Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

The OCR Should Be Cut

The Reserve Bank Monetary Policy Committee releases its next Monetary Policy Statement and Official Cash Rate (OCR) decision next Wednesday – the first we’ve heard from them since November.

Until a couple of weeks ago you could probably mount a pretty strong case for the status quo. If the MPC was right to have left the OCR unchanged at 1 per cent in November, it probably looked as if that was still going to be the right decision in February. I thought they should have cut in November, and so was still inclined to think they should cut now – but it wasn’t a particularly strongly held view. It is worth remembering that after all these years, the Bank’s favoured core inflation measure still isn’t back to 2 per cent (it was last there in 2009) and there wasn’t a lot in the wind suggesting it was likely to rise further. But there hadn’t looked to be a lot in it.

The Reserve Bank’s Survey of Expectations, released at 3pm today, looks to be not-inconsistent with that sort of status quo story. But the survey closed a week ago, and opened two weeks ago – the Bank doesn’t tell us when responses came in, but I know I completed mine on 25 January.

Since then coronavirus has become a huge story. From an economic perspective, the issue isn’t so much the number of deaths – 50 or so in total two weeks ago and 640 now, on official figures – as the policy and personal responses, here (and in other similar countries) and in China. Two weeks ago, perhaps optimists might have hoped a one week shutdown over Lunar New Year might break the back of the problem. But then, of course, ever more cities in China were locked down, the PRC authorities banned most outbound tourism, countries starting putting restrictions on arrivals of non-citizens who’d been in the PRC, and finally New Zealand – apparently dragged along by Australia – banned the arrivals of anyone other than citizens (and their close family members) who’d been in China recently. We’ve also seen dairy product prices falling, talking of serious disruption in the logging industry, and so on. We’ve even seen some more-domestic effects, including the cancellation of the Lantern Festival in Auckland. Oh, and there seems to be no sign in the PRC responses that suggests they think they’ve already got on top of the problem.

No one knows how long these effects will last, or whether things may yet get (perhaps materially) worse from here (I was talking to a journalist the other day about possible extreme scenarios, and it doesn’t really do to contemplate what would happen to world trade – perhaps only for a short period – in such scenarios).

When I say ‘no one”, that of course includes the Monetary Policy Committee, who will have not a shred more information on the underlying situation – and probably very little more on domestic economic effects – than you, I, or anyone else. Any data available just yet – perhaps daily air arrivals, or electronic transactions volumes in (say) Queenstown – will be fragmentary at best, and there won’t even be new local business survey data for a few weeks. So they have to work with what we know, perhaps how things would be likely to play out if the policy responses (here and abroad) remain much as they are for any length of time, and within a framework for thinking about risk and regret.

All of which looks a lot like the classic sort of shock monetary policy is designed to help manage (lean against). Aggregate demand in New Zealand will take a not-insignificant hit: tourism and export education from the PRC is about 1 per cent of GDP, and tourist numbers will dry up almost completely for now, and (if our numbers are similar to those in Australia) the export education numbers are likely to more than halve.

Would be good if MBIE/Min of Ed published comparable NZ numbers

"Aus. Dept of Education figures..show more than 106,680 Chinese international students with visas to study at universities and schools remain stuck outside Aus – 56% of the entire cohort."https://t.co/JjwMsmsoET

— Michael Reddell (@MHReddell) February 6, 2020

These effects might not last long, but they are the situation we face now and no one has any idea how long the adverse effect will last.

But these aren’t the only demand effects. Australia and the PRC are our two largest overall export markets: economic activity in China is likely to have taken a substantial hit this quarter, and Australian universities are (for example) even more dependent on the PRC student market than the New Zealand ones are.

And how would you respond to uncertainty if you were in business, or were (for example) a lending institution. The rational response is to put projects on hold where possible. That seems likely to happen – perhaps on a very small scale initially (few new projects start each week, but mounting as the situation becomes more protracted (and perhaps doubts grow about just how quickly business might rebound).

Also, although the focus to date has been on services exports (tourism and export education), and a couple of goods export sectors, even if goods can be still shipped out to China, you have wonder how soon the flow of imports is going to be affected – people who’ve been in China in the last 14 days can’t enter Singapore, Australia, PNG, Fiji, Taiwan or…..New Zealand (and, I understand it, much of New Zealand’s trade is trans-shipped through Australia or Singapore). Ships need sailors.

I don’t know what the Reserve Bank will have chosen to do about their formal economic forecasts. In their shoes, I’d probably publish ex-coronavirus forecasts, and then a series of scenarios around coronavirus effects (what else can they do: they usually treat other policies as a given, and in this case the ban of people who’ve visited the PRC is scheduled to lift next Sunday, but I doubt anyone much expects it will be, and more importantly neither they nor anyone else can credibly forecast the path of the virus, including how its is beginning to spread outside China).

But whatever they do in the body of the document is much less important than the policy call they make. This is the time to cut the OCR. perhaps even by 50 basis points. It would be a mix of risk-mitigation and responding to a real loss of demand (very rarely do we see such hard early evidence of a specific source of demand drying up so quickly).

The standard counter-argument is something along the lines of “early days”, “likely to rebound quite quickly – eventually”, and so on. But here is the thing about monetary policy: it can be adjusted quickly (to cut and to raise); it is the tool designed for short-term macro-stabilisation (unlike fiscal policy) and some of the channels – notably those to the exchange rate – work really quite quickly. I’m not suggesting that cutting the OCR would make more than a trivial difference to GDP in the March quarter (the tourists and students still won’t have come), but if the effects are any longer-lasting we would start to see the benefits.

Twice before the Reserve Bank has cut the OCR is response to truly-exogenous external events. The first was the unscheduled 50 basis point cut in September 2001 (a week or so after the terrorist attacks). Here was the case we made then

“It seems more likely now that the current slowdown in the world economy will worsen. In these circumstances, New Zealand’s short-term economic outlook would be adversely affected, although any downturn might well be relatively short-lived.

“New Zealand business and consumer confidence will be hurt by recent international and domestic developments, and today’s move is a precaution in a period of heightened uncertainty.

I still reckon that was an appropriate response at the time, even though we had (a) no new survey or hard data, (b) there were no foreign or domestic government restrictions which would have the direct effect of biting into domestic demand in New Zealand and (c) the exchange rate – already low – was by this point almost 5 per cent lower than it had been on 11 September. It was explicitly precautionary, but in a climate where our best judgement told us that if there was any effect it was going to be adverse (disinflationary).

The second such 50 point cut was in March 2011, after the severe February earthquake. As the Governor put it at the time

“The earthquake has caused substantial damage to property and buildings, and immense disruption to business activity. While it is difficult to know exactly how large or long-lasting these effects will be, it is clear that economic activity, most certainly in Christchurch but also nationwide, will be negatively impacted. Business and consumer confidence has almost certainly deteriorated.

Going on to observe

We expect that the current monetary policy accommodation will need to be removed once the rebuilding phase materialises. This will take some time. For now we have acted pre-emptively in reducing the OCR to lessen the economic impact of the earthquake and guard against the risk of this impact becoming especially severe.”

We knew that the longer-term impact of the earthquake would be a big positive boost to demand (all that rebuilding activity, which would crowd out other activity in time) but still concluded that it was appropriate to cut early and quite hard to lean against adverse confidence effects etc (and some direct adverse demand effects – eg to South Island tourism). Perhaps we just got lucky, but it still looks like an appropriate response to me, even with years of hindsight.

In June 2003, SARS also played a role in the Bank’s decision to cut the OCR then. I wasn’t involved in that decision – I was working overseas – so don’t have as strong a sense of the balance of factors. One can mount an argument that it was unnecessary to have cut – the Governor eventually concluded as much – but much of that argument was with the benefit of a hindsight that real-time decisionmakers could not have had (about how quickly the virus would be contained).

Set against the backdrop of those three cuts, I reckon the case for an OCR cut now – even it had to be pullled back in six months’ time – is stronger than in any of those other cases. We have clear adverse domestic demand effects, that aren’t just about confidence but about policy choices in China and in New Zealand (and, more peripherally, in other countries), we don’t just have a one-day event which we live with the aftermath of (rather an ongoing situation, which is probably still worsening), the epicentre of the issue is in the world’s largest or second-largest economy which itself is taking a large negative economic hit for now, and Australia – our other main trading partner, and major source of investment – faces very similar issues to New Zealand.

Against that backdrop, it isn’t obvious what the downside would be to an OCR cut next week. Core inflation is still below the target midpoint, and yet the demand shock is adverse. Perhaps things resolve themselves very quickly in a couple of months and the Bank is slow to pull back the OCR cut. The worst that could happen then might be core inflation going a bit above 2 per cent. But since 2 per cent isn’t supposed to be a ceiling, and we’ve haven’t even been to 2 per cent in the last decade, that might count as a gain not a loss, in terms of supporting core medium-term inflation expectations.

Then, of course, think about really bad scenarios, and a world with very limited fiscal and monetary policy capacity to respond to a serious downturn. It really is important to keep those expectations up. Recall that that was one of the stories the Reserve Bank told for a while after the unexpected 50 basis point cut last August.

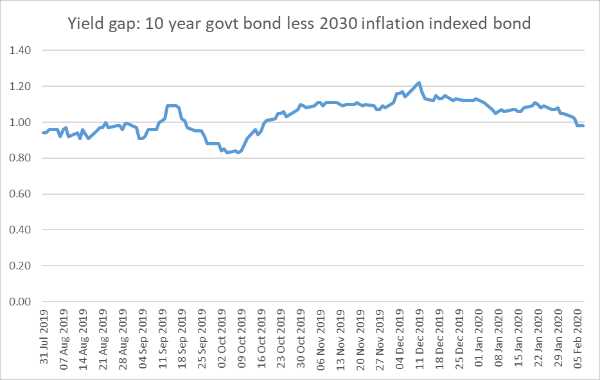

But here is the implied inflation expectation measure from market prices, right up to today (the difference between yields on nominal and indexed 10 year government bonds)

There was a bit of lift in this measure of implied expectations late last year (partly global, but a range of central banks were responding similarly). But now we are pretty much back to where we were before the Bank cut the OCR unexpectedly sharply six months ago (and this even after bond yields have bounced off their lows earlier this week). I guess we should take some comfort that implied expectations aren’t lower than those in August, but 0.98 per cent is a long way from 2.

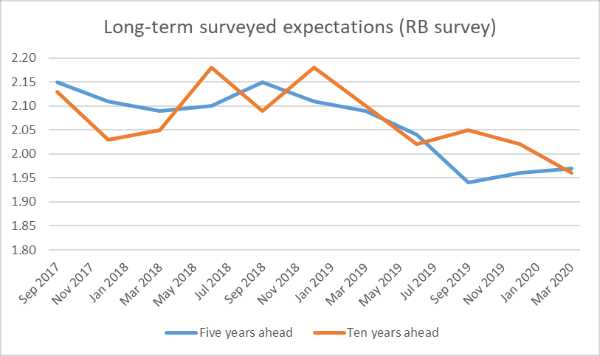

And as one last straw in the wind, in 2017 the Bank (helpfully) added a couple of questions asking about respondents expectations for inflation five and ten years hence. The answers have hewed pretty close to 2 per cent – I usually put in 2 per cent for 10 years hence, noting that the current MPC/government won’t have any effect on those outcomes – but when I opened the survey results today I noticed that even these expectations (which the Bank likes to boast of, as a sign of confidence) have been edging down.

The differences are small, and in isolation I wouldn’t put much weight on them. But not much is moving in the right direction, and these results were surveyed two weeks ago when most respondents thought the policy status quo was just fine for now.

It seems a pretty obvious call to me that they should cut on Wedneday – absent some startling positive turn in the virus and related news between now and Wednesday morning – rather than just idly handwringing about “watching and waiting”. And the Governor/MPC was willing to make some big and unexpected calls (wisely or not) last year. The Bank wouldn’t be the first central bank to move either.

Who knows whether or not the Bank will actually move on Wednesday – quite possibly not even them yet – but I’m sure the MPC will have been looking for some analysis of past responses to out-of-the-blue shocks and thinking about the similarities and differences here. Whichever path they finally choose, that thinking should be laid out – not just noted – in the MPS and/or the minutes.

Originally published on Michael's blog Croaking Cassandra here Binoy Kampmark: Ted Turner - The Devil Behind Cable News

Binoy Kampmark: Ted Turner - The Devil Behind Cable News Keith Rankin: Clipping The Ticket; Solving Hormuz, In Context

Keith Rankin: Clipping The Ticket; Solving Hormuz, In Context Ian Powell: Inhumanity Of US Economic Sanctions Against Cuba – Infant Mortality And Starvation; Time To End NZ’s Silence

Ian Powell: Inhumanity Of US Economic Sanctions Against Cuba – Infant Mortality And Starvation; Time To End NZ’s Silence Ramzy Baroud: Subjects Of Empire - Breaking The Cycle Of Arab Dependency On US Elections

Ramzy Baroud: Subjects Of Empire - Breaking The Cycle Of Arab Dependency On US Elections Peter Dunne: Dunne's Weekly - The Pragmatic Food For Fuel Deal With Singapore

Peter Dunne: Dunne's Weekly - The Pragmatic Food For Fuel Deal With Singapore Eugene Doyle: After Israel’s Brutal Attack On Kiwis, Our Government Does Nothing

Eugene Doyle: After Israel’s Brutal Attack On Kiwis, Our Government Does Nothing