Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

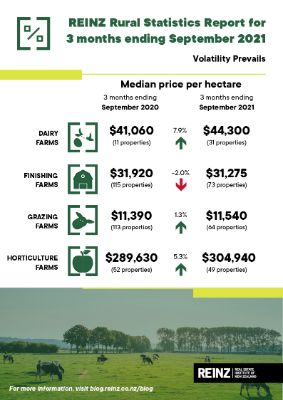

Volatility Prevails

Data released today by the Real Estate Institute of New Zealand (REINZ) shows there were 100 fewer farm sales (-27.5%) for the three months ended September 2021 than for the three months ended September 2020. Overall, there were 264 farm sales in the three months ended September 2021, compared to 321 farm sales for the three months ended August 2021 (-17.8%), and 364 farm sales for the three months ended September 2020.

1,667 farms were sold in the year to September 2021, 33.4% more than were sold in the year to September 2020, with 165.1% more Dairy farms, 1.0% less Dairy Support, 20.3% more Grazing farms, 39.1% more Finishing farms and 46.3% less Arable farms sold over the same period.

The median price per hectare for all farms sold in the three months to September 2021 was $31,300 compared to $25,560 recorded for three months ended September 2020(+22.5%). The median price per hectare increased 15.2% compared to August 2021.

The REINZ All Farm Price Index increased 0.1% in the three months to September 2021 compared to the three months to August 2021. Compared to the three months ending September 2020 the REINZ All Farm Price Index increased 13.9%. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors.

Two regions recorded an increase in the number of farm sales for the three months ended September 2021 compared to the three months ended September 2020, with the most notable being Auckland (+2 sales) and Nelson/Marlborough (+1 sales). Manawatu-Wanganui (-21 sales) and Wellington (-14 sales) recorded the biggest decreases in sales. Compared to the three months ended August 2021, 1 region recorded an increase in sales, Waikato (+4 sales).

Brian Peacocke, Rural Spokesman, at REINZ says: “Sales data for the three-month period ending September 2021 reflects ongoing volatility within the rural sector, on this occasion impacting farm sales which have dropped a significant 27.5% from the same period 12 months ago, albeit only slightly below the volumes recorded two years ago.

“The major impact was felt within the finishing (-36.5%), grazing (-43.3%} and the arable (-66.6%) categories.

“The major gain, by comparison, occurred in the dairy category which recorded 31 sales for the 2021 September quarter versus 11 sales for the September 2020 period (+64.5%) and whilst the numbers in themselves are not too dramatic, it does nevertheless signal an emerging degree of support for the dairy industry.

“Equally, however, it could also signal that given the improving financial forecast for the dairy payout, volatility accepted, some older vendors may well be picking this is an opportune time to retire and step away from a lengthy involvement in the dairy industry.

“Sales during the 2021-2022 season will tell if this is a continuing trend.

“Volatility from a variety of other sources continues to impact the rural sector, from equinox-driven extremes in weather to pandemic-driven extremes in the overall economy, both of which appear to be enduring currently within the country as well as offshore.

“Climate change, environmental issues, carbon prices and forestry expansion are further examples of where volatility is prevalent, and likely to continue.

“One of the brighter spots during recent weeks has been the announcement that non-national workers currently employed within the country on work visas, given appropriate conditions no doubt, can apply for residency. That is a first big step in assisting the rural sector with the retention and possibly the availability of labour, one of the endemic issues impacting the overall rural economy,” he concludes.

Points of interest from around New Zealand during September 2021 include the following:

- Northland/Auckland

Well spread activity throughout Northland with improved sales volumes for finishing, grazing and horticulture blocks in particular, with a good solid range of prices, horticulture again being to the fore. Reasonably quiet in the dairy category

A smattering of sales in the Auckland region, horticulture sales being notable in the Glenbrook and Bombay districts, with the Franklin region having more success on finishing properties than Rodney district to the north.

- Waikato

Strong sales of dairy units throughout the wider region from Hauraki to South Waikato, reinforced by two very solid results in the Gordonton district at $60,000 per hectare and better; Tatua supply properties continued that theme on a very much stronger basis; a healthy number of finishing property sales backed up by steady results for grazing units rounded off a good month for the province

- Bay of Plenty/Rotorua

An easing of activity within the coastal region; several sales of horticulture properties in the Western Bay of Plenty; no farm sales in the Rotorua district

- Gisborne/Hawkes Bay

Constrained activity throughout the eastern districts with one grazing unit sale in Gisborne, but the one in horticulture sale in Hawkes Bay gave a great result to the owner of a good Twyford apple orchard.

- Taranaki

Modest results in Ferdinand country with one South Taranaki dairy unit selling in separate parcels, and a dairy support unit in the same district selling at a very good price.

- Manawatu/Wanganui/Tararua

A substantial 65% drop in sales volumes within the region with lighter activity on grazing units in the Tararua; a welcome burst of results on forestry woodlots in the Horowhenua district.

- Wairarapa/Wellington

Deadly quiet on results from the Wairarapa but a brief spark of activity on a small finishing unit in Upper Hutt.

- Nelson/Tasman/Marlborough

A cluster of sales relating to one grazing property backed up by a finishing block in the Tasman district; Marlborough reported light sales in the finishing, grazing and horticulture sectors.

- Canterbury/West Coast

A gentle easing in volumes from last month but a significant drop in sales numbers from the September 2020 quarter; nevertheless, a good spread of that lighter result covering all categories across the Canterbury region; reports of increasing numbers of dairy units coming to the market, particularly in South Canterbury; activity in the West Coast was considerably reduced with one sale of a small grazing property.

- Otago

The general drop in sales continued in Otago, with results will down on previous months.

- Southland

Good activity in the southern region with a healthy array of sales across the board; two dairy units sold at consistent prices backed up by well-sold properties in the finishing, grazing and dairy support categories, with an ex-tulip growing property also selling strongly to round out the mix.

In September 2021, Finishing farms accounted for a 28% share of all sales. Grazing farms accounted for 24% of all sales, Horticulture farms accounted for 19% of all sales and Dairy farms accounted for 12% of all sales. These four property types accounted for 82% of all sales during the three months ended September 2021.

Dairy Farms

For the three months ended September 2021, the median sales price per hectare for dairy farms was $44,300 (31 properties), compared to $41,910 (30 properties) for the three months ended August 2021, and $41,060 (11 properties) for the three months ended September 2020. The median price per hectare for dairy farms has increased 7.9% over the past 12 months. The median dairy farm size for the three months ended September 2021 was 96 hectares.

On a price per kilo of milk solids basis, the median sales price was $47.36 per kg of milk solids for the three months ended September 2021, compared to $40.93 per kg of milk solids for the three months ended August 2021 (+15.7%), and $33.77 per kg of milk solids for the three months ended September 2020 (+40.2%).

The REINZ Dairy Farm Price Index increased 6.5% in the three months to September 2021 compared to the three months to August 2021. Compared to September 2020, the REINZ Dairy Farm Price Index increased 10.2%. The REINZ Dairy Farm Price Index adjusts for differences in farm size and location compared to the median price per hectare, which does not adjust for these factors.

Finishing Farms

For the three months ended September 2021, the median sale price per hectare for finishing farms was $31,275 (73 properties), compared to $30,815 (99 properties) for the three months ended August 2021, and $31,920 (115 properties) for the three months ended September 2020. The median price per hectare for finishing farms has decreased -2.0% over the past 12 months. The median finishing farm size for the three months ended September 2021 was 36 hectares.

Grazing Farms

For the three months ended September 2021, the median sales price per hectare for grazing farms was $11,540 (64 properties), compared to $11,670 (95 properties) for the three months ended August 2021 and $11,390 (113 properties) for the three months ended September 2020. The median price per hectare for grazing farms has increased 1.3% over the past 12 months. The median grazing farm size for the three months ended September 2021 was 104 hectares.

Horticulture Farms

For the three months ended September 2021, the median sales price per hectare for horticulture farms was $304,940 (49 properties), compared to $298,290 (46 properties) for the three months ended August 2021 and $289,630 (52 properties) for the three months ended September 2020. The median price per hectare for horticulture farms has increased 5.3% over the past 12 months. The median horticulture farm size for the three months ended September 2021 was 8 hectares.

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students