Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

The ‘Gaspy’ For Mortgage Rates: New Tool Lets Kiwis See What Rates Others Actually Got

AUCKLAND, NZ. 7 May 2026. Most Kiwis would not dream of filling up the car without checking Gaspy first. The idea that petrol prices vary from station to station, and that a five minute check can save ten dollars, is now second nature. Mortgage rates work the same way, except the stakes are thousands of dollars a year, and until recently there was no easy place to look.

Spend ten minutes in any of the large NZ mortgage rates Facebook groups and the gap becomes obvious. The same question, posted again and again, sometimes dozens of times a day. "Refixing next week, ANZ offered me 5.89, is that competitive?" "What rate did you get on 1 year with BNZ?" "Anyone just refinanced to ASB, what did they actually walk away with?"

The replies are well meant, but messy. Screenshots from six months ago. Rates from a different equity band. Numbers without context. The person asking still walks away unsure whether they got a fair deal.

A new free tool, built in New Zealand, is trying to change that. It works on the same principle as Gaspy: people share what they paid, everyone else sees the range, and the market becomes a little less opaque.

From fuel to finance

The comparison is not perfect, but it is useful. Fuel is a commodity. The 91 octane at Z is the same 91 octane at Mobil. Mortgage rates are more complex. The rate a bank offers depends on equity, loan size, term, how long you have been a customer, and whether you are willing to walk. Two people at the same bank on the same day can receive different numbers.

That complexity is exactly why a simple shared benchmark matters. Not to replace negotiation, but to give people a starting point before they pick up the phone.

"There are tens of thousands of New Zealanders sitting in mortgage rate Facebook groups, posting the same question every single day," says Tom Filmer, who built the tool. "Refix coming up, what did you get. It is one of the most important financial decisions a household makes, and the best tool we have given them is a comments section. There has to be a better way."

How it works

The flow is deliberately simple, built around the way people already behave.

Upload a screenshot of the offer. The rate offer letter, the bank app screen, the email from the broker. The tool reads it to verify a real number is being submitted.

Confirm the details. The bank, the fixed term, the loan balance, the property value, and how long is left on the current fix are read straight from the screenshot, so there is almost nothing to type. Users just check the numbers look right before submitting. That is enough to place the submission in the right equity band, without identifying anyone.

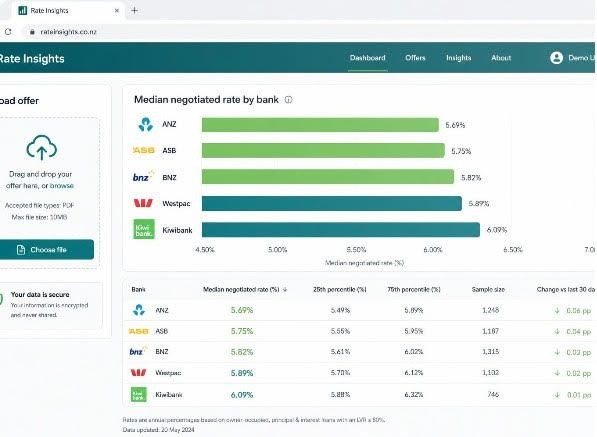

See similar results instantly. The page shows the median rate other Kiwis on the same bank, same term, and same equity band were offered, alongside the carded rate for that day. If a personal saving is available against the user's current rate, it is shown in dollars per year, not percentages.

Nothing is published with a name attached. No phone numbers are captured. No data is sold. The only purpose is to turn private offers into a shared, anonymous benchmark that everyone can use.

Why this matters now

Fixed terms in New Zealand are short. According to interest.co.nz and CoreLogic data, the average fixed rate term is now 12 to 18 months. That means most households are negotiating a rate at least once a year, often more. A 0.20% difference on a $650,000 loan is roughly $1,300 a year, every year, for the life of that fix.

The information asymmetry has always favoured the lender. The bank knows what every customer is paying. The customer knows only what they are paying, and whatever a few strangers in a Facebook thread are willing to share.

A shared benchmark, built from real offers, does not solve that imbalance entirely. But it shifts the starting point. Instead of walking in blind, a borrower can arrive with a sense of where the middle of the market sits for someone like them.

What it is not

This is not financial advice. It is not a rate prediction. It does not negotiate on anyone's behalf. The output is a benchmark, a starting point for a better conversation with a bank or a mortgage adviser, with the maths shown.

It also does not replace the Facebook groups. Those communities will keep doing what they do. The tool just gives the people in them somewhere to point when the same question comes up tomorrow night.

About Dashr

Dashr is a New Zealand built financial dashboard that brings a household's full financial position into one secure, read only view. By reducing the fragmentation across banks, KiwiSaver, investments, and everyday accounts, it helps Kiwis and their advisers make better informed decisions, without losing visibility along the way.

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students