Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

A Hawkish Surprise As The RBNZ Runs Out Of Patience

29 November

- The RBNZ left the cash rate unchanged at 5.5% today. No surprises there. But their hawkish tone certainly surprised. The RBNZ revealed an upwards bias to inflation risks and will not call job done until they see the fruits of their labour shown with inflation back down to 2%.

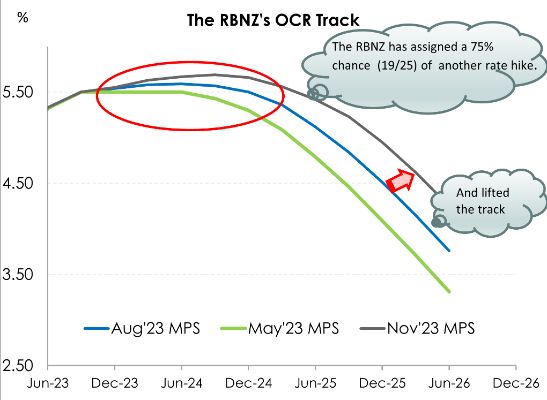

- Despite a number of data points which would have suggested the end of the tightening cycle, the RBNZ have kept the door wide open for another hike. Lifting the OCR track to 5.69% by September 2024, signalling a 75% chance of a hike.

- The timing of cuts is getting pushed further and further into the distance. We fear the downside risk of a softening global backdrop and the high interest rates which are still making their way through the economy. But we have to take the RBNZ’s word. Rate cuts are not looking likely anytime soon.

“…capacity pressures are assumed to decline by less than in the August Statement over the projection, supported by strong net immigration, a higher outlook for house prices, and stronger government investment over the medium term. World interest rates have also increased, placing downward pressure on the New Zealand dollar exchange rate and, all else equal, boosting inflationary pressure within the economy.” (RBNZ Nov MPS)

The RBNZ left the cash rate unchanged at 5.50% - no surprises. But the OCR track was lifted from 5.59% to 5.69% - big surprise. The RBNZ came out a lot more hawkish than expected. Inflation came in below their August expectations. But the RBNZ made clear that the champagne’s still sitting on ice. Rapidly decelerating imported inflation is doing most of the work in bringing down headline inflation. Domestic inflation is a slow-moving beast. And risks are tilted to the upside. Upside risks for which the RBNZ holds very little tolerance. Inflation has been sitting above target since mid-2021, and is forecast to remain above 3% for another 12 months. It’s going take some time before we get back to the 2% target. And the RBNZ is running out of patience. The RBNZ made clear that they’re “willing” to hike rates again if needed. Inflation expectations have become unanchored, and their credibility is under threat.

“Some members noted that inflation has now been above target for some time, and that there should be a low tolerance for any increase in the time to return inflation to target.” (RBNZ Nov MPS)

Everything washes out in the OCR track. And it was more hawkish than we had hoped. The key message in the track is that the RBNZ is willing to raise the cash rate again. The RBNZ lifted the OCR track to 5.69% by the September 2024 quarter. So odds are on (75%) for another rate hike and way out in 2024. We were surprised by the move. The RBNZ is clearly putting more emphasis on the growing demand impulse of the current migration boom. There’s greater risk that the boost to aggregate demand and housing (specifically rents) will outweigh the deflationary force of greater supply capacity.

There’s no doubt that a higher track was presented to also remind markets that “higher for longer” remains the rhetoric. Influenced largely by offshore developments, wholesale rates have recently drifted lower – effectively loosening financial conditions. And that’s not something the RBNZ wants here and now. What they do want is for rates to remain restrictive to continue weighing on household consumption and broader economic activity. Wholesale rates and therefore mortgage and other lending rates, need to stay high and dry. And the threat of further rate hikes does just that.

The other, somewhat academic, rational for the move higher in the OCR track was the upward revision to the guesstimated “neutral rate” – the Goldilocks interest rate that’s not hot or cold, it’s just right. The non-contractionary rate was lifted in the August MPS, from 2% to 2.25%, resulting in a higher track. And we saw the same play out today. The neutral rate was revised up 25bps to 2.50%. That’s the RBNZ’s way of saying the current level of interest rates don’t hurt as much as they’d like. The current cash rate is a little less effective in constraining demand. So basically, monetary policy is not quite as tight. And, in their eyes, we can handle a little higher rates.

But the hawkishness didn’t stop with the lift in the OCR track peak. Thoughts of rate cuts were also squashed. The new track has now pushed out the first rate cut to 2025, which would mean RBNZ staying on hold for ~2 years! We disagree. We acknowledge that the risk over the next 6-9 months is tilted toward further tightening. The RBNZ admitted an upward bias to rates. But we still believe the RBNZ will be in a position to normalise policy next year. Rate cuts could well be a 2024 story. Just later in 2024. We expect the inflation rate to be back within the 1-3% target band by mid-2024, and confidently returning to the 2% target. In saying that, our initial call for May is proving optimistic, at this stage. The RBNZ will want more data under its belt, specifically inflation prints, before changing direction. We now pencil in the first rate cut in November next year.

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students