Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Rural NZ Remains Resilient

Data released today by the Real Estate Institute of New Zealand (REINZ) shows there were 131 more farm sales (+48.5%) for the three months ended September 2020 than for the three months ended September 2019. Overall, there were 401 farm sales in the three months ended September 2020, compared to 386 farm sales for the three months ended August 2020 (+3.9%), and 270 farm sales for the three months ended September 2019. 1,285 farms were sold in the year to September 2020, 5.6% fewer than were sold in the year to September 2019, with 24.1% less Dairy farms, 14.9% less Grazing farms, 9.3% less Finishing farms and 4.6% less Arable farms sold over the same period.

The median price per hectare for all farms sold in the three months to September 2020 was $26,917 compared to $25,754 recorded for three months ended September 2019 (+4.5%). The median price per hectare increased 4.9% compared to August 2020.

The REINZ All Farm Price Index increased 0.7% in the three months to September 2020 compared to the three months to August 2020. Compared to the three months ending September 2019 the REINZ All Farm Price Index rose 0.7%. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors.

Eleven of the 14 regions recorded an increase in the number of farm sales for the three months ended September 2020 compared to the three months ended September 2019, with the most notable being Canterbury (+27) and Manawatu/Wanganui (+24). Otago recorded the most substantial decline in sales (-6) followed by Bay of Plenty (-2). Compared to the three months ended August 2020, eight regions recorded an increase in sales with the biggest increases being in Bay of Plenty (+6), and Taranaki and Canterbury (+5).

Brian Peacocke, Rural Spokesman, at REINZ says: “As evidenced by the increase in farm sales for the 3 month period ending 30 September, the rural sector continues to reinforce its primary position as being the backbone of the NZ economy.

“The increase in total sales volumes suggests farmers and investors alike are opting for the security of land ownership as opposed to investing in other sectors which have been and are continuing to be impacted by the constraints imposed by the COVID-19 pandemic.

“The median price reinforces the above viewpoint with most categories holding par or increasing slightly, apart from the horticulture sector which continues to grow in value and go from strength to strength.

“Whilst the volatility of early spring conditions with plunging temperatures and late falls of snow have caused losses within late lambing ewes, the accompanying sweep of rain across the country has brought a gasp of relief from farmers in many regions who were “staring down the barrel” of another prolonged dry spell, but have now been given a period of respite, brief or otherwise, only time will tell.

“Product prices, like the weather, also reflect volatility with beef and sheep prices under temporary pressure, but the dairy industry is smiling with news of an increase in the current payout from Fonterra, the major dairy processor in the country, this in spite of some much required restructuring and restoration of its balance sheet.

“Tatua in central Waikato has posted another record payout, and labour issues aside, the horticulture sector continues to exude good health,” he concludes.

Points of Interest around New Zealand include:

- Northland/Auckland - good volumes of sales of finishing and grazing properties albeit a number of those were smaller units with prices reflecting quality; no dairy farm sales; several dairy support/finishing sales in the Auckland region but one interesting sale of a larger scale block planted in manuka within the Thames/ Coromandel district

- Waikato/King Country - light activity in the dairy sector although the 2 sales recorded in the Matamata and Arohena districts reflected strong pricing for their respective localities; a good surge of finishing sales at good levels in the Waipa district but generally quiet in the King Country and Taupo

- Bay of Plenty/Rotorua - strong prices paid for good finishing units throughout both districts; quiet on dairy and grazing blocks but solid activity on horticulture blocks in the Bay of Plenty where the majority of the interest centred on smaller avocado orchards

- Gisborne/Hawke’s Bay - a cross-section of activity in the horticulture and grazing sectors in Gisborne backed up by good solid sales at good prices for finishing units in particular from Wairoa to Central Hawke’s Bay; one deer farm sale west of Napier

- Taranaki - one dairy farm sale plus several strong sales of dairy support and finishing properties in the Stratford and South Taranaki districts

- Manawatu/Wanganui/Tararua - in keeping with the theme throughout the country, a good level of sales with some very strong prices paid for finishing units throughout the western region, with Tararua in the east claiming the lead on sales of grazing properties

- Wairarapa/Wellington - relatively quiet throughout with a light smattering of grazing blocks selling at modest prices

- Nelson/Marlborough - strong activity in the Marlborough district with a good level of prices paid for finishing, grazing and horticulture properties, with some particularly solid results in the latter category; light activity in the Tasman and Kaikoura districts

- Canterbury - one larger drystock sale plus a smaller finishing block in the Hurunui district; some good sales of dairy support, arable and grazing blocks throughout the Selwyn district plus a good level of activity across the board in the Ashburton, Timaru and Waimate districts, that mix including finishing, grazing, horticulture and deer properties

- Otago - almost the quietest period on record with just one sale of a smaller finishing unit recorded

- Southland - energy persists in the deep south with a good sound level of sales of finishing and grazing properties with very good prices paid in both categories – no dairy farm sales yet.

Finishing farms accounted for the largest number of sales with a 31% share of all sales over the three months to September 2020, Grazing farms accounted for 30%, Dairy accounted for 3% and Horticulture accounted for 14% of all sales. These four property types accounted for 78% of all sales during the three months ended September 2020.

Dairy Farms

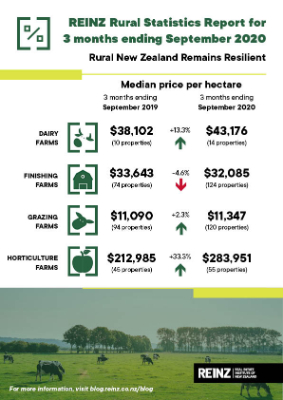

For the three months ended September 2020, the median sales price per hectare for dairy farms was $43,176 (14 properties), compared to $39,030 (12 properties) for the three months ended August 2020, and $38,102 (10 properties) for the three months ended September 2019. The median price per hectare for dairy farms has increased 13.3% over the past 12 months. The median dairy farm size for the three months ended September 2020 was 104 hectares.

On a price per kilo of milk solids basis the median sales price was $33.77 per kg of milk solids for the three months ended September 2020, compared to $31.60 per kg of milk solids for the three months ended August 2020 (+6.9%), and $31.06 per kg of milk solids for the three months ended September 2019 (+8.7%).

The REINZ Dairy Farm Price Index rose 11.8% in the three months to September 2020 compared to the three months to August 2020. Compared to September 2019, the REINZ Dairy Farm Price Index fell 7.5%. The REINZ Dairy Farm Price Index adjusts for differences in farm size and location compared to the median price per hectare, which does not adjust for these factors.

Finishing Farms

For the three months ended September 2020, the median sale price per hectare for finishing farms was $32,085 (124 properties), compared to $32,568 (114 properties) for the three months ended August 2020, and $33,643 (74 properties) for the three months ended September 2019. The median price per hectare for finishing farms has decreased 4.6% over the past 12 months. The median finishing farm size for the three months ended September 2020 was 32 hectares.

Grazing Farms

For the three months ended September 2020, the median sales price per hectare for grazing farms was $11,347 (120 properties), compared to $11,154 (120 properties) for the three months ended August 2020 and $11,090 (94 properties) for the three months ended September 2019. The median price per hectare for grazing farms has increased 2.3% over the past 12 months. The median grazing farm size for the three months ended September 2020 was 99 hectares.

Horticulture Farms

For the three months ended September 2020, the median sales price per hectare for horticulture farms was $283,951 (55 properties), compared to $266,139 (54 properties) for the three months ended August 2020 and $212,985 (45 properties) for the three months ended September 2019. The median price per hectare for horticulture farms has risen 33.3% over the past 12 months. The median horticulture farm size for the three months ended September 2020 was 6 hectares.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention