Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Constrained Conditions For The Rural Sector

Data released today by the Real Estate Institute of New Zealand (REINZ) shows there were 122 less farm sales (-32.1%) for the three months ended May 2020 than for the three months ended May 2019. Overall, there were 258 farm sales in the three months ended May 2020, compared to 251 farm sales for the three months ended April 2020 (+2.8%), and 380 farm sales for the three months ended May 2019. 1,132 farms were sold in the year to May 2020, 19.5% fewer than were sold in the year to May 2019, with 26.6% less Dairy farms, 27.8% less Grazing farms, 26.0% less Finishing farms and 1.2% less Arable farms sold over the same period.

The median price per hectare for all farms sold in the three months to May 2020 was $23,221 compared to $22,244 recorded for three months ended May 2019 (+4.4%). The median price per hectare increased 2.5% compared to April 2020.

The REINZ All Farm Price Index fell 0.1% in the three months to May 2020 compared to the three months to April 2020. Compared to the three months ending May 2019 the REINZ All Farm Price Index fell 5.1%. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors.

Two of the 14 regions recorded an increase in the number of farm sales for the three months ended May 2020 compared to the three months ended May 2019, namely West Coast (+4) and Otago (+1). Waikato recorded the most substantial decline in sales (-24) followed by Bay of Plenty (-22). Compared to the three months ended April 2020, eight regions recorded an increase in sales with the biggest increases being in Bay of Plenty (+6) and Taranaki (+4) Brian Peacocke, Rural Spokesman, at REINZ says: “Sales volumes for the 3-month period ending May 2020 are relatively stable when compared to the previous 3-month period.

However, in comparison to the equivalent period in 2019, there has been a 32% reduction in the number of farm sales, and a massive 41.75% reduction in sales from the same period in 2018, two years ago.

“The COVID-19 pandemic is one of the major reasons for the drop-off in activity, but this situation has been exacerbated by a trend emerging prior to the commencement of the lockdown whereby reports from around the country consistently confirm the apparent “restricted lending” policy within the banking sector where obtaining finance for farm purchases is becoming an increasing frustration for the farming sector.

“Drought conditions have continued to plague parts of the country, particularly Hawke’s Bay, whereas by comparison, reports from Southland indicate the region has experienced one of the best autumns for some time.

“The very tight situation relating to killing space in the meat processing plants, which was compounded by social distancing required under the lockdown, irrespective of it being an essential industry, has now began to ease, much to the relief of those who have been trying to move surplus animals off the farm pre-winter.

“Product prices in the main reflect the above, but forward signals for beef, lamb and the volatile dairy payout appear to be reasonably optimistic. Horticulture, the golden child in the agriculture sector, is going well with kiwifruit in particular looking set for record prices.

“The exchange rate is solid, the Official Cash Rate is at a record low, as are interest rates albeit that issue is a moot point if the banks are reluctant to lend money, even to supposedly well qualified clients,” he concludes.

Points of Interest around New Zealand include:

- Northland/Auckland - tight conditions in the Far North improve in the mid to lower North with a scattering of predominantly grazing category sales and two dairy farm sales at the lower end of the price scale. Auckland conditions were similar apart from the Franklin district which experienced restrained activity in the dairy and finishing categories

- Waikato/King Country/Taupo - a slight increase in dairy farm sales in the Waikato and Otorohanga districts with price matching quality; light activity in the finishing sector and no sales recorded in the Waitomo and Taupo districts

- Bay of Plenty/Rotorua - a big uplift in horticultural sales in the Bay of Plenty (from 1 sale in April to 8 in May) with the sale of a large kiwifruit orchard at Paengaroa at just under $12m leading the way; several strong sales of finishing units in Western Bay of Plenty and Whakatane but no sales in the Rotorua district

- Gisborne/Hawke’s Bay - no farm sales in Gisborne but a reasonable scattering of dairy, finishing and grazing units in the Wairoa and Heretaunga areas, with two strong sales of horticultural properties in the Hastings district – very quiet in Central Hawke’s Bay

- Taranaki - a good sale for an arable property in the New Plymouth district and several strong sales of dairy support properties in South Taranaki

- Manawatu/Wanganui - a good range of transactions at solid prices for grazing and finishing units from Ruapehu to the central Manawatu and into the Tararua district, where two dairy farm sales were the icing on the cake. a good range of transactions at solid prices for grazing and finishing units from Ruapehu to the central Manawatu and into the Tararua district, where two dairy farm sales were the icing on the cake

- Wairarapa/Wellington - light activity in the drystock sector, restricted to the Carterton and Featherston districts

- Nelson/Marlborough - medium activity at sensible prices for finishing units in the Tasman district but a good lift in results with good prices paid for good quality, well established vineyards in the Marlborough district

- Canterbury/Westland - a mix of finishing and grazing property sales at current prices in the Hurunui, Waimakariri and Selwyn districts, with similar volumes at stronger prices for finishing units in the Ashburton and Timaru districts, these being backed up by an arable sale at Waimate – one grazing sale on the West Coast

- Otago - quieter than previously but arable sales at strong prices featured in the Waitaki and Dunedin regions, supported by a solid sale of a finishing block in the latter locality

- Southland - the strongest region in the country again with a good level of sales at good prices for dairy, grazing and arable properties, all within the Southland district.

Grazing farms accounted for the largest number of sales with a 26% share of all sales over the three months to May 2020, Finishing farms accounted for 25%, Dairy accounted for 13% and Horticulture accounted for 12% of all sales. These four property types accounted for 76% of all sales during the three months ended May 2020.

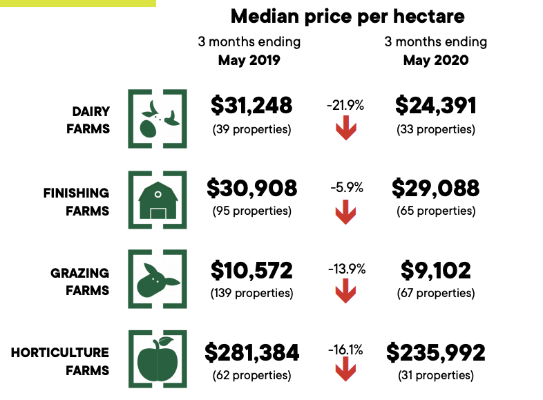

Dairy Farms

For the three months ended May 2020, the median sales price per hectare for dairy farms was $24,391 (33 properties), compared to $30,790 (35 properties) for the three months ended April 2020, and $31,248 (39 properties) for the three months ended May 2019. The median price per hectare for dairy farms has decreased 21.9% over the past 12 months. The median dairy farm size for the three months ended May 2020 was 123 hectares.

On a price per kilo of milk solids basis the median sales price was $32.50 per kg of milk solids for the three months ended May 2020, compared to $32.97 per kg of milk solids for the three months ended April 2020 (-1.4%), and $32.17 per kg of milk solids for the three months ended May 2019 (+1.0%).

The REINZ Dairy Farm Price Index fell 3.5% in the three months to May 2020 compared to the three months to April 2020. Compared to May 2019, the REINZ Dairy Farm Price Index fell 5.7%. The REINZ Dairy Farm Price Index adjusts for differences in farm size and location compared to the median price per hectare, which does not adjust for these factors.

Finishing Farms

For the three months ended May 2020, the median sale price per hectare for finishing farms was $29,088 (65 properties), compared to $29,523 (60 properties) for the three months ended April 2020, and $30,908 (95 properties) for the three months ended May 2019. The median price per hectare for finishing farms has fallen 5.9% over the past 12 months. The median finishing farm size for the three months ended May 2020 was 35 hectares.

Grazing Farms

For the three months ended May 2020, the median sales price per hectare for grazing farms was $9,102 (67 properties), compared to $9,344 (68 properties) for the three months ended April 2020 and $10,572 (139 properties) for the three months ended May 2019. The median price per hectare for grazing farms has fallen 13.9% over the past 12 months. The median grazing farm size for the three months ended May 2020 was 133 hectares.

Horticulture Farms

For the three months ended May 2020, the median sales price per hectare for horticulture farms was $235,992 (31 properties), compared to $214,942 (30 properties) for the three months ended April 2020 and $281,384 (62 properties) for the three months ended May 2019. The median price per hectare for horticulture farms has fallen 16.1% over the past 12 months. The median horticulture farm size for the three months ended May 2020 was 6 hectares.

University of Auckland: Junk Food Designed To Make Us Eat More, Study Finds

University of Auckland: Junk Food Designed To Make Us Eat More, Study Finds Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality