Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Chris Sanders: Problems Of The Age Of Order

Sanders Research Associates Ltd. provides international strategic planning and risk management services to both corporate and private clients. SRA also publishes a webzine available by subscription. Visit http://www.sandersresearch.com to get a good feel for the real deal.

Founder’s Comment

Problems Of The Age Of Order

By Chris Sanders

15 June, 2004

© 2003-5. Sanders Research Associates. All

rights reserved.

FROM:

http://www.sandersresearch.com/Sanders/NewsManager/ShowNewsGen.aspx?NewsID=642

Focusing the mind’s eye is for determining impending perils. Events have natural courses, people have successes and failures: it is imperative to examine movements signalling impending perils.

- Thomas Cleary, translator (1993) Thunder in the Sky: On the acquisition and exercise of power, London, Shambhala, ISBN 0-87773-951-X, p. 67

Stopping opponents from adapting

Chinese inflation slowed month on month in May, presumably relieving those analysts who have been fretting about the Bank of China forcing a hard landing on the Chinese economy. Chinese inflation is in any case primarily a matter of food price increases, which if you are not poor and not Chinese is presumably also not a matter for worry. It is impressive that a country as large as China is even capable of producing national inflation statistics on such a timely basis, but then they also are able to produce national GDP numbers on the 31st of December. This seems to us to be a triumph of hope over experience, and confirms what we have long thought about mainstream economics. What is happening may be less important than what people are told is happening.

Click for big version

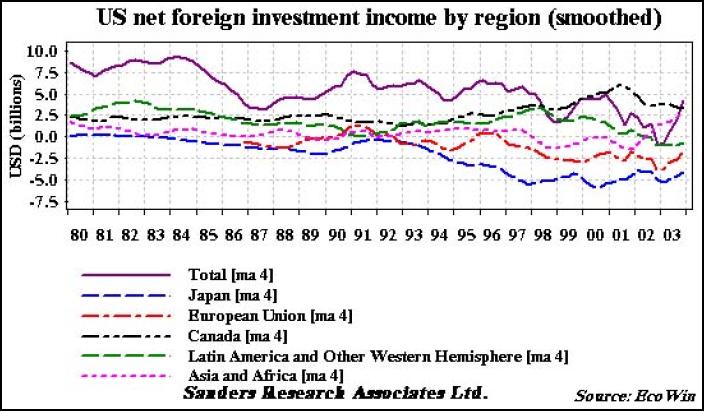

Asian holdings of US government and agency securities continue to climb relentlessly, at a rate of more than 30% per annum. These official flows of capital into the US are basically a reflection of private US flows into Asia. China’s willingness to do this rather than to allow its currency to climb is a result, presumably, of a desire to absorb into the economy the 200 million or so Chinese workers who are either unemployed or seriously underemployed. This is a long term process, not to be rushed beyond the maximum politically sustainable pace. Experience of the last ten years or so suggests that a GDP growth rate of 8% or so has managed to employ an additional 10 million workers a year without igniting a destabilising inflation. Making the heroic assumption that the past is a reliable guide to the future, China needs another twenty years to reposition its labour force and restructure its economy.

It is important to understand some of the usually unspoken assumptions underlying the Chinese “problem.” The first of these is that this is a problem only in the context of globalisation as it is currently understood. This is very much a conceptualisation of the world political economy as a construct of international finance capital. I hasten to add that this does not necessarily invalidate the construct, but it would be dishonest not to acknowledge the enormous profits to be derived from intermediating the international flows of goods and money that are generated by the system as structured. It is not at all clear to us, for instance, that it is a more sensible or “better” use of Chinese savings to invest them in US securities and in so doing finance US purchases of Chinese goods, than it would be to invest them in China directly so that Chinese could purchase Chinese goods. Across the Sea of Japan, we have seen a similar issue unfold over the last twenty years or so. Japan, the world’s second largest national economy, is locked into an export-led model of growth that has made no economic sense from a national perspective at least since 1975. Certainly since 1995 it has made a great deal of sense from an international perspective. Focusing on exports has permitted, indeed required the suppression of domestic private credit growth in favour of government debt expansion and currency intervention to support the dollar and suppress the yen. This has ensured a steady flow of Japanese savings to finance American credit growth.

This gets to the heart of the matter. The other side of Chinese exports is the US willingness to absorb a large part of China’s adjustment by restructuring the American economy away from production by opening its market to Chinese goods produced by labour whose compensation needs to be held in real terms below the rate of profit on the goods that labour is producing. The trade-off for the US is that it gets financing at rates considerably below what it would otherwise have to pay the rest of the world for capital, and enjoys the ability to invest in Chinese projects and share in the profits from that country’s growth. It is thus the “excess” return on investment in China produced by holding real wages in China down that produces the economic quid pro quo that “buys” the necessary offsetting adjustment by American labour.

It is possible to envision this as a relatively smooth and continuous process that proceeds for the necessary twenty years without being fatally disrupted.[i] This may in fact turn out to be the case, but twenty years is a long time in life, never mind politics. That the Chinese are able to maintain the financial and political discipline necessary to hold up their side of the trade is the easiest assumption to make. After all, it will be in China that the biggest excess profits will be made over the period in which their unemployed labour is absorbed, and assuming that the process evolves as planned, it should become politically easier over time. After all, the marginal changes in the life of Chinese labour should be positive. That is the whole point of the exercise.

Unsettling their order

The assumptions underlying the American side of the bargain are less sanguine, we think. The problem is essentially that US workers are being asked, or more accurately are expected, to absorb major economic, social and cultural changes in the way they live and work. These changes for the majority are undoubtedly negative, which raises the question, how long can the US continue to supply markets and investment capital to China? Viewed from the US side of the Pacific twenty years seems like a long time indeed.

Click for big version

The problem from the US side of the ocean is the way the benefits from excess profits growth in China are employed, or more crudely, divided up. This process can be visualised as continuum between two policy choices: either the Chinese can compensate American investors directly or they can recycle all of the dollar proceeds resulting from the difference between the return on their sales to the US and their cost of those sales to the US by purchasing US government debt. The former choice returns all of the benefit in the form of profits to the investors and the latter distributes them more widely to a broader spectrum of American citizens in the form of lower borrowing costs on the national debt.

In reality the actual mix lies somewhere along the spectrum away from the two extremes. But this is a very rough and incomplete characterisation of the political compensation of the US by China for its cooperation in bringing China’s 200 million “surplus” workers into the first world labour force. The truth of the matter is that as China’s real wage (or real exchange rate if you prefer) rises over time, America’s real wage has to fall. This is not the way economists or politicians like to characterise the process, which is usually discussed in terms of one side only. The preferred characterisation is of Chinese wages rising to reach the global real wage. It is seldom discussed in terms of American real wages falling to reach the global real wage. Economic policy needs to be marketed just like everything else.

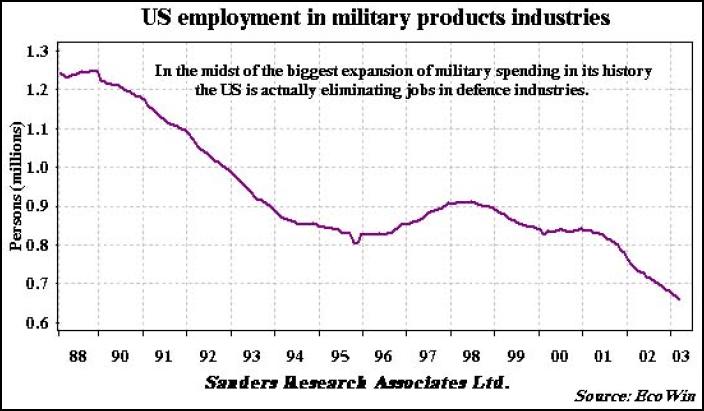

Yet this in fact is exactly what is happening, and can be seen in a host of phenomena from the collapse of manufacturing and even defence related employment in American industry to the massive influx of Latin American labour from south of the border, down Mexico way. And one of the characteristics of this process has not been its continuity, but rather its discontinuities, such as the stock market bubble of the late 90s or the collapse of manufacturing employment in the early 2000s which has reversed fifty years of manufacturing employment gains in just three. The hope that China can smoothly absorb one fifth of a billion workers without a few discontinuities of its own seems to us to be wildly unrealistic, especially considering that this is a country with some of the timeliest economic statistics in the world. In fact so timely are they that they cannot possibly be believable.

Click for big version

This does not appear to bother the statisticians in Peking or their political employers, who understand well the principle articulated above: it is not what you say but how you say it and to whom that counts. The target for information about China is those foreign pension funds that used to prudently shy away from foreign investment in countries where you couldn’t believe the data or count on your day in court, but are necessary to provide the capital with which to take out the early investors in China’s export sector who have made a lot of money but need an exit strategy for when the returns are no longer “excess.”

One of the practical consequences of choosing this policy mix is that Asian real exchange rates need to be held down in order for it to work, which means suppressing the market consequences of surging Asian exports. In the tangible world of things as opposed to the abstractions of theory this has in turn resulted in an explosion of international activity as more and more things are moved over vast distances. Boeing’s announcement last week of the award of two contracts to Chinese suppliers for aircraft components illustrates the point. All this movement means fantastic profits for the middlemen, transporters, financiers and speculators but is difficult to understand from the standpoint of necessity, national security or even economic theory.

And so we come back to the underlying proposition, which is the Chinese “problem.” Given that this is held to be a problem of labour absorption one might have thought it more sensible to use those workers in more labour intensive uses closer to their home rather than wreaking environmental havoc in the interior of China, promoting the export of finished goods to the US from free trade zones on the coast and in the process sparking one of the largest migrations of people in history. As with so many other problems in the Age of Order, this one receives little serious deconstruction no matter how badly needed. Instead, a “problem” is invoked inviting a “solution.” As ever the cost of financing that solution is, as we have seen above, borne by labour. Chinese workers receive lower real incomes than they might otherwise have and so do American workers. It is not China that is providing compensation to the United States but rather some Chinese that are doing a deal with some Americans. Their nationality is, frankly, irrelevant, except as a tool with which to justify the disenfranchisement of the majority who actually produce the source of the wealth that is being traded by the minority.

Great achievement

Heretofore the Americans have bought domestic social and political acquiescence to this program by encouraging one of the most fantastic debt explosions in history. During the Clinton administration this was mostly private sector debt growth, albeit led by agencies backed by the Federal government.[ii] But in the last four years public sector debt has resumed growing explosively. The nature of the fiscal choices underlying this change are revealing: massively regressive tax cuts, hidden regressive tax increases, massive increases in military spending and on “national security” programs, and cuts in all other discretionary spending programs. The effective result has been a transfer of liabilities to the least well off and incomes and wealth to those who are better off. This has the effect of tilting the Chinese quid pro quo to the United States which is financed by lower Chinese real wages to Americans with very high real incomes.

There is a strong case to be made that nationalism is one of the biggest hoaxes to ever be foisted on the producing classes just as ideology is one of the biggest to be foisted on the intellectuals. Like all good hoaxes, these depend for their longevity on the enthusiasm of the hoaxed for the hoax. Americans are arguably amongst the most patriotic people in the world, and also arguably amongst the most grievously mislead. Nor is there much doubt that the intellectuals as a class sincerely believe in the benefits of liberal capitalism which has been “proven” by history to be the most superior social system ever devised by man. Even those who dissent couch their dissent in the language of neo-classical economics; after all, that’s the way one gets tenure.

In our business by contrast it is results that count, and to get results one has to know who is doing what to whom. There is not much ideology in a bread line, and there is not much nationalism in a prison camp.

Chris

Sanders

csanders@sandersresearch.com

[i] For one of the best discussions of the economic issues raised by the Chinese – U.S. relationship read Dooley, Folkerts-Landau and Garber, A Map to the Revived Bretton Woods End Game: Direct Investment, Rising Real Wages and the Absorption of Excess Labour in the Periphery, Deutsche Bank June 2004. The view expressed by the authors is probably the best explication of the economic logic lying behind US and Chinese economic strategy. One can recognise this but still not agree with the strategy. It is not so much the economics of their argument, which is clear enough, but the politics that are consequent to it that are problematic, particularly on the American side. The authors appear to recognise this, hence they explicitly discuss the trade off implicit in different methods of recycling China’s surplus. However they do not appear to agree with the proposition that it is not just a process of Chinese real wages gradually rising over time as it is also a matter of American real wages declining. At least they do not address the issue as such.

[ii] One of the most widely analysed and least understood aspects of the Clinton years is the huge expansion of GSE balance sheets. This amounted, in effect, to the government stoking a housing boom, and the easy money that was both a cause and consequence also stoked a stock market boom. This increased the government’s tax revenues permitting it to begin to pay down its direct liabilities, which encouraged foreigners to allocate investment capital to the US, in turn helping to stimulate the two aforementioned booms. To this day most analysis of the Clinton period focuses on the “prudence” of the Rubin Treasury and its success in bringing the government’s finances under control. In fact, the exact opposite was the case. The price of balancing the Federal budget was an explosion in debt across the economy and a meteoric rise in the government’s off-balance sheet liabilities. During the Clinton years too the last vestiges of prudent financial control and fiduciary responsibility in government were cast aside. “Undocumentable transactions” exploded, growing between 1996 and 2001 to more than $3 trillion. Presumably under the Bush regime the growth in fraud has accelerated thanks to the growth in military spending, but it is impossible to tell since the War on Terror has resulted in such things being classified and the investigations that had been begun in Congress shut down. This should not fool anyone however about the so-called achievements of the Rubin Treasury, which were quite the opposite of those it is credited with.

Peter Dunne: Dunne's Weekly - The Pragmatic Food For Fuel Deal With Singapore

Peter Dunne: Dunne's Weekly - The Pragmatic Food For Fuel Deal With Singapore Eugene Doyle: After Israel’s Brutal Attack On Kiwis, Our Government Does Nothing

Eugene Doyle: After Israel’s Brutal Attack On Kiwis, Our Government Does Nothing Keith Rankin: Has Sweden Become A De Facto Apartheid Narco State?

Keith Rankin: Has Sweden Become A De Facto Apartheid Narco State? Bruce Mahalski: Change In The Weather #194

Bruce Mahalski: Change In The Weather #194 Binoy Kampmark: Dangers To The Fourth Estate - The 2026 World Press Freedom Index

Binoy Kampmark: Dangers To The Fourth Estate - The 2026 World Press Freedom Index Richard S. Ehrlich: Strait Of Hormuz Blockades & Thailand's Land Bridge

Richard S. Ehrlich: Strait Of Hormuz Blockades & Thailand's Land Bridge