Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Disney's Streaming Endgame: Will ‘Pam & Tommy’ Appear Next To ‘Lilo & Stitch’? [Parrot Analytics]

The Walt Disney Company rounds out a media earnings season on Wednesday that can charitably be described as ‘mixed.’

Netflix played the expectations game well and its stock seems to have bottomed out for now, but is still down roughly 60% year to date.

Meanwhile Wall Street has reevaluated the prospects of Warner Bros. Discovery and Paramount Global, who are trying to have their cake and eat it too when it comes to both traditional media revenue and streaming growth.

How will Disney fare? CEO Bob Chapek, fresh off a three year contract extension, is about to tell us.

Disney remains the market leader in many key measures of audience demand:

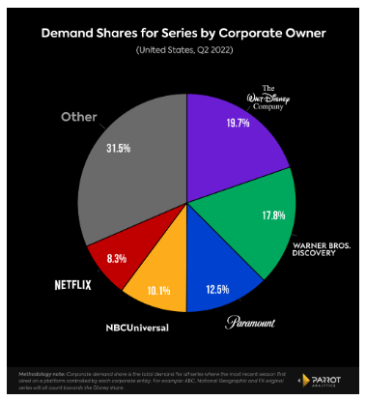

- Disney is number one in US corporate demand share (19.7%), although its lead over second place is smaller than ever following the official merger of Warner Bros. Discovery (17.8%).

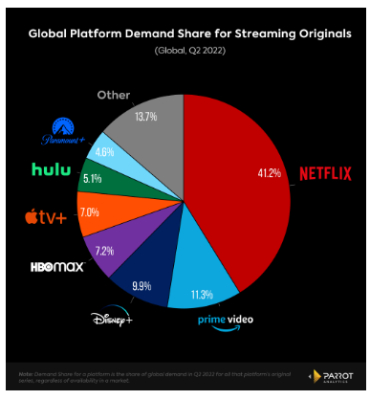

- Disney+’s global demand share grew faster than any other service in the latest quarter (up from 8.8% to 9.9%).

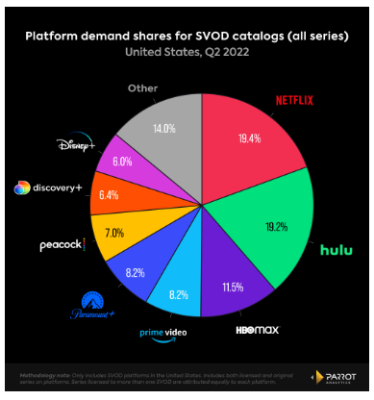

- Hulu (19.2%) is just behind Netflix (19.4%) in on-platform demand share, and a theoretical combination of Hulu and Disney+ (25.2%) would healthily beat out the coming combination of HBO Max and Discovery+ (17.9%) in US on-platform demand share.

All that said, some cracks have begun to appear in Disney’s high growth streaming facade:

- A year ago, Disney+ had four of the five most in-demand streaming originals by US audience demand in the April-June quarter. This past quarter it had two.

- In a show of overconfidence, Disney+ scheduled Obi-Wan Kenobi to debut directly against the fourth season of Netflix’s Stranger Things on May 27. Stranger Things drew several times more audience demand than Obi-Wan Kenobi with both global and US audiences.

- Disney+ pushed back the next Star Wars live action series, Andor, from August 31 to September 21 in order to avoid competing with the debuts of HBO’s House of the Dragon and Amazon Prime Video’s Lord of the Rings: The Rings of Power.

- Losing the Indian Premier League cricket streaming rights will cause Disney’s global subscriber numbers to take a hit.

Disney+’s reliance on franchises — especially Marvel and Star Wars — to drive subscriptions is as strong as ever. These properties will help Disney+ retain much of its sizable subscriber base for the foreseeable future, but it remains to be seen how much more Disney+ can grow without branching out beyond these two franchises.

If Disney+ is to look outside of Marvel and Star Wars for subscriber growth, there is a potential option in house. Which brings us to the biggest question for Disney’s streaming ambitions: what is the plan for Hulu?

The service, including FX on Hulu, has accounted for a steady stream of critical hits with Outstanding demand (top 2.9% of all shows) in the past year such as Only Murders in the Building, The Dropout, Dopesick, Reservation Dogs, The Bear and more.

The Disney bundle is one of the best values available to US streaming consumers, but would it make more sense for Hulu and Disney+ to be folded into the same app ala Discovery+ and HBO Max? Comcast’s minority stake in Hulu complicates plans for that in the immediate future.

Now that Disney+ is already streaming R-rated Netflix Marvel series, should there be less concern about ‘adult’ programming from Hulu appearing alongside more traditionally family friendly Disney fare?

The ultimate question for Chapek and Disney: in order to create a true four quadrant streaming service, do you need Pam & Tommy next to Lilo & Stitch?

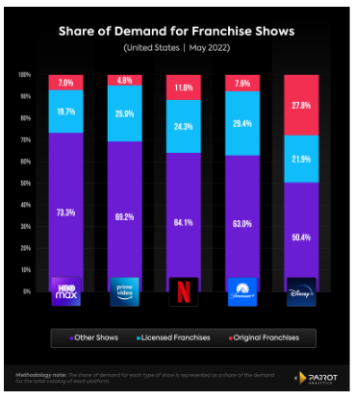

Franchise Demand by Platform

- This breakdown of franchise demand shows how much more reliant Disney+ is on its original franchises — mostly Star Wars and Marvel — than the other streamers are on theirs.

- As of May 2022, audience demand for original franchises accounted for 27.8% of the total demand for TV content available on Disney+, by far the most of any other major platform measured. Netflix was the second highest at 11.6%.

- Disney builds itself around franchises. Its studio divisions practically operate to build out franchises from the get-go. There are plans for sequels if demand is met, and box office sales are high.

- This coincides with consumer products and theme park divisions working those titles into their lineups, with characters being licensed out to video game developers to continue capitalizing on attention.

- Parrot Analytics Director of Strategy Julia Alexander has the full breakdown of what franchises mean to Disney and its competitors.

Corporate Demand Share

- Corporate demand share assesses the long-term viability of the top media companies as they look to consolidate their original content’s availability exclusively onto their own platforms.

- Disney is still in first place here, but the gap between Disney and second place is now the closest we have measured, due directly to the combination of Discovery, Inc. and WarnerMedia’s assets.

- Disney’s corporate share has increased by almost a full percentage point compared to a year ago (18.9%). Considering that corporate demand share changes at a much more glacial pace than originals and on-platform demand, this is a significant increase. However, Disney’s corporate share is still down from 22.1% four years ago.

- As speculation about further media consolidation heightens, it’s worth noting that any hypothetical combination of Warner Bros. Discovery (17.8%), Paramount Global (12.5%), and/or NBCUniversal (10.1%) would create a company that immediately overtakes Disney as the dominant US media company by cross platform TV demand.

Global Originals Demand Share

- Disney+ saw the highest global demand share growth of any streaming service last quarter, moving up from 8.8% to 9.9%.

- Disney+’s global originals demand share has grown 35.6% compared to a year ago (7.3%), and 191% versus two years ago (3.4%).

- Disney+ is one of a trio of

services — along with HBO Max and Apple TV+ — that

accounts for virtually all of Netflix’s global demand

share losses over the last two years.

- From Q2 2020 - the first quarter in which Apple TV+, Disney+ and HBO Max were all available - to Q2 2022, those three streaming services grew their combined global demand share from 10.5% to 24.1%. This 13.6% gain contrasts with Netflix’s 13.8% drop from 55% to 41.2%.

- Hulu and Disney+ would account for 15% in global streaming originals share if combined into the same streamer, which would put them in a healthy second place behind Netflix.

On-Platform Demand Share

- Hulu has consistently been one of the top two services in on-platform demand, due to its massive library catalog.

- While it’s down in eighth place in total on-platform demand, Disney+’s share has grown significantly year over year, from 4.6% in Q2 2021 to 6.0% in Q2 2022.

- Since demand for originals drives subscriber acquisition while library demand helps with retention, Hulu’s leading position in on-platform share alongside Disney+’s strong originals share reveals that the services complement each other well in terms of building a sustainable SVOD model.

- One major theme in the next phase of streaming will be platform consolidation. The on-platform share data provides an early hint of who could be the leaders in this space.

- A combination of Hulu and Disney+ would lead the US market in on-platform demand share (25.2%), well ahead of Netflix (19.4%). The coming combination of HBO Max and Discovery+ would be in third place (17.9%).

Parrot Analytics

Global television demand measurement

Parrot Analytics is the leading global content demand analytics company for the multi-platform TV business. With the world's largest TV audience demand datasets, the company currently tracks more than 1.5B daily expressions of demand in over 100 languages from 200+ countries to reveal the content consumers engage with and watch the most across platforms.

As a trusted partner to some of the biggest media companies and content creators in the world, Parrot Analytics optimises content workflows in real time. The company's TV analytics products result in better production, distribution, acquisition and marketing decisions, as well as accelerated SVOD platform success.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention