https://www.scoop.co.nz/stories/HL2511/S00020/making-new-zealand-superannuation-sustainable.htm

|

| ||

Making New Zealand Superannuation Sustainable |

||

We need to make New Zealand superannuation sustainable. It is expensive, but also a vital lifeline for many in retirement. The proportion of New Zealanders who are 65 years and over is only increasing the government burden of paying superannuation, while the percentage of New Zealanders in the paid workforce decreases.

How to fix this is the conundrum. I propose a new model below to do this.

We need to act now while we have choices and options. Economic commentators - such as Cameron Bagrie, Shamubeel Eaqub, Brian Easton, Brad Olsen, and Susan St John - have long been urging governments of both stripes to do something.

The Treasury's 2025 Long-Term Fiscal Statement likewise implores action, noting that: "Over the last 20 years our Statements have consistently warned that population ageing will place increasing pressure on New Zealand’s long-term fiscal position." This year's statement presents three broad and logical options: reducing the amount of superannuation paid out; raising the age of eligibility, and introducing means-testing.

None of these are politically palatable in a context where many voters fear financial vulnerability in their old age and superannuation is still seen as an entitlement following a life of work.

Reducing the amount paid out is difficult when many superannuants cannot cover the basics.

Raising the age of eligibility may "disadvantage some groups and costs would increase elsewhere"

Means-testing is argued to be "not as straightforward as other benefits."

But Treasury also suggests that, rather than bluntly implementing one or other of its options, a combination of these is plausible.

What might this look like?

Combining these options doesn't have to be synchronous. Instead I propose we adopt a staged model which provides superannuation at different times for different groups of people. This sounds complicated - but it doesn't have to be.

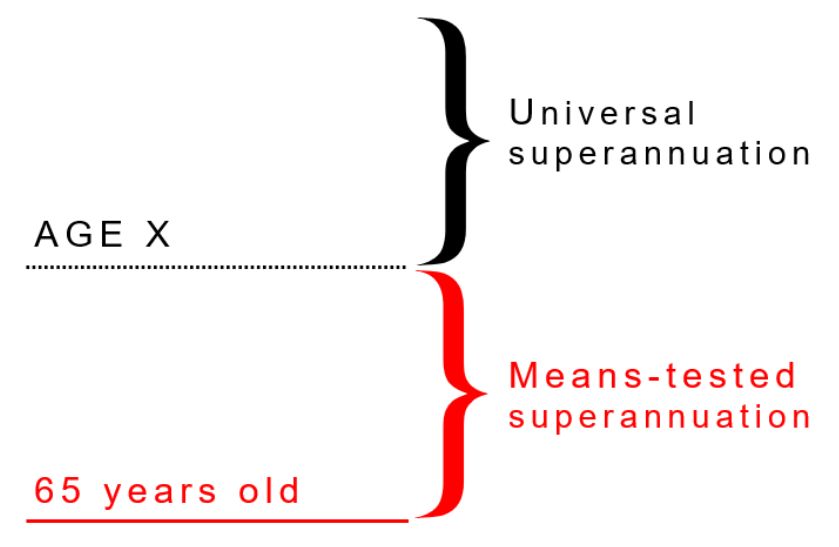

One way of combining income mean-testing and raising the age of eligibility is to introduce a limited period of means-testing beyond which superannuation is universally available.

This would mean that the age of universal superannuation could be gradually raised (e.g. by 5 years over 15 years) while maintaining 65 years as the age for a means-tested superannuation.

Because this model retains the safety net for those most at need, raising the age of universal superannuation is less politically problematic and so has potential for broader appeal across the political spectrum.

Because the model does not abandon the concept of a universal superannuation there is an implicit acknowledgement that, after a life of work, we are all entitled to receive its benefit.

The model as a concept does not answer every question, and because of this it allows for political difference as much as it aims for bipartisan support. Key questions that remain include: at what age would universal superannuation begin and what would the transitional arrangements be to get us there?

Another question is what constitutes means testing? A starting point for this discussion would be income testing with possibly some work test. This would be a more productive conversation starter than asset or wealth testing, which is said to be difficult and, in the words of one commentator, "just uranium wrapped in barbed wire."

When raising the age of superannuation is broached, the issue of equity also surfaces - particularly for people in physically-demanding occupations, who might need to retire earlier than other groups. Life expectancy is another factor that might warrant an exception to the model. Such factors need to be clearly identified, substantiated and researched, and further discussion had as to how targeted exceptions, such as exemption from means testing, might occur.

The reason for proposing this model is to advance a moderate way that could reduce the cost of superannuation that might garner cross-party backing. The moderation of such a staged model is important because progress on the matter of superannuation is currently stifled because any changes are considered "political suicide."

No expert is saying the current model is financially sustainable, and the consenus is that action sooner will limit adverse consequences. Politicians need to step their current thinking up a gear and start to implement change.

A strength of this model is that it keeps access to superannuation at 65 years for those in need while not abandoning the cherished idea of universal superannuation. These are two principles which surely a majority of us can support.

Home Page | Headlines | Previous Story | Next Story

Copyright (c) Scoop Media