https://www.scoop.co.nz/stories/BU2507/S00252/headline-heads-north-but-core-matters-more.htm

|

| ||

Headline Heads North. But Core Matters More. |

||

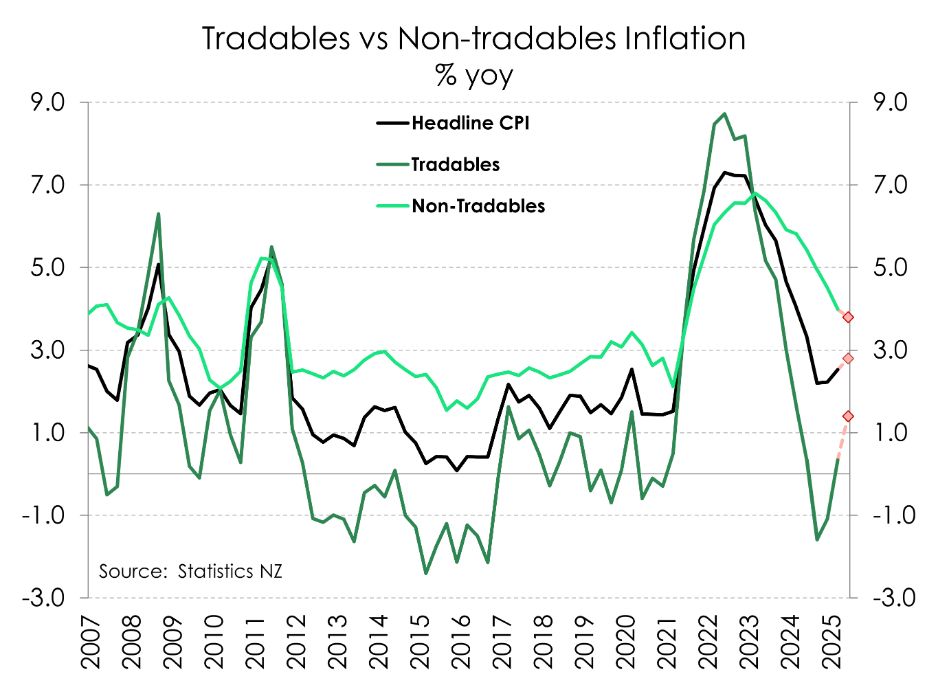

The first test for a cut to the cash rate in August comes next week. Kiwi inflation data is due out on Monday. By our calculations, consumer prices likely rose 0.7% over the June quarter. Such a move would see an acceleration in annual inflation, from 2.5% to 2.8%. Inflation is pushing closer to the top end of the RBNZ’s 1-3% target band. But context is key. A strengthening in imported inflation is driving headline higher. But domestic price pressures, on balance, continue to cool. For now, there’s little risk this bout of high inflation will persist. Especially given that there's still significant spare capacity in the Kiwi economy.

The rapid deceleration in imported inflation, which helped to pull down headline, is reversing course. We’re no longer importing deflation. The RBNZ May forecasts pencilled in a 0.9%yoy increase in imported inflation from 0.3%. Those forecasts predate the recent lift in food prices. More timely data suggests a larger lift. We expect annual tradables inflation to rise to 1.4%.

Domestic inflation, in contrast, should continue its (slow) move south. We expect annual non-tradables inflation to pierce below 4% for the first time in four years. We have pencilled in a fall to 3.8%, broadly in line with the RBNZ’s 3.7% estimate. Over time, domestic inflation has become less broad-based. Capacity pressures have eased, and the moderation in wage growth suggests that price-setting behaviour is adapting to the low-inflation environment. Reflective of a weakening economy and labour market, is the continued slowing in services inflation. Wage growth has eased significantly. As a result, services inflation has trended lower.

For monetary policy, the underlying trend in inflation is most important. Core measures of inflation strip out the volatile price movements. Encouragingly, core inflation has been trending south since hitting the 6.7% peak at the end of 2022. In the year to March 2025, core inflation fell to 2.6%. We expect more progress was made over the June quarter, with measures of core inflation remaining within the RBNZ’s target band.

Home Page | Business | Previous Story | Next Story

Copyright (c) Scoop Media