Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Explaining New Zealand’s Flawed Anti-Money Laundering Laws

Asia Pacific AML, Kerry Grass

At the 1989 Heads of Government G7 summit, the world leaders spoke about their increasing concern from the rise in drug trafficking and the resulting money laundering that was occurring through the international banking system. At paragraph 52 of their published Economic Declaration, the G7 leaders declared:

The drug problem has reached devastating proportions. We stress the urgent need for decisive action, both on a national and an international basis. We urge all countries, especially those where drug production, trading and consumption are large, to join our efforts to counter drug production, to reduce demand, and to carry forward the fight against drug trafficking itself and the laundering of its proceeds.

The G7 Leaders concluded the 1989 Summit by setting out various measures to manage these new and evolving risks. One of these measures was to establish a ‘task force’ to assess ‘member countries’ in their efforts to prevent the banking system and financial institutions, being utilised for the purpose of money laundering. It was at this time or shortly after that the Financial Action Task Force came into existence.

Less than a year after its creation, the FATF published 40 Recommendations. In setting its recommendations, the FATF encouraged G7 member countries, as well as other countries, to adopt these preventative measures.

The FATF 40-Recommendations became the international anti-money laundering standard.

Following the 9/11 attacks on US soil in 2001, the FATF increased its mandate to include ‘terrorism financing’. This resulted in an additional 9 ‘Special Recommendations’. Consequently the FATF 40 Recommendations became known as FATF 40+9.

New Zealand’s History With FATF Recommendations

New Zealand joined the FATF as a member country in 1991 and on 1 April 1996, introduced its first law to regulate money laundering.

Known as the Financial Transactions Reporting Act 1996 (the FTR Act), it applied to registered banks, lawyers, accountants, real estate agents, trustees, stockbrokers and more.

New Zealand Has Its First FATF Country Inspection

In September 2003, the FATF commenced the first country inspection of New Zealand’s AML/CFT regime and identified significant deficiencies.

These non-compliant ratings to core FATF Recommendations included: (a) a lack of mandatory supervision of captured businesses, (b) not capturing all businesses covered in the FATF Recommendations, (c) the absence of a requirement to implement AML/CFT systems like customer due diligence and (d) identity verification did not set minimum standards.

Whereas other countries had set legislative standards of ‘identity verification’, such as using passports, birth certificates, driver license etc, NZ was not on par.

Not identifying customers and not knowing who are the true owners of a bank account, is a significant exposure to either unknowingly or being wilfully blind to facilitating transnational crime, organised crime, corruption, fraud and the list goes on.

IMF Publishes NZ Country Report 2005

On 12 August 2005, the International Monetary Fund (the IMF) published a ‘Country Report’ of New Zealand’s status (the FATF 2005 Report).

The FATF 2005 Report detailed –

The experts reviewed the relevant AML/CFT laws and regulations and the supervisory and regulatory systems in place to deter money laundering (ML) and financing of terrorism (FT) among financial institutions. The experts also reviewed the regulatory systems in place for casinos as well as the capacity and implementation of all these systems. The evaluation team met with officials from the relevant NZ agencies from 20 – 24 October 2003.

The main sources of illegal proceeds are considered to be the cultivation, manufacturing or dealing in illicit drugs, traditionally cannabis, but more recently methamphetamines. Fraud offences have also produced significant proceeds.

Money laundering techniques range from unsophisticated cash payments for assets to complicated corporate transactions involving a number of transactions through companies and financial institutions both in NZ and overseas.

Apart from misuse of the banking system and the purchase of real estate, significant actual and potential trends in money laundering methods have been seen in the area of casinos (both local and foreign patrons), the misuse of trust accounts belonging to professional intermediaries such as accountants and lawyers, and alternative remittance agents operating in different parts of the country.

Alternative remittance agents (who use the formal sector to remit funds) are regarded as being a higher risk sector because of poor compliance with the customer due diligence and reporting requirements of the FTRA.

No evidence of an underground banking system, such as “Hawala”, has been found.

No evidence of terrorist financing activity has been uncovered.

Under the heading ‘Main Findings’, the 2005 IMF Report informed –

Since its last evaluation in 1998, NZ has made few changes to its AML regime.

Customer due diligence measures need to be amended to introduce appropriate requirements to properly identify third parties for whom a customer is acting.

Appropriate mandatory requirements also need to be introduced concerning financial institutions and their internal controls and measures to prevent their control or acquisition by criminals.

Most importantly, an effective system needs to be introduced to supervise and/or monitor the compliance by relevant financial and other institutions with their AML/CFT obligations.

The New Zealand Financial Intelligence Unit (FIU) is established within the NZ Police (NZ Police FIU).

The NZ Police FIU receives, analyses, and disseminates suspicious transaction reports (STR) and other relevant information, as well as, intelligence concerning suspected ML and FT activities. STR are required to be sent in the prescribed format, usually by post or fax.

Since 1997, the NZ Police FIU has had an established staff of three.

The NZ Police FIU requires additional resources to adequately perform its core FIU functions i.e. receipt, analysis and dissemination of STR, as well as give input into other issues such as revised guidelines.

The number of STRs received by the FIU has trebled over the past five years, with nearly 3000 STR being received in 2002.

While relevant data is recorded on a database and analysed by the NZ Police FIU, the functionality of the database is very limited and the retrieval of these statistics is difficult.

Money remittance businesses were thought to be a higher risk sector.

There is a project to improve the NZ Police FIU database. It is important that the whole information technology infrastructure for the NZ Police FIU is urgently extended and remodelled, so that the FIU can properly perform its functions, including electronic receipt of STR.

Regarding supervision of banks, New Zealand’s approach to AML/CFT supervision differs significantly from that of most other countries

The New Zealand framework is generally built on three pillars: regulatory discipline, self discipline through effective internal governance and market discipline, but places much greater emphasis on the latter two pillars than is the norm elsewhere.

As regards AML/CFT supervision in particular, the RBNZ is not responsible for supervising all the main AML/CFT requirements that are laid out in the FTRA. This responsibility falls to the NZ Police FIU.

Neither the RBNZ nor the FIU conduct on-site examinations of banks and the RBNZ makes less use of prudential requirements than is the case in some countries.

Oversight of non-bank financial institutions by public authorities is limited.

Supervision by competent authorities thus plays a limited role in the New Zealand framework, and this creates an obstacle to ensuring the effective application of the AML/CFT requirements by financial institutions.

The FIU is not in position to fully carry out its supervisory role to ensure compliance, due to its limited resources and the absence of legal authority.

New Zealand authorities should develop an effective supervisory framework in order to have the adequate organisation to ensure the compliance with AML/CFT requirements of their financial sector.

There are no explicit requirements to identify the owners or controllers of legal persons such as companies.

New Pastures for New Zealand’s AML/CFT Regime

Following the 2005 IMF Report, it was another 8 years before New Zealand rolled out a revamped AML/CFT regime to its banks and financial institutions.

On 16 October 2009, the Anti-Money Laundering and Countering Financing of Terrorism Act received the Royal Assent but the AML/CFT Act did not come into force until 30 June 2013.

Over this 5-year lead-in period, NZ government had to develop an effective AML/CFT supervisory model. The private sector needed time to establish business risk assessments, followed by policies, procedures and controls.

Though the AML/CFT Act had a much better legislative framework which incorporated a supervisory oversight function, there was one significant flaw in the AML/CFT Act that remains today.

New Zealand’s ‘One Word’ Material Flaw In AML/CFT Act

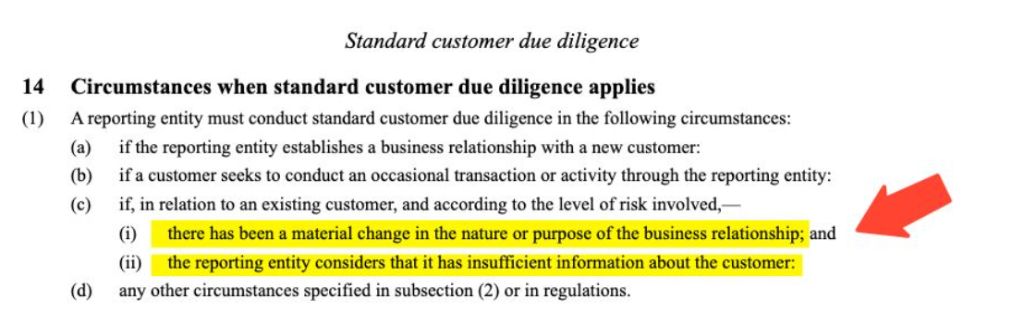

The primary "flaw" in the New Zealand AML/CFT Act concerns the definition of existing customers. The AML/CFT Act sets out that banks and financial institutions did not have to identify existing customers, even if they were aware there was an absence of identity information linked to the account.

The AML/CFT Act only required banks and financial institutions to identify existing customers if the account activity had a material change. An extract from the AML/FT Act of this flaw is copied below:

As the former FTR Act also did not set minimum identification standards, then it can be assumed when the AML/CFT Act came into effect ‘existing customers’ were not yet identified to a minimum and reliable standard, and it could remain that way.

As this flaw remains today in the AML/CFT Act, it can be assumed a high level of money laundering, financial crime, transnational crime etc is being facilitated through or within New Zealand.

Though the upcoming revamp of New Zealand’s AML/CFT Act is going to plug this gaping hole, why did it take so long? The Ministry of Justice, as the Administrator of the AML/CFT Act, should have plugged this gap immediately.

When a country operates with an international banking system that does not identify its underlying clients and/or beneficiaries, this is a clear exposure and attractiveness to facilitate transnational crime.

Financial Action Task Force Has Wool Pulled Over Eyes

When the FATF returned for its mutual evaluation of New Zealand in 2021, it failed to identify this flaw. The FATF 2021 Mutual Evaluation Report of New Zealand (FATF 2021 Report).

At page 189 of the FATF 2021 Report details –

Criterion 10.16 - Reporting entities are required to apply CDD requirements to existing customers on the basis of materiality and risk if there is a material change in the nature of purpose of the business relationship or the reporting entity considers that it has insufficient information about the customer (section 14(1)(c) of the AML/CFT Act).

Hidden in the above paragraph is the mistake made by FATF by stating the section 14(1)(c) uses ‘or’ whereas, as shown in the extract above, it is ‘and’.

Additional Flaws Continue Post AML/CFT Reform

Though the upcoming revamp of New Zealand’s flaws in the AML/CFT Act are intending to close this gap of section 14(1)(c), the harm from New Zealand operating with such a significant weakness has caused astronomical harm to the objectives of the AML/CFT Act.

However, this one word flaw is not the only flaw that exists in the AML/CFT Act and the upcoming reform of New Zealand AML/CFT laws is failing to address other existing weaknesses.

More on New Zealand’s weakened infrastructure to combat money laundering, transnational crime and financing of terrorism will be reported from Asia Pacific AML.

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows