Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

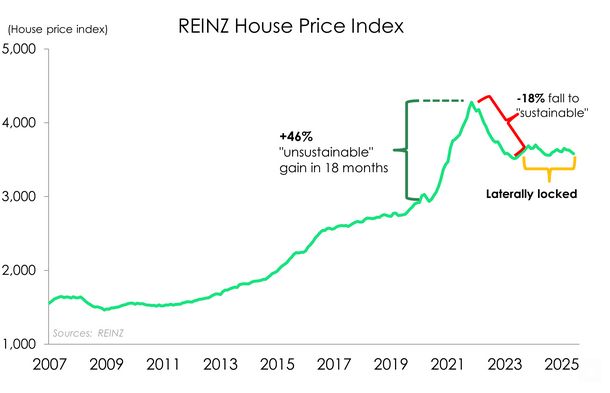

Our Laterally Locked Housing Landscape Is Holding The Line. We’re Looking Ahead

- The Kiwi housing market continues to stumble sideways. Yes, there was an unsustainable 46% surge out of Covid. Yes, the RBNZ orchestrated an 18% correction back to more sustainable levels. But over the last 2 years, house prices have gone nowhere. That will change, next year. Interest rate cuts will fuel confidence. And confidence will generate activity.

- Investors have been hunted by policymakers, both from the last Government and RBNZ. Interest rate deductibility, Brightline tests, and laser focussed LVR restrictions have all targeted investors. Precisely what we don’t need with a chronic housing shortage. It’s investors that will reignite the housing market. But now, they remain sidelined, waiting to rebuild equity in their portfolios. It’s chicken and the egg. Which one came first? Interest rate cuts.

- Interest rates are the biggest driver of house prices. Swift interest rate cuts are feeding through fast. But they have not gone far enough. And investors no longer need to worry about the Brightline test or interest deductibility. But they do still worry. They’re waiting for the economy to recover. They’re waiting for their own businesses to improve. They’re waiting.

- The true test will come over the warmer months.

The latest REINZ data shows a housing market that remains largely locked in lateral moves. After seven consecutive months of (very) modest gains, house prices dipped by a seasonally adjusted 0.3% in June. Over the year, house prices were up just 0.3%. That’s not a market in recovery. It’s a market that is failing to find its footing. And after 225bps of rate cuts, the recovery lacks any real conviction.

House prices are still down 16.3% from the November 2021 peak. And prices have only lifted half a percent since the RBNZ started cutting in August last year. Rate cuts have not yet triggered investors. The median national house price sits virtually unchanged from a year ago at $770,000. And the median days to sell, one of the best real-time indicators of housing dynamics, continues to yo-yo above the long-term average of 40. The longer it takes to sell, the weaker the market. And days to sell lifted to 50 from 47 last month. It’s still a buyer’s market out there.

As we said in our latest outlook “We’ve seen green shoots emerge, and then die off, only to re-emerge again. But we must wait, like gardeners, until spring… to see if the green shoots start blossoming or remain in drought.”

The data for June was frost bitten. The colder months are always harder on the housing market. But nevertheless, this is certainly not a hallmark of an economy that has undergone a significant easing cycle.

And if anything, the unresponsiveness of investors is a sign that there is more work for the RBNZ to do. More rate cuts are needed to stimulate demand in housing. Much of our optimistic forecasts for growth in the Kiwi economy into 2026 is predicated on a bounce in housing demand. It’s the Kiwi way.

Heightened job insecurity from a labour market still bleeding out, a surge in housing stock, the continued absence of investors, and rapidly declining net migration are all weighing heavily on the housing market’s recovery. Many of these pressures are themselves by-products of an economy that still needs stimulus.

Yes, we are getting closer to the bottom in interest rates. And these days forecasters, including ourselves, are arguing over just 50bps. It’s not much, but it is still important. Do we need a neutral (unhelpful) rate of 3%, or do we need a stimulatory (helpful) rate of 2.5%. We argue that the economy needs (more) help.

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students