https://www.scoop.co.nz/stories/BU2603/S00394/are-rate-hikes-coming-we-certainly-hope-not.htm

|

| ||

Are Rate Hikes Coming? We Certainly Hope Not. |

||

Things are getting messier and more heated in the Middle East. President Donald Trump has given Iran a 48-hour ultimatum: fully re-open the Strait of Hormuz or have their power plants obliterated. The threat has not gone down well. Iran has swiftly countered back saying that it would target all energy, information technology, and desalination infrastructure in the region belonging to the US and Israel.

The question now is whether the trigger will actually be pulled by either party. We know Trump loves a headline. And the messaging from him, in even just the past week, has been all over the place. From mid-week comments around ruling out a ceasefire, to ending Friday with comments that the US may be close to winding down its military efforts, and now this.

Taking all the escalating threats into account, we expect oil prices to head higher when markets open today. Prices had surged to US$119pb following Israel’s attack on Iran’s South Pars gas field mid week. But we closed the week slightly lower at $112pb after Trumps comments on Friday, though now redundant.

It’s a very fluid situation. With the countdown on, we’ll know more tomorrow. But at least for now, both sides won't back down… and we’re left watching the clock.

Acutely aware of the ongoing geopolitical risks, the RBNZ last week announced a change to the speech topic Governor Breman is set to deliver to the Business NZ’s CEO Forum tomorrow. The speech was originally meant to draw on the February MPS to discuss the current outlook. But communications from the RBNZ last week have confirmed that the speech will now focus on the potential economic impacts for NZ from the ongoing conflict in the Middle East.

Published publicly at 9am tomorrow, a lot hinges on the messaging around inflation and demand risks, and in light of the push higher in wholesale rates. Fears of inflation have markets traders pricing in three rate hikes this year. Rate hikes are completely unwarranted in our view. And we completely disagree with market sentiment. We see hikes as infeasible for the RBNZ, given the immense demand shock that the oil disruption brings to the Kiwi economy. (See our COTW for more).

Taking a leaf from the number of Central Banks taking the stage last week (see our special topic), we expect Breman to acknowledge near-term inflation, but emphasize the significant downside risks to growth. And in doing so, push back on wholesale rates… much like she did at the end of last year, and then again at their February MPS. It’s like a scene from Pulp Fiction… we need the “wolf” to hose down the gore in rates markets. “If I'm curt with you it's because time is a factor.”

Our starting point is also a factor. Last week’s disappointing GDP numbers showed we are more sensitive to any shocks, as we’ve struggled to recover for a severe recession. (See our full review here).

Output lifted 0.2% over the December quarter. And the impressive 1.1% lift in the September quarter was revised down to 0.9%. From the Reserve Bank’s perspective, the softer forecast economy to matters. A smaller assumed economy implies weaker domestic inflation pressures, with the output gap is closing more slowly than expected. That means less inflation pressure.

Overall, we've managed to produce just 1.3% of growth over the year, just 0.7% on a per capita basis. We're still struggling. And that’s before the sharp deterioration in the outlook over the past three weeks given the conflict in the Middle East. We struggle to see the RBNZ delivering rate hikes to fight off a supply-side shock (they have no control over). The damage to demand outweighs inflation risks.

To end on some good news, we got word last week that, from April onwards, every OCR decision will be followed by a 3pm press conference. Previously, press conferences were reserved for the quarterly Monetary Policy Statements only, and not the smaller Monetary Policy Reviews. We like the move. It’s a genuine improvement in transparency. And that’s what we need, especially key in times of uncertainty.

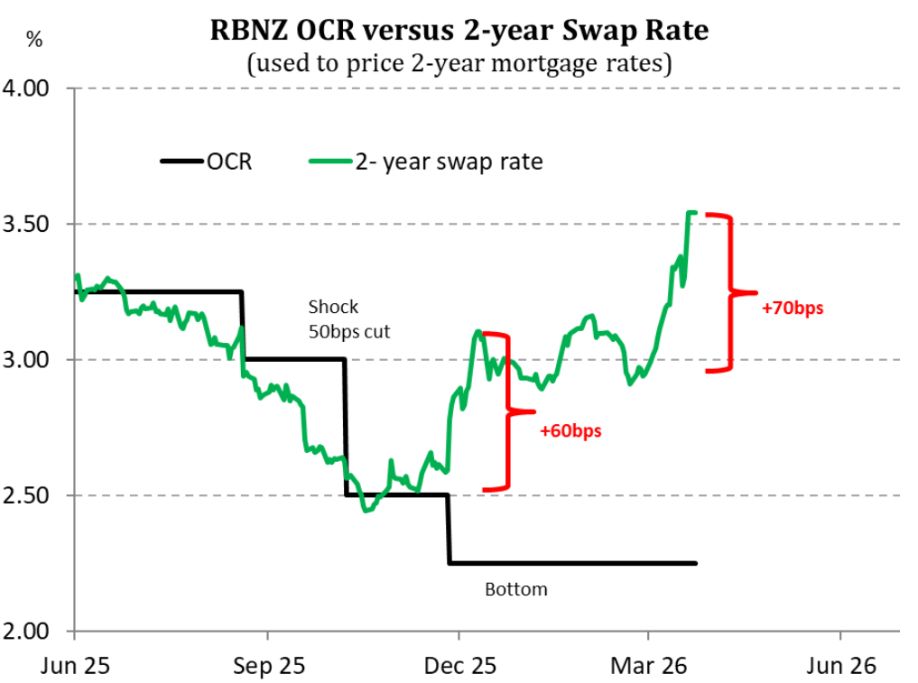

We have witnessed another dramatic move in financial markets. Wholesale interest rates have surged higher, as thoughts of oil induced inflation dominate positioning. "Low and stable" inflation/rates have become "high and uncertain". And traders have pushed short dated yields over 70bps higher in just a few weeks.

The escalation in the Iran war, without an end in sight, has markets fixated on not just the oil price, but delivery of refined products - diesel especially. It's diesel that is used in the big trucks and farming equipment. It seems markets are pricing in higher inflation, without consideration for demand destruction.

Higher petrol prices hurt consumers and businesses. Short-dated rates have over 3 rate hikes priced in for this year. We find that hard to imagine, let alone forecast. The pivotal 2-year swap rate has been catapulted to 3.64%, and climbing, from a 2.9% low following the last RBNZ's statement in February. That's a massive move, that reminds us of the spike following the RBNZ's previous statement in November. These massive moves are being passed onto mortgage rates, effectively tightening financial conditions (again).

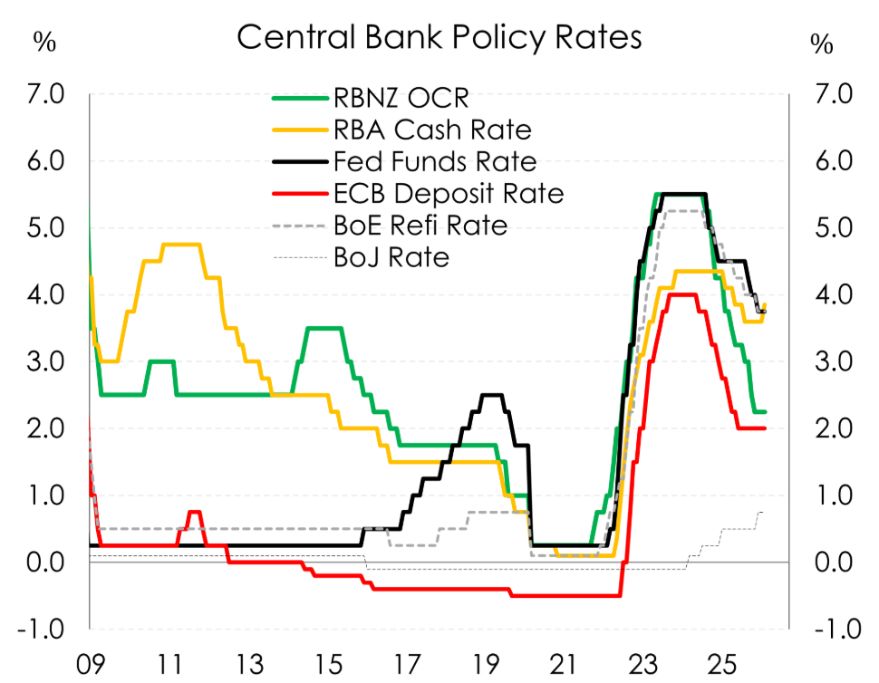

Alongside all the war headlines we also had a bonanza of Central banks meetings over the last week to keep us busy. The decisions from all were virtually as called by markets. With the Fed, BoE, ECB, BoJ, BoC, and Swiss bank all keeping rates steadily on hold. While the RBA, under a close 5-4 vote, lifted the cash rate 25bps to 4.10%.

For those that kept rates steady and on hold the overall tone last week was broadly wait and see with acknowledgements to both the upside risks of inflation and downside risks to growth. Just some differences in tone around the edges.

But it’s worth highlighting the move from our neighbours down under. The RBA is the only central bank that raised rates last week, and that only by the nearest of margins. We stand firm that the Kiwi economy is in a very different position to the Aussies, and so we don’t see this as a risk that the RBNZ will follow suit.

The RBA voted 5-4 to hike the official cash rate last week. This is the second hike in a row for the RBA, raising the OCR 25bp from 3.85% to 4.1%.

The split-vote is a reflection of global uncertainty and high Aussie inflation. Unlike New Zealand, Australia’s economy has been running hot, with a tightening labour market and higher than expected growth since February. The disagreement between board members centred around timing, with all members agreeing that a hike was needed, but some tempted to hold out until May. This is completely different to the Kiwi economy. Our labour market is still showing signs of large spare capacity and low demand.

The conflict in Iran and subsequent oil price disruption is increasing the downside risk to the global and Australian economy. The resulting higher petrol prices will act as a tax on consumption while also adding to inflation. However, Governor Bullock was clear, the RBA believes that higher fuel costs will not slow demand enough to bring Australia’s inflation down on their own. New Zealand is more likely to feel the downside risk to demand from the increased oil prices, because our demand never really got a good chance to heat up in the first place.

Comparing the Kiwi and Aussie economies, if they were pots on the stove, the Kiwi economy is luke-warm at best, while the Aussie is starting to simmer. The RBA wants to make sure their pot doesn’t boil over, while the RBNZ should be trying to make sure that the Kiwi doesn’t grow completely cold. All that to say that our view on next week’s RBNZ decision is that they will hold and that rate hikes are not a part of the story for New Zealand in 2026.

Another central bank holing last week included Canada’s BoC which is set to look through the conflict’s near term inflationary effects. Although Canada is sitting at 2% inflation, a much more comfortable spot for their economy than the Kiwi 3.1%, we feel that a similar approach is needed at home. The Canadians quoted slack in their economy and the expectation that higher gas prices will “squeeze consumers, leaving them with less income for other spending” – exactly our view.

Home Page | Business | Previous Story | Next Story

Copyright (c) Scoop Media