WBD & Disney Earnings: Can Legacy Giants Survive On Their Own?

Thursday, 9 November 2023, 6:58 pm Article: Parrot Analytics

The two largest companies by corporate demand share

report earnings on Wednesday, facing similar fundamental

issues heading into 2024 and beyond.

Disney and Warner

Bros. Discovery (and its predecessors) have diligently

followed Wall Street’s shifting moods over the last half

decade. Disney chased Netflix’s streaming subscriber

growth-at-all-costs business model and was handsomely

rewarded at first before the bill came due in

2022.

WBD’s very existence is the result of an

attempt to create a Netflix competitor by combining the

media assets of then-AT&T’s WarnerMedia (née Time

Warner) under streaming-focused CEO Jason Kilar, with those

of then-Discovery Communications.

As of November 2023,

Disney‘s market cap sits at less than half of its peak

valuation from March 2021, and WBD is valued roughly the

same as the Hulu platform.

If any two companies in the

industry are relatively ‘strike proof�� it should be

Disney and WBD. They have the most in-demand libraries to

keep streamers as fresh as possible, and access to the most

popular live sports.

But with massive debt loads,

shrinking linear TV businesses, and cracks appearing in

previously untouchable franchises, both companies have put

virtually everything on the table to get their media and

streaming arms to consistent profitability. Once golden

geese such as ESPN, NBA rights, premium scripted content

exclusivity, and more are now up for sale.

Heading

into 2024, the Magic Kingdom and Dream Factory are being

forced to wake up and smell the pixie dust.

Hulu

Deal

Disney’s

recent announcement that it will carry out its 2019

agreement to buyout Hulu should end up costing the company

north of $9B, at a time when cost cutting is the name of the

game.

In terms of content, Disney presumably

bringing Hulu into Disney+ makes sense from a scale

perspective. Disney+ and Hulu combined would easily overtake

Netflix as the platform with the most total catalog demand

— including all TV series and movies available — with US

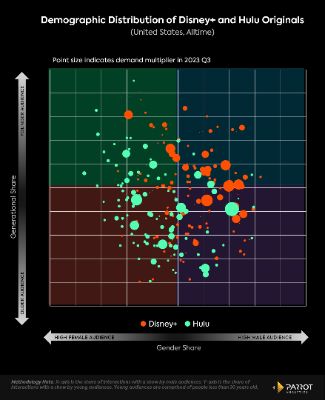

audiences. Parrot Analytics audience demographic data shows

that Hulu and Disney+ originals would combine well to form a

true four quadrant service.

While the price tag is

high, the Hulu buyout will result in increased synergies for

Disney. According to Parrot Analytics, integrating key Hulu

originals and additional library content into the Disney+

app could prevent around $500 million in at-risk churn

revenue, and add an additional $750 million in advertising

revenue.

However, it’s also fair to wonder how a

combined single service app may affect churn, which the

Disney bundle is effective at

mitigating.

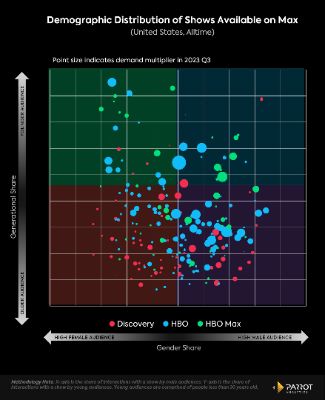

Warner Bros. Discovery

WBD’s

raison d'etre, Max, serves as one example of how to

integrate massive content libraries into one app. Combining

Discovery originals onto the old HBO Max platform has

created a four quadrant service that is second only to

Netflix in terms of total catalog demand with US audiences.

However, subscriber growth for Max has plateaued and even

ticked down in Q2 2023.

After building a walled

garden streaming service, WBD is now back to licensing out

some of its premium content, including HBO Originals and DC

films, even to Netflix.

These moves will help

WBD’s bottomline line, and have increased demand for the

licensed content, but it may also be pulling consumers back

to Netflix and help it further its lead over the

field.

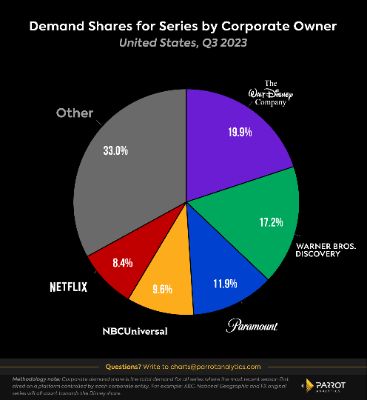

How To Leapfrog Disney?

Corporate

demand share assesses the long-term viability of the top

media companies as they look to consolidate their original

content’s availability exclusively onto their own

platforms, and can effectively help value a conglomerate’s

legacy and library content in aggregate.

Since the

Discovery-WarnerMedia merger went through in April 2022,

Disney and WBD have been the top two media conglomerates in

corporate demand share. Disney has historically been the

biggest slice of this pie chart. These two companies alone

account for 37.1% of the demand for all TV content with US

audiences as of Q3 2023.

WBD’s most

straightforward path to leapfrogging Disney in this category

is to join forces with a competitor. A combination with

either NBCUniversal or Paramount Global would put either new

entity ahead of Disney in Corporate Demand

Share.

While the Hulu buyout should improve

Disney’s streaming business, Disney may be arming Comcast

with the funds to make an industry-shifting acquisition.

Comcast CEO Brian Roberts made failed attempts to acquire

both Disney and 21st Century Fox. Regulatory hurdles aside,

could the third time for Roberts finally be the charm when

it comes to Warner Bros. Discovery?

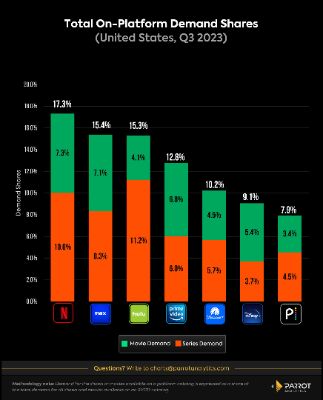

Go-To

Streaming Home

Demand

for original series drives subscription growth, and library

content is key for customer retention, an increasingly

crucial element of all streaming strategies as the market

matures and consumers are offered more choice and easier

ways to cancel than ever.

Library content will also

be a crucial short-term asset as Hollywood’s labor strikes

prolong, with new shows and movies likely to run dry in into

early 2024 and beyond.

There is a clear ‘Big

Three’ in terms of general entertainment platforms.

WBD’s Max just edge’s out Hulu for second place behind

Netflix in this category.

That said, once Hulu

(15.3%) and Disney+ (9.1%) are combined, that new Disney

streamer should easily top both Netflix and Max when it

comes to total on-platform demand for

content.