge overhang of corporate debt compressed profits even further. Between the year ending in mid-2000 and the year ending in mid-2001, gdp growth fell from 5 per cent to minus 1 per cent per annum and investment from 9 per cent to minus 5 per cent - in both cases faster than at any other time since World War ii - sending the economy into a tail-spin.

In 2001, 2002, and the first half of 2003, employment in the non-farm economy (measured in hours and including the self-employed) fell by 2 per cent, 2.5 per cent, and 1.5 per cent respectively, after having increased at an average annual rate of more than 2 per cent between 1995 and 2000. This in itself entailed an enormous hit to aggregate demand, an inexorable and persistent downward pull on the economy. Simultaneously real hourly wages, which had grown 3.5 per cent in 2000, were brutally cut back - to minus 0.1 percent, 1.2 per cent, and 0.3 per cent, respectively, in 2001, 2002, and the first half of 2003. As a result of the combination of reduced hourly wage growth and falling employment, total real non-farm compensation - the main element of aggregate demand - fell by 1.2 per cent, 1.4 per cent, and 0.2 per cent, respectively, in 2001, 2002, and the first half of 2003, after increasing at an average annual pace of 4.3 per cent between 1995 and 2000. Perhaps most striking of all, after having grown at an average annual rate of 10 per cent between 1995 and 2000, real expenditures on plant and equipment fell sharply in 2001 and 2002, and were flat in the first half of 2003. All else being equal, these huge blows to consumer and investment demand, resulting from the mammoth reductions in employment, compensation, and capital spending growth, would have kept the economy in, or near recession, right into the present. As it was, even in the face of the government’s enormous stimulus programme, they were responsible for driving average annual growth of non-farm gdp from 4.6 per cent between 1995 and 2000 to minus 0.1 per cent in 2001 and preventing it from going higher than 2.7 per cent in 2002 and 2.6 per cent in the first half of 2003.

Exacerbating the downturn, US overseas sales also plummeted. Over the previous two decades the growth of US exports had tended to depend, paradoxically, on the increase of US imports. This is because they relied upon a world economy whose increasingly export-dependent growth had itself become ever more reliant upon the growth of US imports. The stock market’s last upward thrust in the final couple of years of the century had rescued the world economy, as well as US exports, from the East Asian crisis by setting off a short lived import boom, especially in information technology components. But with US equity prices and investment collapsing, especially again in ‘new economy’ sectors, the process was reversed. Japan, Europe, and East Asia now lost steam as fast as the us, while much of the developing world, notably Latin America, was plunged, after a brief honeymoon, back into crisis. Because the economies of the us’s trading partners had become so dependent on sales to the US - and because the US possesses a far greater propensity to import than does either the EU or Japan - the descent into recession reduced the capacity of the rest of the world to absorb us imports more than vice versa. In 2001, 2002, and the first half of 2003, us export growth therefore fell even further behind US import growth than previously. US real imports, after having increased by 13.2 per cent in 2000, dropped by 2.9 per cent in 2001, then grew by 3.7 per cent and 2.25 respectively, in 2002 and the first half of 2003. US real exports, on the other hand, after growing by 9.7 per cent in 2000, fell by 5.4 per cent, 3.6 per cent, and 0.1 per cent in 2001, 2002 and the first half of 2003. As the rest of the world, deprived of the American motor, slowed down, the US could look only to itself to launch an economic recovery upon which the whole global economy depended.

To stem the plunge, from January 2001 onwards the Federal Reserve lowered the cost of borrowing with unprecedented rapidity, reducing short-term interest rates on eleven occasions, from 6.5 per cent to 1.75 per cent, over the course of the year. But, as the Fed discovered, interest- rate reductions are much more effective in reviving an economy in which consumption has been restricted by a tightening of credit - as in all previous post-war cyclical downturns - than in re-starting an economy driven into recession by declining investment and employment resulting from over-capacity, making for falling rates of profit.

Vastly over-supplied with plant and equipment, non-financial corporations had little incentive to step up capital accumulation, no matter how far interest rates were brought down by the Fed. On the contrary, having increased their indebtedness from 73 to 90 per cent of their gdp between 1995 and 2000, they had every motivation to restore their balance sheets by trying to save more, and their so doing made it that much more difficult for them to invest. Whereas vastly increased apparent wealth derived from market capitalization allowed non-financial corporations to raise their borrowing as a proportion of their income to a near record 8 per cent for 1998, 1999, and 2000 taken together, they were obliged sharply to reduce it to 4.6 per cent, 2.1 per cent, and 2.6 per cent, in 2001, 2002 and the first half of 2003, as the value of their stock dramatically contracted. Real non-residential expenditures on plant and equipment thus fell like a stone, declining from an average annual rate of 10.1 per cent between 1995 and 2000 to an average annual rate of minus 4.4 per cent between 2000 and the middle of 2003. It has been the failure of investment to revive that has constituted the ultimate factor holding back the economy.

Manufacturing crisis

The manufacturing sector was the main, almost exclusive, site and source of the economic slowdown, as developments maturing over the previous half-decade came to fruition. Although by the middle 1990s this sector had come to constitute only 29.3 per cent and 32.7 per cent, respectively, of corporate and non-financial GDP, as late as 1995, manufacturing still accounted for 42.5 and 50 per cent, respectively, of corporate and non-financial corporate profits (before payment of interest). As a consequence, manufacturing’s descent into crisis meant crisis for the whole economy.

Between 1995 and 2000, the growth of costs in the US manufacturing economy posed no threat to profitability. On the contrary: productivity growth in manufacturing grew so rapidly that it more than cancelled out the rise of wages, with the result that unit labour costs fell at an impressive average annual rate of more than 1 per cent a year over the quinquennium. Even so, US producers found it vastly more difficult to defend, let alone expand, their markets and profit margins during this period, because they had to face an appreciation of the dollar in tradeweighted terms of 21 per cent and, from 1997, crisis conditions on the world market. World export prices, measured in dollars, fell at the stunning rate of 4 per cent per annum over the half decade, with the consequence that, while US manufacturing exports increased at an average annual rate of 7 per cent a year, manufacturing imports rose 40 per cent faster, at 10 per cent per annum, and their share of the US market jumped by a third. Despite falling production costs, price pressure was therefore so intense that the manufacturing sector maintained its rates of profit only between 1995 and 1997, and then simply because wage pressure was so weak in those two years, real wages falling by 1.5 per cent. Between 1997 and 2000, prices fell even more than did unit labour costs, with the result that, in that short period, as the economy bubbled over, the manufacturing rate of profit fell by 15 per cent.

In 2001 the crisis in manufacturing reached a climax, as competitive pressures from the world market intensified and were vastly complicated by the slowdown of the domestic market. As world manufacturing prices dropped by a further 2.4 per cent and US manufacturing exports (nominal) fell by 7 per cent, American manufacturers saw growth in real domestic consumption cut by half. In the face of these contractions, us manufacturing gdp dropped by a staggering 6 per cent and capacity utilization declined by 7.1 per cent. Meanwhile, real manufacturing investment fell by 5.4 per cent. With output and capacity utilization, as well as expenditures on new plant, equipment, and software, falling off so rapidly, there was no way employers could reduce the labour force fast enough to prevent a huge fall in productivity growth. Employment (measured in hours) was in fact cut back by 4.8 per cent. But the growth of output per hour in manufacturing still plunged from 6.1 per cent in 2000 to minus 0.4 per cent in 2001.

Manufacturing firms responded to these excruciating pressures by battening down employees’ compensation: real wages, which had grown 3.9 per cent in 2000, fell 1.2 per cent in 2001. But with productivity as well as capacity utilization diving, employers still could not prevent unit labour costs from rising by 2 per cent. Nor could they stop domestic manufacturing prices from falling by 0.4 per cent, after a 2 per cent drop in 2000. The outcome was that in 2001 the rate of profit for the manufacturing sector fell a further 21.3 per cent, to a level over a third down from its 1997 peak. Between 1997 and 2001, as corporate indebtedness rocketed, manufacturing net interest as a proportion of manufacturing net profits rose from 19 per cent to 40.5 per cent, a post-war record. Partly as a consequence, by 2001 manufacturing profits net of interest had fallen a total of 44.4 per cent from their high point in 1997.

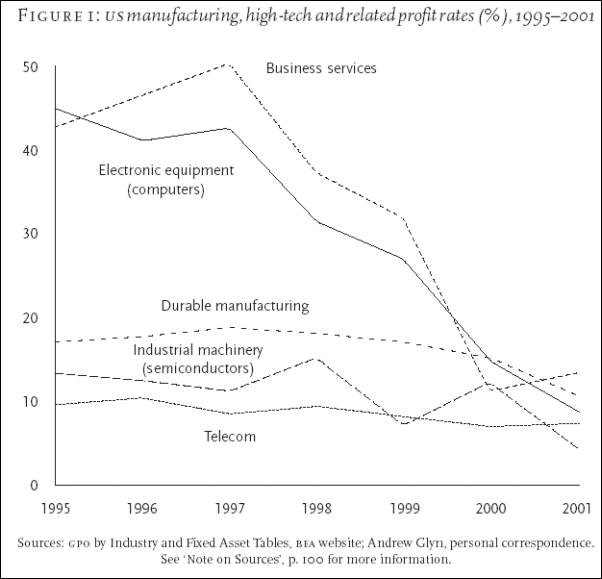

The profitability crisis struck all across manufacturing, including traditional industries from textiles to steel to leather. But the eye of the storm was the information technology sector, which is located for the most part in durable goods manufacturing, but includes a few industries outside manufacturing, most notably telecommunications. Business services, which cater largely to manufacturing corporations, were hard hit, too. The high- tech industries had been the main beneficiaries of the financial largesse generated by the stock market run-up, becoming the leading agents of over-investment, and, in turn, the main victims of over-capacity, falling profits, and over-burdened balance sheets. Many experienced huge falls in their profit rates. Even where their profit rates did not fall spectacularly, these industries generally experienced very major declines in their absolute profits after payment of interest, due to the huge cost of servicing the enormous debts that they had run up during the bubble. Between 1995 and 2001, profits excluding interest in electronic equipment (including computers) fell from $59.5 billion (1997) to $12.2 billion, in industrial equipment (including semi-conductors) from $13.3 billion to $2.9 billion, in telecommunications from $24.2 billion (1996) to $6.8 billion, and in business services from $76.2 billion (1997) to $33.5 billion.

Click for big version

The decline in manufacturing profitability was by itself responsible for the entire fall in the rate of profit for the non-financial corporate sector as a whole in 2001. That is, the non-financial corporate sector with manufacturing left out managed to avoid any fall in the rate of profit in 2001. [7]

As it was, the profitability crisis in manufacturing was severe enough in 2001 to inflict a 10 per cent fall in the rate of profit on the non-financial corporate sector as a whole. By 2001, the non-financial corporate profit rate, having already experienced a 19 per cent decline between 1997 and 2000, had fallen by a total of 27 per cent from its 1997 peak.

It is from the manufacturing sector, and related industries, that the most powerful downward pressures on the economy have continued to emanate, as manufacturing employers have cut back mercilessly in order to restore profits. In 2002 and the first half of 2003, they reduced output by 0.4 per cent and 2.8 per cent, respectively, [8] and brought down investment quite a bit faster, at an average annual rate of 5 per cent or more. [9] Above all, they radically reduced employment. Between July 2000 and October 2003, employers eliminated 2.8 million jobs in the manufacturing sector. This was well over 100 per cent of the total of 2.45 million private sector jobs lost in the same period - meaning that the economy outside manufacturing actually gained jobs in this period. Since its most recent peak in 1997 peak, the manufacturing sector has lost one-fifth of its labour force. Largely as a consequence, after having increased at an average annual rate of 3.8 per cent between 1995 and 2000, total compensation in manufacturing fell at the annual average rate of 3.1 per cent between the end of 2000 and the middle of 2003, thereby accounting, once again, for most of the decline in real total compensation that took place in the non-farm economy during that period. By way of its continual, powerful restraining effect on the growth of effective demand, the crisis of investment and employment has been the main depressive factor in the overall economy since the slowdown began in the latter part of 2000 - and the collapse of investment and employment in the manufacturing sector has been largely behind that crisis.

******* notes *******

7 Parts of the non-manufacturing, non-financial corporate sector also experienced intense profitability problems, including telecommunications, business services, and the airline industry; but their losses were offset by gains of other industries.8 These figures are for gross output, not value added (gdp). They are therefore firstapproximations. The standard value-added numbers will not be made available bythe Bureau of Economic Analysis until next year.

9 This assumes that the fall in manufacturing investment was at least as great in the private economy as a whole. Figures for manufacturing investment for 2002 and 2003 are not yet available.

*********

iii. a distorted path of expansion

Through the middle of 2003, Greenspan’s historic interest rate reductions ran up against a wall of industrial over-capacity and corporate indebtedness, failing to stem the slowdown of investment, to stimulate corporate borrowing, or to impart new dynamism to manufacturing and related industries, especially in the form of job growth. The Fed therefore had no choice but to fall back on driving up consumption growth to keep the economy turning over. In this it has to a significant degree succeeded, with the consequence that the economy has ended up following a paradoxical two-track trajectory. Manufacturing and related industries have continued a profound contraction whose origins go back to 1995, and lie in ongoing global over-capacity, intensifying overseas competition, and a long overvalued dollar. But major parts of the of the non-manufacturing sector have, by contrast, succeeded in sustaining an expansion that also originated in the mid-1990s, due to the perpetuation throughout the boom and right through the ensuing slowdown of broader trends and conditions dating back to that point - notably the ever easier availability of cheap credit, the continued blowing up of asset price bubbles, the impetuous and unending growth of debt, the creditdriven increase of consumer spending, and the dizzying rise of imports made cheap by the high dollar.

To some extent, Alan Greenspan’s reduced interest rates could directly foster borrowing, and thereby consumption. During economic slowdowns, households typically need to increase their borrowing in order to cover the loss of income that results from slowed wage growth and rising unemployment. But precisely because they face downward pressure on their incomes, households face inherent limits to their ability to increase the burden of debt they can take on. In 2001, due to layoffs and the holding down of wages, total real compensation of all workers, including those working for the government, fell by 1.7 per cent compared to the final quarter of 2000; it dropped another 0.1 per cent in 2002; and it rose by only 0.4 per cent in the first half of 2003. The intent of the Fed has been to overcome the limitations of such stagnant incomes by reviving - or perhaps more precisely continuing - its strategy of the 1990s, namely to stimulate the economy by relying on wealth effects.

Once more Greenspan has thus sought to push up asset prices, inflating paper wealth, in order to enhance the capacity to borrow and thereby to spend. But, in the wake of the deep fall of profitability from 1997 and of equity prices from the middle of 2000, as well as corporations’ preoccupation with reducing indebtedness by cutting back on borrowing, he has had to shift emphasis. The Fed is still attempting to boost the stock market to improve the financial condition of corporations and the business outlook more generally. But it has had to place its hopes for stimulating the economy primarily on driving down mortgage rates and pushing up housing prices, so as to pave the way for increased household borrowing and consumer spending (including investment in houses). In their own terms, these hopes have been spectacularly realized.

Thanks in part to the Fed’s actions, long-term interest rates fell significantly and housing prices rose precipitously. Between June 2000 and June 2003, the interest rate on 30 year fixed mortgages fell from 8.29 per cent to 5.23 per cent, a total of 37 per cent. In the same interval, housing prices rose by 7 cent per annum, extending and accentuating a trend that originated between 1995 and 2000, when they increased at an average annual rate of 5.1 per cent. [10]

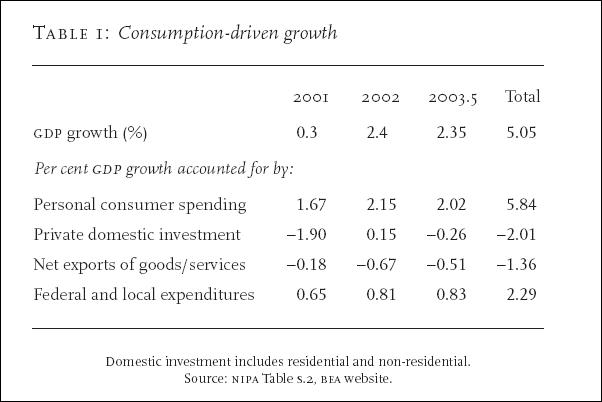

With their collateral sharply increased and their cost of borrowing radically reduced, households were able to ramp up their borrowing rapidly, even as the economy slowed down, hourly real wage growth declined, and unemployment rose. Already between 1998 and 2000, household borrowing as a proportion of annual household income, averaging 7.5 per cent, was approaching the historic highs reached in the mid-1980s. Starting in 2001, it climbed steeply, and during the first half of 2003, smashed all records at close to 12 per cent. The growth of household debt accounted for 70 per cent of the total growth of private non-financial debt outstanding between 2000 and 2003. Almost all of the household borrowing in these years - 85 per cent - was by way of home mortgages made possible by housing price inflation and reduced interest rates; less than a mere 15 per cent through other forms of consumer credit, which evidently were held down by the stagnation of incomes. By taking advantage of the appreciation in the value of their homes, and the fall in borrowing costs, households have been able to ‘cash out’ huge sums from their home equity - by way of home sales, refinancing and second mortgages - and so to play to the hilt their assigned role of driving the economy by sustaining the growth of consumption. Between 2000 and the middle of 2003, the increase of real consumption expenditures reached 2.8 per cent per year, despite the fact that, as noted, total real compensation actually declined in the same period. The sustained growth of consumption, itself dependent upon the growth of household debt, was the determining factor behind increases in gdp from 2000 onwards - in limiting the precipitous descent of the economy in 2001, in stabilizing it in the winter of 2001–02, and in stimulating the growth that has taken place in the period since. In national accounting terms, the increase of personal consumption expenditures was responsible for almost all of the gdp increase that took place between 2000 and the second half of 2003. By itself, it accounted for 16 per cent more growth than actually took place in that period. Put another way, it not only offset, by itself, the substantial negative impact on gdp growth of falling investment and a widening trade deficit, but accounted in addition for about 50 per cent of the positive growth that took place. Having fallen to 0.3 per cent in 2001, gdp growth reached 2.4 per cent in 2002 and 2.3 per cent in the first half of 2003 (annualized).

Click for big version

The Fed is betting the bank that the growth of consumption will hold up long enough for corporations to work off their excess capacity, begin investing and hiring again, and allow the almighty consumer to take a rest. That’s what’s required to restore the economy to a semblance of health.

Fiscal stimulus

While the Fed implemented its monetary stimulus, the Bush administration added what looks like a major fiscal stimulus modelled after that of Ronald Reagan, forcing through Congress enormous cuts in taxation and major increases in military spending. But these measures are less potent than they look. The administration has thrown a few small bones to the mass of the population - cash grants to the states to help cover the cost of medicare, a reduction in taxes on married people, an increase in the tax credit for child care, and the moving forward in time of reductions in rates called for by the tax act of 2001. But all these measures taken together are worth only about $35 billion in 2003. They can give the economy a palpable temporary boost. But their impact on the $11 trillion economy is bound to be fleeting. The remaining tax reductions mainly decrease the levy on dividends and therefore benefit the very rich almost exclusively. Their effect will be much more to increase savings and the purchase of financial assets than to boost consumption, doing little to improve aggregate demand. The fact that tax cuts at the federal level will have the effect of reducing revenue to money-strapped state governments, forcing them to cut back on spending and in some cases to increase taxation, is likely to counteract much, though not all, of what stimulus they do impart.

In the wake of 9/11, the growth of military spending reached 6 per cent in 2001 and 10 per cent in 2002, and enabled the equities of the nation’s nine largest defence contractors to outperform the average firm listed on the s&p 500 index by 30 per cent in the year following the attack on the wtc and the Pentagon. [10]

Amounting to about 65 per cent and 80 per cent respectively of the total increases in Federal spending in these two years, defence spending has unquestionably helped to push the economy forward. Nevertheless, the growth of military expenditures was responsible for an increase in gdp of no more than 0.75 per cent in total during 2001 and 2002. [11]

******* notes *******

10 H. Wood, M. A. Walton, and A. Sonthalia, ‘Defense Budget Apt to Remain on Track’, Morgan Stanley Equity Research Aerospace and Defense, 16 December 2002; T. Bennett et al, ‘Global News, Valuations and Forecasts,’ ibidem, 12 November 2002.I wish to thank Aayush Sonthalia for making these available to me.11 In the second quarter of 2003, ballooning expenditures on the Iraq War lifted therate of (otherwise lagging) gdp growth significantly, but it seems doubtful whether these are sustainable.

*********

Of course, as the economy decelerated, the combination of huge tax breaks for the rich and giant increases in military spending sent the federal government once more deeply into the red. By 2000, thanks to the speculative boom, and huge capital gains from the appreciation of stocks, the federal budget had gone positive to the tune of $236 billion. In just two and a half years, however, it had fallen into negative territory by a whopping $450 billion. Since the economy was sputtering, Keynesian deficits were very much in order. But since so much of the motivation of the Administration’s package was political and military, rather than strictly economic, it is not surprising that the way in which it has plunged public finances from surplus to deficit has been minimally efficient as a stimulus to economic growth.

Due to the sustained increase in consumption, driven by fast rising household and, to some extent, government debt, a good part of the economy outside manufacturing has come through the slowdown in relatively good shape. Even in the recession year 2001, the rate of profit for the entire non-financial corporate economy outside of manufacturing actually rose slightly, and it has risen a lot faster in 2002 and the first half of 2003. On the assumption that manufacturing output has remained roughly flat in this interval, gdp in the non-farm non-manufacturing sector has risen at an annual average rate of better than 3 per cent. Jobs there increased by 600,000 between July 2000 and July 2003. Even total compensation has increased, if only slightly. Within non-manufacturing, those sectors best positioned to take advantage of falling interest rates, accelerated indebtedness, rising consumer spending, runaway import growth, and rising asset prices - notably, construction, retail trade and, above all, finance - have done extremely well, imparting a distinctive cast to the economic trajectory of the US in the new millennium.

Construction and retail

The construction industry has enjoyed its greatest boom in the postwar epoch, and for obvious reasons. The economy has grown virtually non-stop for a dozen years, placing unprecedented strain on the supply of housing. Since the mid-1990s, moreover, the growth of consumption, buoyed by ever easier access to borrowing, has increased even faster, magnifying the impact on the demand for housing of the sustained economic expansion. The inevitable consequence has been a spectacular increase of house sales and housing prices. Meanwhile, the growth of real wages in construction - where what had once been a highly organized industry is now largely de-unionized - has been held below 1 per cent per annum for the past ten years. Over the previous 15 years, between 1978 and 1993, construction real wages fell at an average annual rate of 1.1 percent - a total of 14 per cent. The rate of profit in the construction industry has thus soared as never before, increasing by a factor of six in the decade ending in 2001 and reaching a level in that year 50 per cent higher than at any previous time since 1945, including the long post-war boom.

The prosperity of the retail trade, like that of the construction industry, was built on well over a decade of wage cutting. Between 1978 and 1991, real compensation in this sector fell at an average annual rate of 1.6 per cent, or 19 per cent in total. Over the next decade, retailers benefited not just from the general expansion of the economy, but from the particularly rapid increase of consumer expenditures - yuppie spending sprees fuelled by the wealth effect. They were further favoured by the unstoppable rise of the dollar that cheapened imports, paving the way for a rising tide of inexpensive goods of every description from China. Between 1995 and 2002, the PRC became the leading exporter to the us, as Chinese imports rose from $44 billion to $122.5 billion, bounding forward at an average annual pace of 16 per cent. In this process, Wal-Mart - now the world’s largest corporation - has played a much publicized starring role, accounting today for no less than 10 per cent of all imports from China, taking advantage of the over-production that is rife in so many Chinese industries to demand ever lower prices. But many other American retailers also did extremely well out of this commerce. [12] Between 1992 and 2001, retail trade employment increased by 2.4 million or 19 percent. Over the same interval, the profit rate in retail trade increased every year, by a total of 57 per cent, including an 8 per cent increase in the recession year 2001.[13]

******* notes *******

12 P. Wonnacott, ‘Behind China’s Export Boom, Heated Battle Among Factories’, Wall Street Journal, 13 November 2003.13 Space precludes consideration of the (much smaller) hotel and accommodations industry, which followed a roughly similar trajectory to that of retail trade, its employment increasing by more than 20 percent and its rate of profit rising by 50 per cent between 1992 and 2001. Another consumption-driven case of a different sort, that requires much further study, is the vast health services industry, which registered huge jumps in corporate profits - from $4.9 billion in 1989 to $15.4 billion in 1994 to $17.3 billion in 1999 to $24.8 billion in 2001, not to mention a near 50 per cent expansion in employment.

*********

The expansion of the financial sector ran parallel to that of both construction and retail trade, but was of a different order entirely. Over the course of the 1990s, it assumed truly revolutionary proportions, transforming the map of the American economy and stretching uninterruptedly into the opening years of the new millennium. The turn to finance began in earnest with the shift to monetarism, high interest rates, a strong dollar and financial de-regulation at the start of the 1980s. It resulted, in particular, from the failure of a decade-long attempt to quell the decline of non-financial profitability, especially in manufacturing, with Keynesian deficits and a low dollar. But, despite ongoing steps to unshackle the financial sector and very major run-ups in both the bond market and the stock market during the 1980s, the combination of a debt-driven mergers and acquisitions craze, commercial real estate bubble, and equity inflation had by the end of the decade issued in major crises not only for commercial banks and developers, and the savings and loans, but even the non-financial corporations themselves.

Finance

All this changed in the 1990s, once Alan Greenspan had bailed out the financial sector. With the onset of the recession of 1990–91, Greenspan not only brought short-term interest rates down dramatically, enabling banks to pursue with ever-improving results their standard policy of borrowing cheap short-term and lending dear long-term. In addition, he allowed banks, in violation of government regulations, to hold onto enormous quantities of long-term bonds, which appreciated spectacularly as long-term interest rates declined, without setting aside funds to cover associated risk. [14] Financial sector profits were restored almost instantaneously, and they began a vertiginous ascent that has yet to be interrupted.

******* notes *******

14 Stiglitz, The Roaring Nineties, London 2003, p. 43.*********

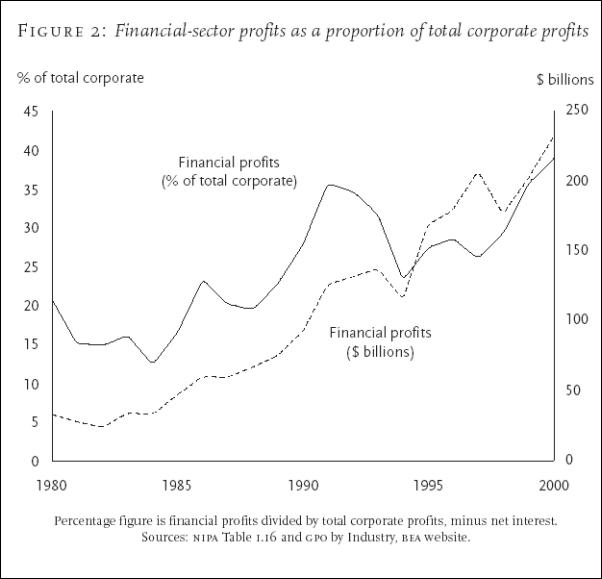

Every major trend of the decade of the 1990s, economic and political, ran in favour of finance. The real economy enjoyed continuous growth. Clinton’s turn to budget balancing plus the impetuous rise of the dollar in the wake of the reverse Plaza Accord - both engineered by his economic czar Robert Rubin, formerly ceo at Goldman Sacks - reduced inflation to a minimum, defending real returns from lending (just as they hurt returns in manufacturing). Clinton and Rubin pushed banking de-regulation to its logical conclusion, opening the way for the rise of ‘one-stop financial supermarkets’ that could make hitherto separated commercial banking, investment banking and insurance functions work together to magnify profits. Above all, the stock market bubble offered historically unmatched opportunities to rake in fees and profits for superintending share issues and mergers and acquisitions, while seeing to the finance of corporate and consumer borrowing. Finally, as the decade, and the equity price bubble, neared a climax, the nascent run-up in housing offered the financial sector still another huge field with multiple opportunities for killings. Between 1994 and 2000, profits for the financial sector doubled. Since, in the same period, profits in the non-financial corporate sector increased by only 30 per cent, financial sector profits as a proportion of total corporate profits climbed from 23 to 39 per cent. In so doing, they accounted for 75 per cent of the increase in corporate profits achieved in these years.

Click for big version

Nor did the bursting of the equity price bubble, and slowdown in the real economy from 2000 onwards, do much to hold back the ascent of finance. The housing bubble replaced the stock market bubble, and falling costs of borrowing did the rest. Profits stemming heavily from mortgage-related business, as well bond trading and underwriting - all tied to declining interest rates - enabled banks and securities firms to continue to rack up sensational gains, even despite the huge fall in share prices and big reductions in the growth of corporate borrowing. Between 2000 and the first half of 2003, the period of the slowdown, financial sector profits continued to expand dramatically, in both absolute and relative terms. In so doing, according to Morgan Stanley, they came to compose close to 50 per cent of total corporate profits, and to account for almost 80 per cent of the increase in corporate profits that occurred between 2000 and 2003. [15]

15 S. Galbraith, ‘Trying to Draw a Pound of Flesh Without a Drop of Blood’, Morgan Stanley US and the Americas Investment Research, 8 September 2003; S. Galbraith ‘Fading Fog’, Morgan Stanley US and the Americas Investment Research, 21 September 2003. The Morgan Stanley data is for s&p 500 corporations. Adequate government data is not yet available on profits for financial sector after 2001. The extraordinary growth in financial profits as a share of corporate profits and of their increase reflects, of course, in part the depressed state of profits outside finance.

iv. contradictions of a bubble-driven economy

The Fed’s turn to ever easier credit brought a semblance of order to the non-manufacturing economy, further rises in profitability for the construction industry and retail trade, and the continuation of an epochmaking expansion of the financial sector. But it did so, in large part, by means of - and at the cost of - inflating the value of financial assets across the board far beyond the worth of the underlying assets that they represent. The ensuing bubbles have provided the collateral required to support ever greater borrowing so as to keep consumption rising and the economy turning over. The outcome has been that US economic growth in the past three years has been driven more by increases in demand generated by borrowing against the speculative appreciation of on-paper wealth, than by demand generated by increased investment and employment, driven by rising profits.

Equity prices of course fell sharply from mid-2000. But, paradoxically, their decline failed even to begin to bring stock values into line with underlying profits, because the latter fell just as far. By October 2002, when equity prices bottomed out, the s&p 500 composite index was 42 per cent below its peak of July 2000; but the earnings-price ratio (i.e. the rate of return on investment in equities), which had already dropped by 48 per cent between its early 1995 peak and mid-2000, failed to rise at all, remaining stuck at around 3.7:1, meaning that equity investments yielded an average annual return of under 4 per cent. In the absence of the Fed’s cheap credit policy, share prices would obviously have fallen a great deal further with respect to underlying earnings. But by implication the equity price bubble was never allowed to burst.

A few months later, that bubble began a new expansion. From February 2003, bond prices rose and interest rates fell, apparently as an expression of the economy’s underlying weakness. Nevertheless, equity prices took off on a new, uninterrupted ascent, and the s&p 500 rose by about 20 per cent in the next six months. This was no doubt as the Fed had hoped. Nevertheless, by the summer of 2003, according to the Financial Times, the earnings-price ratio of the s&p 500 had fallen another 10 per cent or so to 3:1, compared to an historical average of about 7:1. The Fed was succeeding in keeping the business climate from darkening further. But, in so doing, it was actually sustaining the stock market bubble in the face of the equity price crash and ensuing economic slowdown. A significant correction could send the economy directly back into recession.

Housing bubble

As equity prices started from the mid-90s onwards to outrun underlying corporate profits and gdp, housing prices too began to bubble up. From 1975, when data first becomes available, through 1995, housing prices increased at an approximately similar rate to consumer prices, so remaining roughly steady in real terms. During the first half of the 1980s, the housing price index fell about 5–10 per cent behind the cpi before catching up to it again by 1985; then, between 1985 and 1990, it rose about 13 per cent above the cpi, before falling back again to its level in 1995. Real housing prices in 1995 were thus the same as they had been in 1985 and 1979. But, from 1995 through the first half of 2003, the rise in the home price index exceeded the increase in the cpi by more than 35 points, historically an unheard-of rise in real housing costs.

The explanation for this housing bubble seems fairly straightforward, given its timing. As shareholders accumulated wealth via the stock market boom, they were able to demand more expensive houses faster than the latter could be supplied. Then, as house prices rose, purchasers became willing to pay ever increasing sums for real estate, on the assumption that values would continue upwards, as in the stock market. When the stock market crashed and the boom came to an end in 2000, the real estate bubble was sustained in part by the Fed’s interest rate reductions, but also by the transfer of funds from the equity to the housing market, especially against a background of sharply reduced returns from lending at interest. The rise in house prices was self-sustaining, as it allowed homeowners, as interest rates dropped, to buy ever more costly homes, keeping demand running ahead of supply. [16]

Thus in just the four years between 1995 and 1999, household wealth in the form of housing increased by 25 per cent. But between the time of the equity market’s peak of 1999 and its trough of the first quarter of 2003, housing values rose even faster, prices increasing at an average annual rate about 5 percent higher than that of consumer prices. In fact, real home prices rose more during those three years than in any other comparable period on record. As a consequence, while shares (including mutual funds) owned by households plunged in value from $12.2 trillion to $7.15 trillion in this brief interval, a drop of $5.05 trillion or 44 per cent, residential real estate owned by households rose in value from $10.4 trillion to $13.9 trillion, an increase of $3.6 trillion or 35 percent, and regained its former place as households’ number one source of wealth.

In the wake of this huge paper appreciation of the value of their homes, households were able to extract dramatically increased funds by selling their homes at prices surpassing their mortgage debt, by refinancing their mortgages, and by taking out home equity loans - with enormous consequences for the growth of consumption and, in turn, gdp. Between 1990 and 1997, households’ extraction of equity averaged about $150 billion per year, but, as the housing bubble began to swell in the last three years of the decade, this figure doubled to around $300 billion annually in 1998, 1999, and 2000. In 2001, 2002 and the first half of 2003, home sales set new all-time records at $6.2 trillion, $6.6 trillion and $7 trillion (annualized). So did mortgage re-financing, at $1.2 trillion, $1.6 trillion, and $3 trillion, respectively. Against this background, in the same three years, the cash raised by way of mortgage borrowing reached unheard of levels - $420 billion, $600 billion and $716 billion, respectively. [17]

******* notes *******

16 This and the preceding paragraph depend on Dean Baker, ‘Homeownership in a Bubble: The Fast Path to Poverty?’, 2003, available at Center for Economic Policy Research website. See especially Figure 1 on The Real Cost of Owning and Renting.17 Time series on mortgage re-financing and cash-outs from it, constructed by Mark Zandi, chief economist at Economy.com, whom I wish to thank for his generosity in making this data available to me.

*********

In 2001, 2002 and the first half of 2003, mortgage equity withdrawals amounted, respectively, to an astounding 5 per cent, 7.7 per cent, and 9 per cent of US personal disposable income - playing an enormous role in sustaining consumer spending, in the wake of a radical decline of income growth. According to the Federal reserve, households use roughly 50 per cent of their cash-outs to finance increased consumer expenditures on everything from home improvement to vehicle purchases, vacations, educations, medical expenses, and, in the case of some hard-pressed families, even general living expenses. Another close to one-third of the cash is used repay higher-cost credit card and other instalment debt, freeing up income for more consumption. The remaining cash is used to finance other investments, usually real estate assets, tending to drive up housing demand, prices, and so in turn gains in household net worth.[18]

******* notes *******

18 Mark Zandi, ‘Housing’s Virtuous Cycle’, Regional Financial Review, August 2003, p. 13.*********

Click for big version

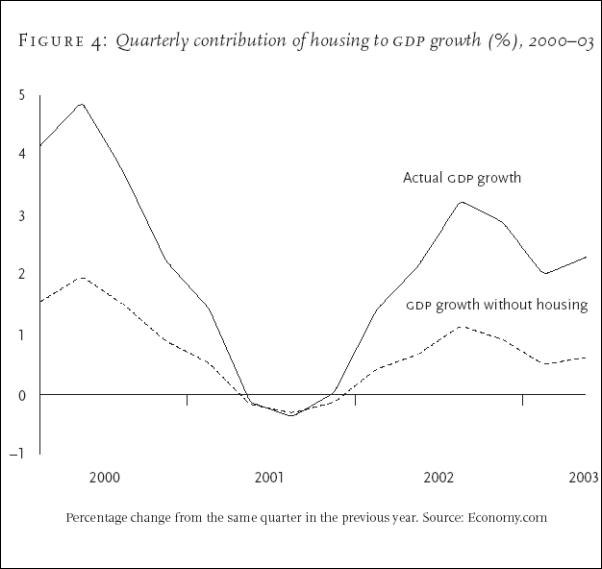

Since the end of 2000, money raised through mortgage refinancing alone has been responsible for at least 20 per cent of the total growth of gdp. If one also takes into account cash-outs through home sales and second mortgages, as well as residential investment spending and purchases of home furnishings, housing and mortgage markets have accounted, in total, for no less than two-thirds of gdp growth between 2000 and the first half of 2003. This means that, in the absence of these contributions from housing, average annual gdp growth in this period would have been just 0.6 per cent, instead of the 1.7 per cent that actually took place. [19]

******* notes *******

19 These results are based on simulations using Economy.com’s macroeconomic model. See Zandi, ‘Housing’s Virtuous Cycle’, p. 14 and fn. 3, especially Chart 3; also Homeownership Alliance, ‘The Economic Contribution of the Mortgage Refinancing Boom’, December 2002, pp. 1–5; and Homeownership Alliance, ‘Mortgage Refinancing accounts for 20 Percent of Real Economic Growth Since 2001’, press release, 17 December 2002 (both available at www.homeownershipalliance.com).*********

Click for big version

Yet it is hard to see how cashing out on this scale can fail to decline significantly in the not-too-distant future. This is because price inflation in real estate seems bound to lose speed, while interest rates - already near post-war lows - are more likely to rise than fall, leaving less scope for withdrawals. So too is homeowners’ propensity to borrow likely to decline, as the equity held by households in their homes had by the middle of 2003 already been reduced to a record post-war low of 54 percent of their homes’ value, down from 60 per cent a decade ago, while their debt as a percentage of household income has climbed to a record 110 per cent, up from 90 percent as recently as 1995. [20]

But if household borrowing slows, the growth of consumer expenditures, hitherto the key to the economy’s health, is bound to be hard hit. As Greenspan mildly put it, ‘[T]he frenetic pace of home equity extraction last year [2002] is likely to appreciably simmer down in 2003, possibly notably lessening support to purchases of goods and services.’ [21]

Dollar bubble and current account deficit

By pumping up consumer spending, especially by means of the debtdriven housing bubble, the Fed’s easy credit regime enabled Americans to keep raising their imports between 2000 and the middle of 2003, even as US exports declined in the face of the drop-off of purchasing power in most of the rest of the world. The consequence has been to prolong and deepen a pattern of international economic development that dates back to the first half of the 1980s, in which a steep rise in manufacturing imports and the US trade deficit widens the American current account deficit, expands US overseas liabilities, and fuels export-led growth throughout much of the rest of the world, above all East Asia.

******* notes *******

20 Business Week.21 ‘The Real Estate Market’, Speech by Alan Greenspan, 4 March 2003, frb website.

*********

This pattern was inaugurated in 1979–80 with the international turn away from Keynesian expansion to monetarist contraction as a means to combat the reduced profitability that continued to grip the advanced capitalist economies, especially in manufacturing. The ensuing jump in interest rates, reduction in the growth of social spending, and repression of wage growth did encourage the shake out of redundant, high-cost and low-profit means of production and, in that way, tended to contribute to the recovery of profitability system-wide. But, these same forces also brought about a sharp decrease in the growth of government and consumer spending, which, in combination with reduced investment growth, cut aggregate demand, inhibiting any uptick of profitability and exacerbating the slowdown. In the face of stagnant domestic markets, and further checks to deficit spending resulting from financial de-regulation, growth in most of the advanced capitalist world came to depend increasingly on stepping up manufacturing exports. But the ever greater generalization of export-dependent growth throughout the world economy only exacerbated the underlying tendency to over-capacity in international manufacturing which, if left to itself, would - sooner rather than later - have led to the seizing up of the international economy.

Against this background of system-wide stagnation, the impetuous growth of US debt, in combination with a soaring dollar, became the central motor driving the world economy. Simply put, since the early 1980s the system has moved forward by way of the expansion of the US current account deficit leading to the piling up of ever greater us liabilities to the rest of the world, on the one hand, and further increases in over-capacity in the international manufacturing sector, on the other. As late as 1979–80, the US ran manufacturing trade surpluses and, leaving aside fuel imports, overall trade surpluses as well. But, from 1981 onwards, US interest rates skyrocketed, the dollar took off, and US deficits, both federal and private, broke new records every year. As a result, the us manufacturing sector sustained the worst crisis in its post-war history. By 1987, with exports stagnating and imports skyrocketing, the manufacturing trade balance had gone a record $120 billion into the red and the current account deficit had reached an unprecedented 3.4 per cent of gdp. As the opposite side of the same coin, rising US manufacturing imports played a central role in pulling the world economy from the deep recession of the early 1980s and underpinning a new cyclical upturn.

The indispensability of US borrowing and currency appreciation for the economic dynamism of the global economy was demonstrated to the hilt from the second half of the 1980s onwards. As the dollar fell sharply from 1985, as private borrowing temporarily collapsed with the recession of 1990–91, and as US public deficits began to dry up from 1993, the US manufacturing trade deficit fell as low as $57 billion (on average) in 1992–93 and the current account deficit was temporarily eliminated. The consequence was that, during the first half of the 1990s, the advanced capitalist economies experienced their worst performance of the entire post-war epoch (outside of the US and East Asian nics, whose currencies were tied to the declining dollar).

Between the mid-1990s and the end of the century, there was still another reversal. The astounding run up of corporate and household borrowing, consequent upon the stock market bubble, in combination with a new takeoff of the dollar, now assumed the role previously played by public deficits in providing the subsidy to demand required to drive not just the us, but the world economy as a whole, by inciting a veritable tidal wave of US manufacturing imports. US manufacturing imports grew from $480 billion in 1993 to $1 trillion in 2000, more than doubling in seven years, while increasing as a share of manufacturing output by 50 percent. Already by 1995, the manufacturing trade deficit had jumped to $145 billion. It reached $271 billion by 1999, and increased by a further $100 billion to $369 billion by 2002. In this way, it accounted, by itself, for something like 60 per cent of the titanic increase in the us current account deficit between 1995 and 2002 and three-quarters of its absolute magnitude in 2002.

In the second half of the 1990s, the US current account itself quadrupled in size and tripled as a percentage of gdp, setting new records almost every year. Then, between 2000 and the middle of 2003, it rose by another twenty percent, to an unprecedented $544 billion, five times its 1995 level. In so doing, it both profoundly exacerbated the difficulties of the US manufacturing sector, and provided an indispensable stimulus to the rest of the world economy, pulling Europe and Japan out of their doldrums after 1995, saving much of East Asia (and the rest of the world) from near collapse in 1997–98, rescuing Latin America from deep crises in 1994–95 and again in 1998–99 and, finally, keeping global depression at bay from 2001 to the present.

Click for big version

Of course, the rise of the US current account deficit has itself depended on the willingness of the rest of the world to hold ever increasing us debts and assets, in effect financing the increase of American consumption to enable its own manufacturing exports and output to continue to grow. During the boom and bubble of the second half of the 1990s, overseas investors were more than happy to fund the US current account deficit. In expectation of big corporate profits and the unending appreciation of assets, they made huge direct investments in the US and bought enormous quantities of corporate equities and bonds, helping to push up the currency ever higher - a dollar bubble that accompanied, and was largely the creation of, the asset price bubble. Between 1995 and 2000, as the US current account deficit exploded, the total of US gross assets held by the rest of the world increased from $3.4 to $6.4 trillion, or 75 per cent of US gdp. [22] But as the American economy slowed and the us stock market declined from mid-2000, the rest of the world’s private investors found US assets decreasingly attractive. Purchases of corporate and Treasury bonds, as well as bonds sold by US agencies such as Fannie Mae and Freddy Mac, continued to grow smartly. But both equity purchases and foreign direct investment by the rest of the world fell sharply - the former dropping from an average of $153 billion for 1999 and 2000 to one of $65 billion for 2001 through the first half of 2003, the latter declining from $306 billion to $86 billion across the same time-periods. Europeans in particular fled US assets. Having peaked in the year ending in October 2000 at $115.6 billion, Eurozone purchases of US equities collapsed to just $4.9 billion in the year ending in April 2003. The result has inevitably been downward pressures on the dollar, intensified by higher interest rates in Europe. Between early 2001 and the middle of 2003, the dollar fell by 37 per cent against the Euro, 27 per cent alone in the year ending June 2003. [23]

The dollar’s decline against the Euro will tend, all else being equal, to make it easier for the US to export and harder to import. But, under current conditions, it may fail to bring about all that much improvement in the us trade and current account deficits, and risks undermining the European economies. Worsening recession in the EU would reduce European demand for US goods, offsetting much of the expected benefit for us exporters from the decline of the dollar. Between 2001 and the first half of 2003, the US trade deficit with Europe actually increased by more than onequarter, from $34.3 to $43.4 billion. Were the dollar to continue to fall in response to this widening gap, the Federal Reserve could be faced with an agonizing choice: either to let the currency drop and risk a wholesale liquidation of US properties by foreign investors - which could wreak havoc in asset markets and set off a serious run on the dollar - or raise interest rates and risk pushing the domestic economy back into recession.

******* notes *******

22 See The Boom and the Bubble, pp. 208–9 and Table 8.1.23 G. Chavez, ‘Weak capital influx seen choking dollar rally’, Reuters Online , 14 July 2003. Thanks to Doug Henwood and lbo list for this reference.

*********

East Asian policies

In fact, so far the overall trade-weighted decline in the dollar’s exchange rate has been limited to around 11 per cent. For its fall has occurred almost entirely against the Euro and only to a small extent against the currencies of East Asia. This is the case, even though trade with East Asia has accounted for a disproportionate share of US trade and current account deficits, which have risen above $100 billion per year with both Japan and China. The reason that the dollar has held up against East Asian currencies is that, led by Japan and China (and including Hong Kong), East Asian governments have stepped up a long-standing policy of re-cycling their current account surpluses into dollar denominated assets to keep down their own currencies. Today, East Asia holds $1.6 trillion in dollar reserves, 70 per cent of the world’s total, up from just 30 per cent in 1990. As the US entered its slowdown, and the American current account deficit widened even further, China, Japan, South Korea and Hong Kong entered the currency markets as never before, raising their combined ownership of US Treasuries from $512 billion to $696 billion in the brief period from December 2001 to June 2003. Indeed, over the first ten months of 2003, Japan and China alone covered an estimated 50 per cent of the US current account deficit, buying $150 billion and $100 billion worth of dollars, respectively. [24]

The East Asian governments have not, of course, pursued this course for altruistic reasons, but in order to sustain the rapid growth of their countries’ manufacturing exports to the US. Nevertheless, by closing the rising financing gap that would otherwise have resulted from the ever widening disparity between US exports and imports, East Asian governments have accomplished nothing less than to stabilize the US economy. In the absence of their purchases, the hyper-expansionary policies pursued by the Fed and the Bush administration would, almost certainly, have issued in a major fall in the dollar, leading to declining asset prices and rising borrowing costs and plunging the us, Asia, and the rest of the world back into recession, Still, it is hard to see how this symbiosis can be very long sustained.

******* notes *******

24 D. Hale, ‘The Manchurian Candidate’, Financial Times, 28 August 2003; C. Swann, ‘Weak renminbi is both boon and bane for the us’, Financial Times, 26–27 July 2003; J. Hughes, “Asia’s currency manifpulation comes under scrutiny,” Financial Times, 24 November 2003..*********

Thus even were East Asian governments able and willing to continue to buy dollar- denominated assets to keep their own currencies cheap so as to subsidize their manufacturers’ exports, this process cannot have a long life. For then the upshot would be to hold down US exports and increase US imports, forcing up the American current account deficit yet further and impelling still greater East Asian investments in us financial assets, with ominous implications for the US and global economies. On the one hand, the influx of East Asian funds onto US financial markets, by pushing down the cost of borrowing, would tend, directly or indirectly, to fuel ongoing asset price bubbles in equities and real estate. On the other hand, the growth of East Asian exports - puffed up by both the high dollar and government-subsidized US demand - would further undermine US industry, while exacerbating over-capacity in manufacturing on a global scale. This is, of course, much the same syndrome - of rising asset prices and manufacturing over-production - that has dogged the world economy and its US component throughout the bubble-wrapped boom and the slowdown that has followed. It is a self-undermining path, in which the inexorable rise of US obligations to the rest of the world enables it to grow through exports at the expense of US productive power, and therefore of the capacity of the US to honour those obligations - - a process that has already led to a stock market crash and a recession.

v. a basis for boom?

In order to keep the economy turning over while it worked off excess capacity and began once again to invest and create jobs, between the middle of 2000 and the middle of 2003, the economic authorities unleashed the greatest macroeconomic stimulus in US history. The Fed decreased its short-term rate from 6.5 per cent to a post-1958 low of 1 per cent (including reductions in November 2002 and June 2003). At the same time, the government’s fiscal position moved from a surplus of 1.4 per cent of gdp to a projected deficit of 4.5 per cent, or $450 billion. During the same interval, the trade-weighted value of the dollar fell more than 10 per cent. Nevertheless, despite this gargantuan boost, the economy barely budged. During the first half of 2003, real annualized expenditures on plant, equipment, and software still failed to grow. In the same period, annualized growth of gdp, at 2.35 per cent fell a drop lower than in 2002. It would indeed have been a third lower, just 1.5 per cent, had it not been for the huge and unsustainable leap in military spending on Iraq, which accounted for more than half of the economy’s 3.3 per cent growth in the second quarter. Meanwhile, unemployment rose to 6.2 per cent, and jobs were continuing to disappear at an alarming rate. In July 2003, the non-farm economy lost 57,000 jobs - after losing 83,000 and 76,000, respectively, in June and May - and non-farm employment fell 38,000 below its level of July 2002. The disparity between stimulus and response appeared to be a direct expression of the economy’s underlying weakness - its still unresolved problems of over-capacity and corporate financial fragility.

By autumn 2003, however, the economy certainly was accelerating. gdp leapt forward at a 8.2 annualized pace, the largest quarterly gain since 1965. . Equally significant, job growth suddenly went positive to the tune of more than 100,000 per month in September and October. To round out the picture, non-residential investment sprang up at an 14 per cent annualized pace, the highest since the beginning of 2000. The economy seemed suddenly to have taken off.

Current acceleration

It may turn out, in retrospect, that the third quarter of 2003 did mark the start of a sustained cyclical upturn. Yet despite the spectacular headline numbers, it is not clear that US economic advance in the third quarter broke in a decisive way from its dependence on bubbles, debt, and consumption. . Once again, personal consumer spending, which expanded at a spectacular 6.4 per cent pace - including a whopping 26.9 per cent increase on durable goods - was at the heart of expansion. Along with the growth of residential investment, it accounted for 75 per cent of total gdp increase. What drove personal consumption? It certainly was not hourly real compensation ( excluding self-employed), which actually fell in the quarter by 0.2 percent for the whole economy, with the result that annualized total real compensation for the first three quarters of 2003 actually fell slightly compared to 2002.

What put money in consumers’ pockets was, above all, households’ enormous cash-outs from mortgage financing. During the first half of 2003, these climbed to about 7 per cent of gdp, and must have played a central role in the spending spree of the third quarter. The Bush administration’s tax rebates of 2003 were also unquestionably pivotal, putting about $25 billion into people’s pockets in the third quarter - a whopping $100 billion on an annualized basis. While real pre-tax personal income grew by 1 per cent during the third quarter, after tax personal income increased by a stunning 7.2 per cent.

What of investment, ultimately the decisive variable? A 14 per cent rise is in itself impressive and, taken in connection with the previous quarter’s 7 per increase, could bode well for the future. Still, a good part of this increase was almost certainly driven by the 2003 tax law, which allows firms to accelerate depreciation, but only if they do so by the end of 2004. In any case, annualized non-residential fixed capital investment in the third quarter was only 4.1 per cent higher than in 2002 and still 1.8 per cent and 6.9 per cent lower than in 2001 and 2000, respectively. This is not yet evidence of a boom in capital accumulation. The sizeable third quarter increases in employment, coming after almost three years of steady decline, were unquestionably the most promising sign for the economy, and perhaps point to a turn-around. But they were still insufficiently large to offset the numbers entering the job market, and thereby reduce unemployment; or to effect any significant increase in real total compensation and so to lift demand. Clearly, there remains a long way to go to transcend the worst cyclical recovery of employment in the postwar era. . In the 23 months following the official end of the recession in November 2001, private sector employment fell by a further 919,000, with almost every sector suffering major losses. Had it not indeed been for a gain of 753,000 jobs in education and health services, job losses in this period of ostensible recovery would have been well over 1.5 million. At the analogous point in the ‘jobless recovery’ following the March trough of the 1990–91 recession, i.e. January–February 1993, the economy was creating 277,000 jobs per month, more than double the 125,000 per month of September–October 2003.

******* notes *******

25 ‘Virtually all of the new consumption during the [third] quarter was financed by tax refunds, mortgage refinancing or borrowing’: P. G. Gosselin, ‘us Economy Expands at its Fastest Pace Since 1984’, Los Angeles Times, 31 October 2003. That personal consumer expenditures fell in September appears to indicate that households had already largely spent their rebates. In mid-November Wal-Mart was sounding a warning over the strength of the recovery in US consumer spending,saying its shoppers remained cautious, favoured cheaper goods, and had little cash to spare: Financial Times, 14 November 2003.*********

A sustainable rise in profitability?