Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Growth beyond limits a system requirement, not policy choice

Growth beyond limits is not a policy choice, it is a system requirement

by Lewis

Verduyn

June 27, 2013

The idea that we should pursue economic growth beyond the carrying capacity of our finite Earth is obviously irrational, if not insane. But that is exactly what policymakers are doing. Why?

You may believe that pursuing ever more Gross Domestic Product (GDP) year after year, counting all economic activity as gain, despite the environmental and societal costs, is pointless, immoral, and ultimately suicidal.

And you may despair that governments around the world often ignore heart-felt protests and petitions to save our Earth so that present and future generations may have a life worth living.

It is only logical to say “Let’s stop focusing on growth because perpetual growth is destroying the ecosystems that support life on our finite Earth.” But when it comes to the limits to growth, governments are not logical.

What do policymakers mean

by “economic growth?”

There is a critical

difference between quantitative growth that expands

resource extraction and material consumption, and

qualitative development that improves efficiency and

reduces environmental and social impacts.

“Growth is more of the same stuff; development is the same amount of better stuff (or at least different stuff).” – Herman Daly

Politicians routinely cite the need to grow productivity to generate more jobs. This usually involves more industry, more exports, more highways, more houses, more consumption of everything that adds to GDP.

The fiscal need to grow GDP is never ending, so economic policies are primarily about expansion and intensification. Even when innovation is encouraged, it is often to enable more profitable exploitation of shrinking resources.

Many people suppose that quantitative growth – the production of more stuff, is necessary because of population growth, making quantitative growth the inevitable default policy setting for economies.

Is GDP growth

needed to keep pace with population growth?

This

seems plausible, because more people create more demand, but

the answer is no.

According to UN data, almost all developed nations are reproducing at below replacement level. Europe as a whole has had a declining birth rate for over 40 years. Every country in the European Union, as well as Canada, Japan and China, now has an annual birth rate below the 2.1 children per woman replacement rate.

Germany is at 1.42; France, 2.08; Spain, 1.48; Italy, 1.41; Greece, 1.40; Portugal, 1.51; and Cyprus, 1.46; while the U.K. is at 1.90, boosted by immigrant parents.

The United States, at 2.06, also has a birth rate below the replacement level. Australia is 1.77; Japan, 1.39; and New Zealand is 2.06.

Singapore has a birth rate of 0.79; Hong Kong, 1.11, which will to see its population almost halve in a generation; Taiwan is 1.11; China, 1.55; Thailand, 1.66; Vietnam, 1.87. Even Indonesia is only at 2.20, just above the replacement rate and falling fast. Malaysia and the Philippines are still growing, as are the south-Asian countries, but this is not projected to last more than a few decades.

Birth rates decline in developing nations as living standards improve, with more healthcare, contraception, education, women’s rights, financial security, and so on. Death rates also decline, causing a net increase in population prior to falling.

“The population will peak in 2040 at 8.1 billion people, and then start to decline and continue declining throughout the second half of this century.” – Jorgen Randers, 2052: A Global Forecast For The Next Forty Years (2012)

Why do countries with declining populations need

growth?

As a rule, governments, regardless of birth

rates, are committed to policies that promote

quantitative growth and consumption.

European Union member nations, the United States, and Japan, all have stable or declining populations, and yet policymakers in these countries are desperately attempting to revive growth in their stagnating economies.

Having a falling birth rate impedes economic growth. An ageing population with fewer young people means less demand, less consumption, less tax, and less GDP.

It seems perverse that despite global population overshoot, many governments now offer incentives for couples to have children, and some use immigration as a means to grow their population, in order to grow their consumption, in order to grow their GDP, in order to reduce their debt to GDP ratio.

So, economic growth is not needed to serve population growth, but vice versa.

Is

conventional economics driving population

overshoot?

It is estimated that developing nations

have 80% of the world’s population and generate 96% of the

population growth. These nations are beginning the

demographic transition to lower birth rates as their

living standards gradually improve.

Therefore, poverty reduction to reduce birth rates is the key to lowering peak population. This hastens the demographic transition to lower birth rates, reducing both the level and duration of resource demand during the transition.

Lowering birth rates would obviously improve global food, water, and energy security.

But our financial system is geared to increase poverty through debt. Furthermore, neoliberal “free market” policies, since the 1980s, have accelerated the debt-poverty machine, hollowing out the incomes of the middle and lower classes, and worsening population overshoot in the poorest nations.

Everywhere, wealth is constantly transferred upward via the interest mechanism.

In the O.E.C.D., income inequality has soared to record levels in recent decades. In the United States, from 1979 to 2007, about $1.1 trillion was transferred to the top 1% of Americans, more than the entire income of the bottom 40%.

Ironically, The World Bank’s bi-line is “Working for a World Free of Poverty”.

Why are governments obsessed with growing

ever more GDP?

The answer is the debt-money system,

or to be specific, debt measured against GDP. Rising debt is

the fiscal motivation for economic growth.

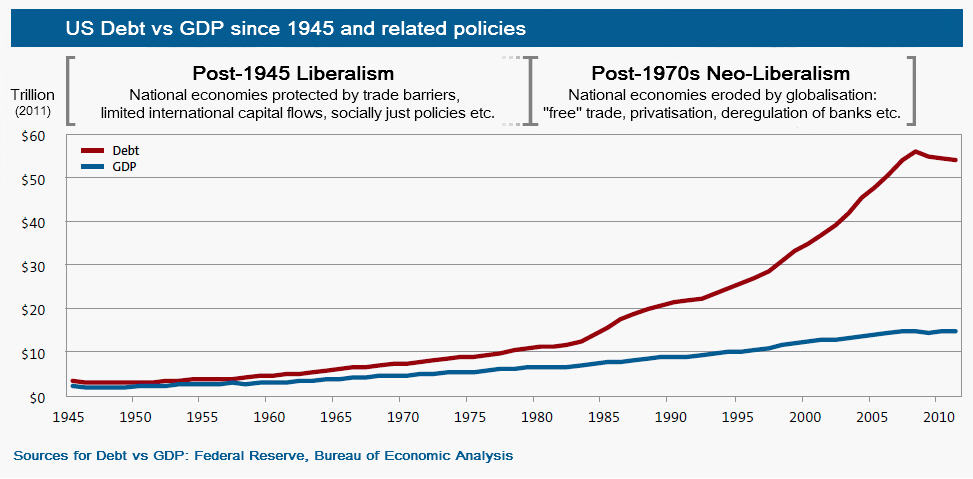

After WW2, from 1945 until the 1970s, growth was so rapid that GDP was sufficient to more or less control debt, while poverty generally receded. “Growth” was therefore the goal of every government. However, the basic pre-conditions for such growth, abundant fossil energy and expanding consumer demand, have been declining for decades. The pre-conditions have changed, but the “growth” policy has not.

Although neoliberals have found new ways to boost corporate growth, by promoting trade deals that allow more access to foreign wealth, and by easing international capital flows, this has only fast-tracked environmental decline and sovereign debt.

Financial deregulation vastly increased debt by allowing runaway gambling in real estate markets and a plethora of derivative instruments, prior to the 2008 crash.

Click for big version.

(See graphic for correlation between US debt to GDP and related policies.)

The pursuit of GDP to settle debt

is futile and destructive

So we just need to grow

more GDP, right? Wrong, because total global debt has

already exceeded global GDP (about $83 trillion in 2012),

many times over.

All debt is a promise to deliver something of real value from our limited physical world, and therefore a system of ever expanding debt is nonsense.

“The monetary economy … is a social invention not constrained by the physical laws of the planet.” – Limits to Growth: The 30-Year Update (2012)

GDP serves the growth-based monetary system of interest-bearing debt, which is divorced from reality, placing impossible claims on the future, like a cancer on all life.

Servicing interest-bearing debt demands exponential growth in GDP, rapidly depleting finite resources – for example, a goal of 3% GDP growth means that the productive economy must double every 24 years.

We simply haven’t got enough planets to exploit. Next, there will be pressure to mine Antarctica, the ocean floors, even the moon and asteroids.

Not only is the pursuit of GDP to settle debt an exercise in futility, GDP is a false measure of economic success. GDP was never intended to measure national welfare.

Designed in the late 1940s to gauge the military capability of economies, GDP makes no distinction between good and bad outcomes. In terms of growing GDP, even weapons sales and wars can be effective strategies.

In many ways, GDP is an indicator of Greed, Destruction, and Pollution.

Why does the

debt-money system require endless growth?

Only about

3% of a nation’s money is created by the government, as

notes and coins. The rest is created digitally by private

banks, out of nothing, when they issue “loans.” Banks do

not lend reserves or customer deposits.

"When banks extend loans to their customers, they create money by crediting their customers' accounts." – Mervyn King, Governor of Bank of England (2012)

The private debt-money system has three fatal defects:

Firstly, the interest mechanism systemically transfers wealth upward, increasingly enriching the minority at the expense of the impoverished majority.

Secondly, the banks create about 97% of the money supply as debt, which when repaid shrinks the money supply and the economy. So the economy depends on the constant creation of new debt, without which the loss of money leads to a recession.

Thirdly, the banks do not create the interest, which must be serviced with the creation of more debt. The interest is a negative phenomenon that compounds over time, requiring the creation of ever more debt to service ever more debt.

The system depends on growth to function, for the simple reason that interest is added to debt. To service exponential interest-bearing debt, the system must continually expand, violating the laws of nature.

The debt-money system has been likened to a ponzi scheme.

“Due to the requirement for interest payments, debt-based currency can only function well in an expanding economy.” – Richard Heinberg, The End of Growth (2011)

Individually, we may pay off our debts, but collectively we must always be in debt to the banks. Debt servitude is "the system."

Naïve politicians sometimes urge us to save money to reduce our debts, and yet all money in savings accounts also represents debt somewhere in the system. They also urge us to spend only what we earn, i.e. stop borrowing and live within our means, but if we all did that, most of the (debt) money supply would disappear!

The two modes of the system are

growth and collapse

Despite the evident

failure of growth-based policies, economists and

policymakers blithely talk about a “recovery” midst a

global scramble for resources in a race to the bottom of the

barrel.

“Even though the benefits of further growth

are now less than the costs, our decision-making elites have

figured out how to keep the dwindling extra benefits for

themselves, while 'sharing' the exploding extra costs with

the poor, the future, and other species. The elite-owned

media, the corporate-funded think tanks, the kept economists

of high academia, and the World Bank — not to mention Gold

Sacks and Wall Street — all sing hymns to growth in

perfect unison, and bamboozle average citizens.” –

Herman Daly

Like deadly Pied Pipers, the growth junkies

are leading us to destruction.

The conundrum of neoclassical economics is that the debt-money system only has two modes of operation, growth and collapse, usually referred to as boom and bust.

The first mode, growth, depends on ever more people producing and consuming ever more stuff. The second mode is the failure of the first.

In the present debt-money system, policymakers have no option but to pursue growth. Basically, their toolbox allows them to either shrink or expand the debt-money supply.

Which suicide policy do you prefer: public austerity or private stimulus?

Austerity shrinks the

spending power of the people

Government austerity

policies involve cutbacks on spending and borrowing. This

reduces the money supply circulating in the economy, which

reduces the demand for goods and services, which reduces

employment. Poverty increases along with the demand for

social services. Commodity prices weaken as consumption

declines, and even large businesses become vulnerable.

A shrinking money supply deflates the economy, leading to defaults, foreclosures, bankruptcies, unemployment, depression, and, historically, social unrest and war.

Nobel prize-winning economist Joseph Stiglitz recently described European Union austerity plans as a “suicide pact”.

Less obvious, is that neoliberals are using austerity to force down wages, strengthen corporate power, and launch a second wave of privatisation through public asset fire sales. Privatisation is a core requirement of austerity plans.

Neoliberal governments, committed to expanding the private sector, are selling off public assets at bargain rates, and further opening up their economies to exploitation by transnationals in exchange for a debtor’s hand-out, sacrificing environmental protections and sovereign freedoms.

Stimulus expands the gambling power

of the brokers

Quantitative easing (QE) is meant to

stimulate growth in the economy by adding to the money

supply. Central banks create new money to buy up toxic

financial assets, such as long-term government bonds and

junk mortgages, from too-big-to-fail-banks and other private

institutions.

QE expands the liquidity of the banks, providing the elite managers, bondholders and brokers with more funds with which to speculate in shares and commodities, raising their stock portfolios. The QE is “base money” added to bank reserves, which are loaned between banks, but never actually loaned to the public. The result is a net loss of credit to the economy. This explains why $3 trillion of QE in the United States has not caused hyperinflation, and why it does not benefit the government, most businesses, or the people on the streets.

The result is a growing unproductive financial sector becoming more decoupled from the productive economy, which is starved for currency and beset with unemployment, while CEO’s collect outrageous bonuses.

Stimulus, to actually be effective, must deliver circulating money to the people in the productive economy. This was the original intention of QE as proposed by the inventor of the term in the 1990s, U.K. Professor Richard A. Werner.

A “recovery” for the

7%, and a depression for the 93%

The overall global

trend is declining growth, while in the United States 93% of

households are losing net worth.

Growth policies are driving a two-tier economy; one serving the wealthy elite who play the markets, while the other bleeds the majority and expands poverty.

“From the end of the recession in 2009 through 2011 (the last year for which Census Bureau wealth data are available), the 8 million households in the U.S. with a net worth above $836,033 saw their aggregate wealth rise by an estimated $5.6 trillion, while the 111 million households with a net worth at or below that level saw their aggregate wealth decline by an estimated $600 billion.” Pew Research, An Uneven Recovery, by Richard Fry and Paul Taylor.

During the so-called US “recovery” from June 2009 through 2011, the wealthy gained 28% in their net worth, while everyone else lost 4% of their assets.

The banking sector made record profits before the crash in 2008, and is again making record profits in the post-crash Great Recession economy.

Is the

debt-money system a banker’s welfare scheme?

Yes.

Whether or not economies grow or collapse, the banking

sector always wins.

During boom times when banks create money as debt, the interest mechanism automatically transfers wealth upward from those who have the least to those who have the most, widening the gap between the rich and the poor.

And during a bust, when mortgagees default and businesses go bankrupt, the banks foreclose and pocket the assets. Even when the too-big-to-fail-banks collapse, the financial elite are rescued by bail-outs or bail-ins.

So the banks expand the money supply during a boom, and shrink it during a bust, which is the reverse of what a healthy economy needs.

The debt-based financial system primarily serves the welfare of an autocratic banking cartel. They maintain their power because they have captured the state's sovereign money, turning it into debt with interest. The power equation is: money scarcity equals dependence equals control.

The system is designed to protect the money masters who created it. The golden rule is that those with the gold make the rules. Or to be more blunt, the masters of the debt-money system pull the strings of puppet governments.

Market and government manipulation, once insidious, now occurs openly in defiance of the rule of law. So far, fraudulent banksters are too-big-to-jail.

Forget “growth”, economies need

permanently circulating money

The obsessive pursuit

of growth, under policies of austerity or stimulus, or any

combination thereof, will only worsen every global

crisis.

The “growth” dogma is so embedded that even well-intentioned analysts overlook the underlying imperative for perpetually expanding GDP – interest-bearing debt.

The death-grip of the private central bankers on the economy is seldom questioned, despite the critical failure of their debt-money system to provide a permanently circulating medium of exchange.

“We are absolutely without a permanent money system... It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon.” – Robert H. Hemphill

Simply, an economy is a body of exchange, and money is its circulating blood, without which its life can only fail and wither.

The monetary lifeblood of a nation – not itself a commodity, is the intermediary that allows the people to trade goods and services of value.

A nation’s money is backed by the “full faith and credit” of the people. Sovereign governments have always had the authority, vested by the people, to issue public money debt-free and interest-free.

Public money is the domain of a sovereign nation.

Survival within limits depends on an economic

“steady state”

Populations in most developed

countries are relatively stable, and the world overall is

moving toward a peak population followed by a decline.

Our civilization is on the brink of multiple collapses; financial, energy, climate, water, food, and biosphere. We have an enormous programme of work ahead in order to adapt our lifestyles to a saner world of less, but ample.

“Economic growth as we have known it is over and done with.” – Richard Heinberg

What is missing is a stable, sustainable, and democratic money system, necessary for our evolution to a steady state economy.

The modernisation of money is a taboo subject among economists and policymakers rooted in the narrow orthodoxies of the IMF private banking system.

But those who understand that economics must be consistent with the real world in order to succeed are being heard more often midst the mounting failures of austerity and QE.

One of the most influential financial policymakers in the world, Adair Turner, chairman of Britain’s Financial Services Authority, in a speech on February 6, 2013, advocated the public issuance of money. His recommendation was backed by a 75-page paper explaining why public debt-free and interest-free money, created for citizens and governments, would restore economic health without leading to hyperinflation.

Governments are

failing in their duty to serve the people

A

freely-elected government is instituted by the people to

serve, not rule.

Such governments derive their authority from the sovereign people, whose power is the source of law. As a Public Trust, its public officers are trustees with a fiduciary duty to serve the private people according to their public Oath of Office, being sworn to uphold the law of the land, protecting justice and life.

Centuries of monetary, legal, and political manipulation, have deeply subverted governments, establishing a global financial oligarchy at the expense of the people and the planet.

So entrenched is this psychological control, that people living in common law nations almost entirely forget that their legal fiction governments still operate under the lawful de jure jurisdiction of the people.

Our government public servants depend for their authority, in all statutory matters, upon the willing consent of each and every man and woman. Our singular right to contract is inviolable.

By relinquishing the public’s monetary power to the private bankers, our government is failing in its fiduciary duty. We are, in effect, being constitutionally betrayed by our disobedient servants.

Government policymakers, having revealed their corporate colours, are now engaged in a deadly economic experiment to revive growth at any cost.

Mass impoverishment, and unemployment exceeding 50% among the youth of some debt-ruined nations, can only lead to a more dangerous crisis.

The perpetual growth of GDP is not a policy choice – it is a systemic requirement to service interest-bearing debt, and a prescription for economic and environmental collapse.

Interest requires “growth”, forever.

“And this term interest, which means the birth of money from money … of all modes of getting wealth this is the most unnatural.” – Aristotle 325BC

Lewis Verduyn is a researcher of neo-classical economics, monetary history, corruption, and jurisprudence.

Binoy Kampmark: Show Me The Money - A Loutish Administration Confronts A Craven Congress

Binoy Kampmark: Show Me The Money - A Loutish Administration Confronts A Craven Congress Ian Powell: Do Wellington Floods, Climate Change And Wealth Accumulation Equal “Suicidal Capitalism”?

Ian Powell: Do Wellington Floods, Climate Change And Wealth Accumulation Equal “Suicidal Capitalism”? Ramzy Baroud: The Pendulum Swings - The Slow Death Of Europe’s Pro-Israel Consensus

Ramzy Baroud: The Pendulum Swings - The Slow Death Of Europe’s Pro-Israel Consensus Dr Nasim: Poem From Gaza - Her Smile

Dr Nasim: Poem From Gaza - Her Smile Keith Rankin: New Zealand's Dependence - Wheat, Rice, Fuel, Ships

Keith Rankin: New Zealand's Dependence - Wheat, Rice, Fuel, Ships Peter Dunne: Dunne's Weekly - Luxon/Peters Spat Just Part Of Peters' Ongoing Plan

Peter Dunne: Dunne's Weekly - Luxon/Peters Spat Just Part Of Peters' Ongoing Plan