Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Continuation Of Softening In New Vehicle Registrations In March

Motor Industry Association Chief Executive Aimee Wiley says that continued soft demand in March is attributable to the wider economic slowdown New Zealand is currently facing. Higher interest rates to combat inflation have also dampened consumer spending considerably.

11,616 registrations in March 2024 are 27.4% lower than March 2023 (4,381 units) and 44.7% lower than March 2022 (9,388 units). On a year-to-date basis, 2024 is 10.8% lower than 2023 (4,091 units), 27.8% lower than 2022 (13,056 units) and 23.4% lower than 2021 (7,951 units).

New Vehicle Industry Key points

- Top three overall market leaders in March 2024 are: Toyota with 20.6% market share (2,391 units), followed by Mitsubishi with 12.8% (1,489 units) and Ford with 12.1% (1,410 units).

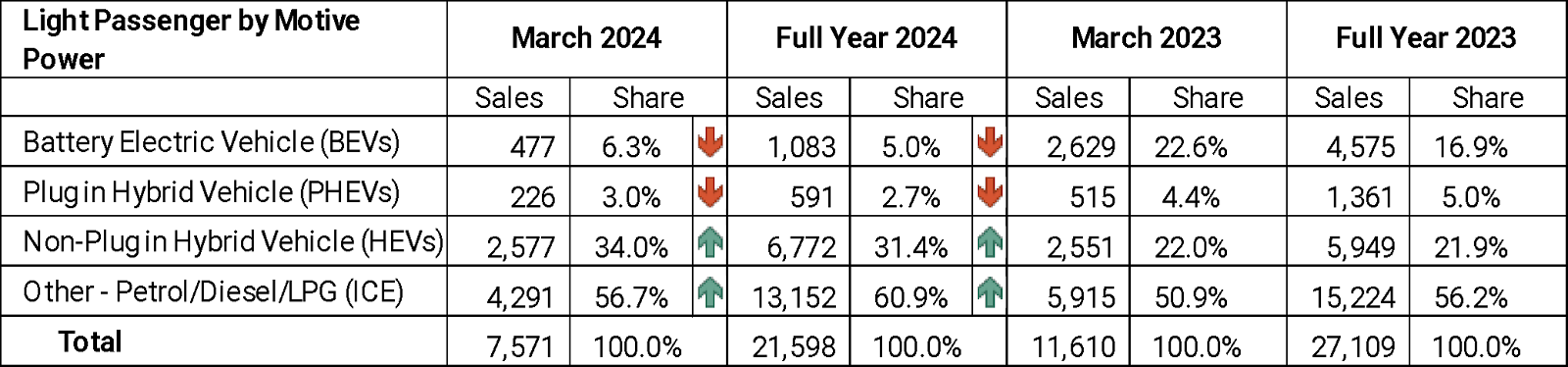

- March registrations breakdown: Light Passenger 7,571, Light Commercial 3,373 and Heavy Commercial at 672.

- Total Industry by motive power for the month of March: 521 BEVs (4.5% share), 226 PHEVs (1.9% share), 2,577 Hybrids (22.2% share) and 8,292 ICE vehicles (71.4% share).

- The overall top three segments in March were Pick Up/Chassis Cab (25.4%), followed by SUV Medium (22.8%) and SUV Compact (22.1%).

Light Passenger Vehicles (including SUVs)

Registrations

Light passenger at 7,571 is 34.9% lower than March 2023 (4055 units) and 32.3% lower than March 2022 (3,611 units). On a year-to-date basis, light passenger is down 20.3% (5,517 units) compared to the same period in 2023 and 22.0% (6,110 units) lower than the same period in 2022.

Light passenger segment leaders: Top 3

- Toyota 1,585 units and 20.9% segment share

- Kia 969 units and 12.8% segment share

- Mitsubishi 808 units and 10.7% segment share

Top selling light passenger models: Top 3

- Toyota RAV4, 791 units and 10.4% segment share

- Kia Stonic, 327 units and 4.3% segment share

- Kia Seltos, 325 units and 4.3% segment share

Segmentation – what consumers are buying: Top 3

- SUV medium 2,652 units (35.0% share of Light Passenger)

- SUV compact 2,563 units (33.9% share of Light Passenger)

- SUV Large 625 units (8.3% share of Light Passenger)

The small to medium segments comprised 86.3% of Light passenger.

Light Passenger Motive Power Insights

Top selling models (by motive power)

Battery Electric Vehicles (BEVs):

The top five models in March: Tesla Model 3 (125 units), followed by Tesla Model Y (74 units), MG 4 (42 units), Volkswagen ID.4 (28 units) and BYD Dolphin (20 units).

Plug in Hybrid Vehicle (PHEVs):

The top five models in March: Mitsubishi Eclipse Cross (32 units) followed by Mitsubishi Outlander (31 units), Mini Countryman (30 units), Mazda CX-60 (17 units) and Land Rover Range Rover Sport (13 units).

Mild Hybrid Vehicle (HEVs):

The top five models in March: Toyota RAV4 (790 units), followed by Toyota Corolla Cross (181 units), Toyota Yaris Cross (147 units), Toyota Yaris (134 units) and Toyota Corolla (112 units).

Light Commercial Vehicles

Registrations

Commercial registrations of 3,373 are 6.5% lower than March 2023 (236 units) and 63.3% lower than March 2022 (5,814 units). On a year-to-date basis registrations are 13.4% higher (1,210 units) compared to the same period in 2023 and 41.9% (7,357 units) lower than the same period in 2022.

Segment leaders

Ford retained the market lead with 32.6% market share (1,101 units) followed by Toyota with 23.9% (806 units) and Mitsubishi third with 20.2% market share (681 units).

Top selling models

The top five models for the month of March were the Ford Ranger (1,005 units), followed by Mitsubishi Triton (681 units), Toyota HiLux (611 units), Nissan Navara (292 units) and Toyota HiAce (107 units).

Motive Power

Light Commercial BEVs: 22 units in March, 59 units year-to-date.

Heavy Commercial Vehicles

Registrations

Heavy commercial registrations of 672 are 11.8% lower than March 2023 (90 units) and 5.8% higher than March 2022 (37 units).

On a year-to-date basis registrations are 11.7% higher (216 units) compared to the same period in 2023 and 24.8% higher (411 units) than the same period in 2022.

Motive Power

Heavy Commercial BEVs: 22 units in March, 82 units year-to-date.

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows