Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

When Good Data Gets Buried In Uncertainty. And Inflation Is Eye-watering To Look Through

- Escalating conflict in the Middle East is likely to dominate market moves for the foreseeable future as the data flow slows and tensions intensify.

- As expected, last week the Fed and BoE left monetary policy settings unchanged with both central banks both noting they are still assessing the impact of tariffs on growth and inflation. Meanwhile at home we saw Kiwi growth outpace expectations over Q1.

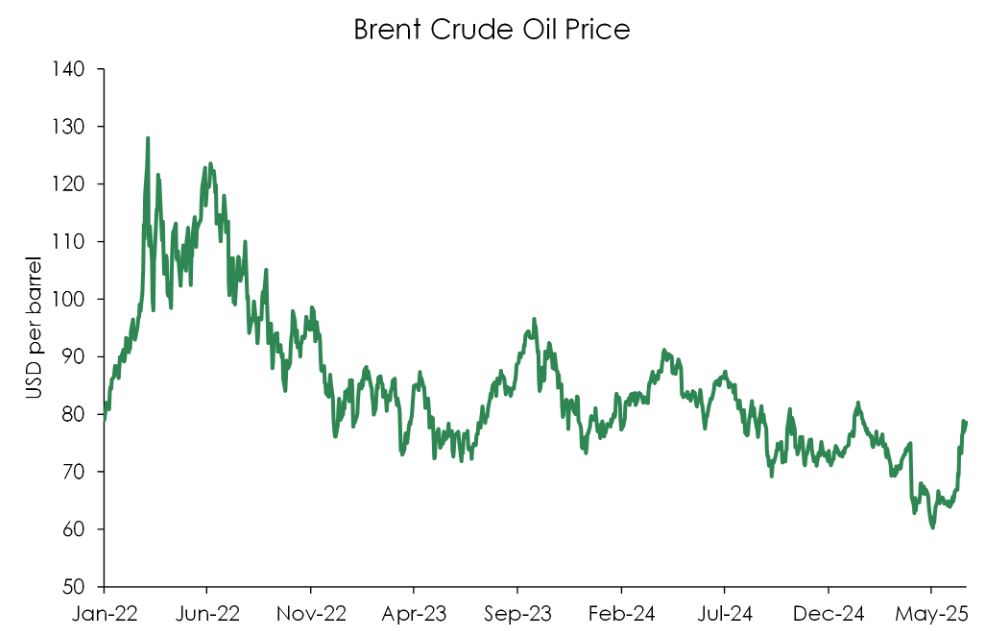

- Our COTW looks at the increase in inflationary pressures stemming from offshore. Food prices are up 4.4%, and oil prices are heading higher.

Here’s our take on current events

Conflict in the Middle East intensified over the weekend as the US launched strikes on three nuclear sites in Iran. And with geopolitical tensions running high, investors continue to move towards safe haven assets. Reclaiming it’s tested safe-haven status the USD has regained strength seeing the Kiwi dollar trading back below 60c. Meanwhile, oil prices, already a leg higher last week, will likely continue on a path higher as tensions persist. Especially with the situation still fluid and the potential for retaliation by Iran. Markets will be closely watching the next steps in the geopolitical landscape. Particularly around the potential closure of the Strait of Hormuz. But for now, the risk remains tilted toward further downside for the Kiwi as the risk-off sentiment continues.

As the situation unfolds, we’re thinking about the potential inflationary and growth impacts for the global and domestic outlook. Sustained disruption in the Middle East would likely exacerbate energy supply concerns, causing a bout of global inflationary pressures. And in today’s already fragile environment, facing tariff trade disruption and an economy only just emerging from recession, a near-term rise in fuel costs would likely place additional pressure on Kiwi households and businesses, reinforcing downside risks to domestic growth. Like most things these days, we’re hoping for a better outcome to play out… But we must flag the downside risks to the global and domestic outlook.

Overshadowed by the conflict in the Middle East, the US Federal Reserve and the Bank of England also met last week. Both central banks left policy rates unchanged as expected, and signalled a patient approach, awaiting more clarity on the impact of tariffs on growth and inflation.

Here at home, the latest GDP numbers out last week showed the pace of the economic recovery quickened over the start of 2025. Economic activity lifted 0.8% over the March quarter, slightly outpacing our expectation of 0.7% and significantly stronger than the RBNZ’s 0.4% forecast. (See our full report here).

It’s nice to have some good news. But we’re holding our horses. The economy remains 0.7% below pre-recession levels. And in the year to March 2025, the Kiwi economy shrank 1.1%. We’re still crawling out of the deep hole we fell into last year. A hole which has been even deeper on a per capita basis. On a per person basis, economic activity lifted 0.5% over the quarter but remains down 1.6% over the year.

Unfortunately, we may be crawling for some time longer. From here out, we’re not expecting to see the same strength seen over summer period sustained. We expect that the damaging effects to growth from tariff volatility and uncertainty have already started to take effect this quarter. And we expect those headwinds to become more evident in the June quarter GDP figures.

More timely economic data are already starting to point to a slowdown. Electronic card spending has softened, and both the manufacturing PMI and services PSI fell sharply back into contraction in May. Weak confidence amid economic fragility and tariff uncertainty is resulting in softening demand. And it’s under these conditions that we’re expecting a weaker Q2 GDP outturn than the strong prints over the summer period.

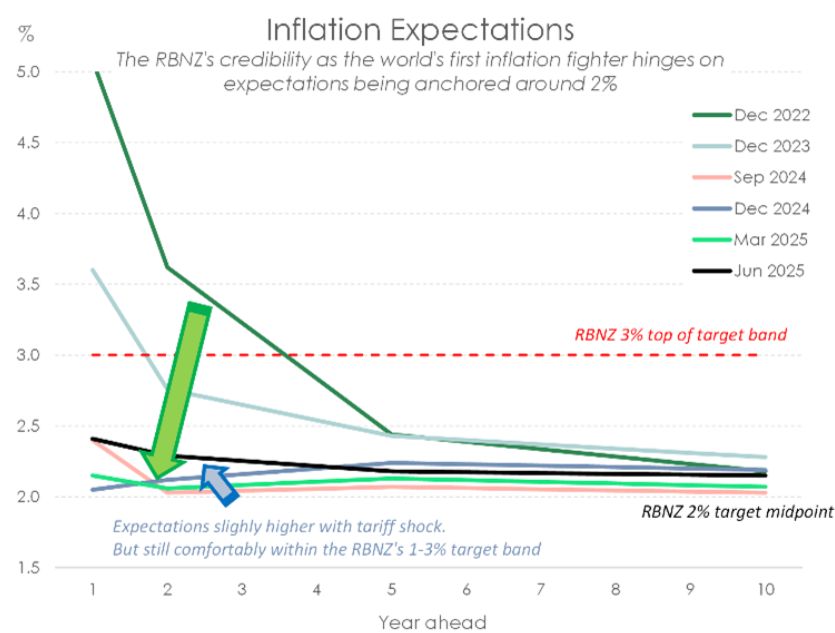

Chart of the Week: Inflation is eye-watering to look through.

Monetary policy makers must look through short-term volatility, even if it’s eye-watering.

Inflationary pressures from offshore are heating up. Food prices are up 4.4%, reflecting elevated global commodity prices. Higher prices for fruit and vegetables as well as meat drove the increase in food prices in May, up 3.6% and 1.7%, respectively.

Petrol prices fell 2.7% in May, but a reversal is likely this month following the conflict in the Middle East. Global oil prices are almost 20% higher since the start of the month.

Domestic inflation continues to ease, but frustrations remain. Rents for example, have cooled rapidly, rising just 0.1% over the month. Annual rental inflation is running at 2.8% - the slowest pace since January 2015. Household energy costs however are on the rise, up a chunky 2.3% over the month.

The risk here is that inflation flirts with the top of the RBNZ’s target band in the near-term. We had already pencilled in a move towards 2.7% this year. But it’s looking like we’ll see a higher peak. In saying that, downside risks dominate the medium-term. Consumer prices will come under pressure amidst slowing global demand and excess capacity in the economy. There’s risk that inflation falls below the RBNZ’s 2% sweet spot, which would necessitate further monetary policy support.

The typical play for central bankers facing a spike in inflation is to look through it, especially if it is the result of a shock. Such is the case for the recent increase in oil prices. The impact should be temporary and an unwind likely. But as we’ve learnt from the RBNZ’s last meeting, there’s nervousness around rising inflation expectations.

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students