Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Go Big For Bang For Buck. The RBNZ Should Go 50

- Mark your calendars. Wednesday 2pm. The RBNZ is set to cut the cash rate. Now, it’s a matter of magnitude. We favour an accelerated move to 2.50%. That is, a 50bps cut.

- The market only has 31bps priced for Wednesday. The way we look at it, it’s exactly these sorts of odds that can give the RBNZ bang for buck. If they cut 50bp, it is not priced, it is not consensus, but it is needed. A 50bp move would get wholesale rates down, lowering retail rates. Whereas a 25bp cut would cause a lift in wholesale rates, making retail rates more sticky.

- Beyond Wednesday, we expect a 25bps cut in November to 2.25%. There’s no doubt our fragile economic recovery needs some extra juice. Lower rates will set up the economy well for the summer trading period.

Here’s our take on current events

A cut from the RBNZ on Wednesday week is all but a done deal. The RBNZ has delivered a significant amount of easing – 250bps to be exact. It’s a lot, and it does put the RBNZ among the most aggressive central banks. But, importantly, rate cuts to date have simply returned monetary policy to “neutral” settings. It is only this week’s eighth cut in the cycle that would work to add stimulus into the economy. Wednesday’s rate decision is pivotal in setting the trajectory in financial markets, and the wider economy, heading into 2026.

The current cash rate of 3% isn’t stimulatory, and it isn’t encouraging excessive behaviour or inflation. But we need a stimulatory rate if we’re going to encourage businesses to take on risk – either invest or hire. And we need a stimulatory rate if we’re going to see embattled households boost discretionary spend. 2.5% is closer to what we need. And the risks are towards a 2% cash rate, in our opinion.

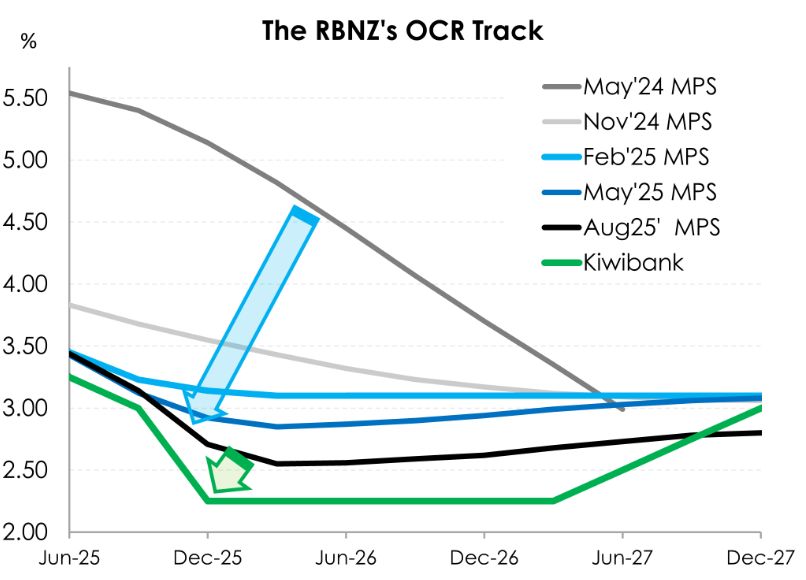

We know that the cash rate will go to at least 2.50% by Christmas. Governor Christian Hawkesby signalled (rather explicitly) as much in his remarks at the Financial Services Council Annual Conference earlier this month. However, there are several routes the cash rate may take to get to 2.50% - and potentially below.

The first scenario is one in which the RBNZ cruises into next year on autopilot. Delivering a 25bps cut this week, and a 25bps cut in November. It’s a seemingly straight bat decision, but one that will no doubt trigger an unhelpful reaction in financial markets. Frustrated (again) by the RBNZ’s delay in getting the job done, wholesale market traders would push interest rates higher. The OCR endpoint priced into the OIS strip would lift from ~2.24% low towards 2.50%. The pivotal 2-year swap (interest) rate would rise from around 2.63% back above 2.80%, unwinding the 20bps post-GDP rally. Mortgage rates would barely move. And in fact, the risk further out turns towards a slight lift in mortgage rates. Very unhelpful. The Kiwi dollar would likely pop higher, back towards 59c. And that’s also very unhelpful. Our exporters could use a little currency depreciation to help offset the tariffs to the US

Given the fragile state of the economic recovery, with demand risks still abound, autopilot is exactly what we don’t need. Rather, awake at the wheel and driving the recovery into 2026 is.

The second scenario is one in which the RBNZ frontloads the signalled easing. The RBNZ could get to 2.50% in one fell swoop (a 50bps cut). But in the same breath, the RBNZ could also signal the end of the easing cycle.

The need for an accelerated move to 2.50% stems from the June quarter GDP figures. They were ugly. The Kiwi economy slammed into reverse, contracting 0.9% over the June quarter. This compares to the RBNZ’s forecast of a 0.3% contraction. The data may be old, but the miss is meaningful. The RBNZ will likely conclude that the output gap is more negative than last estimated. The RBNZ will be going back to the drawing board with a weaker growth starting point.

A ‘50 and done’ would still be consistent with the RBNZ’s forward guidance, but markets would interpret such a move as hawkish. We will likely see a similar reaction in financial markets as the first scenario, but perhaps not as strong. Because only 31bps are currently priced for Wednesday, meaning there’s still an element of shock to come from a 50bp cut. But signalling “that’s all folks” would see a recalibration in market expectations. Currently, a ~2.26% terminal rate is being priced by early next year. But that would quickly lift under this scenario with the OIS curve pushing higher. Naturally, wholesale rates would sell off, limiting further (needed) downside to retail rates. And the decision might also light a fire under the Kiwi dollar as the RBNZ underdelivers on current market expectations.

The third scenario is what we think they should do. Like the second scenario, the RBNZ should deliver 50bps on Wednesday. But we think some extra juice is warranted. We have long-forecasted the cash rate falling to 2.50%. But it’s becoming clear that the economy needs more support. We expect a further 25bps cut in November to 2.25%.

In this scenario, wholesale rates would likely continue their downward spiral. Because a 50bps cut is not completely priced, and the signal for another cut in November should see expected cuts brought forward. Pricing for the November meeting should drop to 2.25%, and wholesale rates along with it. It’s not hard to see a ~10bp slide in the pivotal 2-year swap, easing towards 2.50%. All mortgage rates would likely be lowered, as needed. And the Kiwi dollar would lose further ground against most other currencies. Last week, the RBA once again emphasised a gradual and cautious approach to policy easing. A relatively tight labour market across the ditch affords the RBA patience. Similarly, the Bank of England is also stressing caution as it battles persistent inflation. Meanwhile, the ECB is virtually calling time on its easing cycle. All the while the Reserve Bank remains in a position of needing to do more. And in delivering more easing than its peers, interest rate differentials are working against the Kiwi. However, risks of a sustained weakening against the Greenback seem limited as the Fed resumes its easing cycle.

We hope that 2.25% is the cycle low in the cash rate. But we think there’s about a 50/50 chance of a further move to 2% in February. It will depend on how the data and recovery play out. This summer will be an important time for data watching. Will the housing market pick up? Will consumer confidence lift into consumption? And will business confidence translate into activity? We hope it will. It will all feed into the February decision.

Charts of the Week: It’s a matter of magnitude.

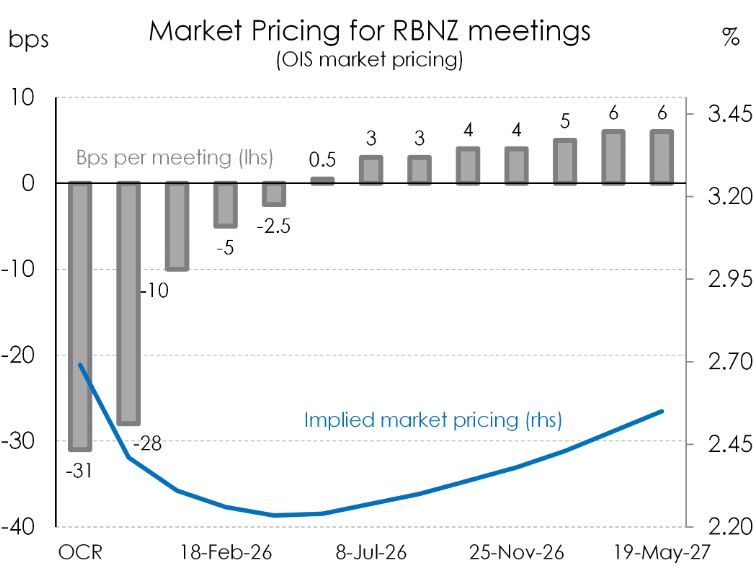

It’s a big week for interest rate markets, with traders on edge. There’s no debate around the need for the RBNZ to cut (again)… But there is active debate over magnitude. 11 of the 26 economists surveyed by Reuters and Bloomberg expect a 50bp cut. We’re in that camp. And there are 15 economists calling for a 25bp move. The way we look at it… it’s exactly these sorts of odds that can give the RBNZ bang for buck. If they cut 50bp, it is not priced, it is not consensus, but it is needed. A 50bp move would get wholesale rates down, lowering retail rates. Whereas a 25bp cut would cause a lift in wholesale rates, making retail rates more sticky.

The market is reasonably priced, and reflects our core view (almost). Looking at the OIS strip, a 2.25% cash rate is priced by April/May. That’s close. But we think the RBNZ should get there by November. For this week’s decision, the market is divided between a 25bp cut and a 50bp cut. There is 31bps priced, to 2.69%. So a full 25bp cut is fully priced and there’s another 6bps thrown in towards a 50bp move. If they do cut by 50bps, the 2.69% rate drops 19bps to 2.5%, making waves. For November, the market has an implied rate of 2.41%. If the RBNZ do cut to 2.25%, then there is a hefty 16bps to fall. Pricing from February (2.3%) onwards is very close to our view.

The latest GDP report on the Kiwi economy’s performance shocked us into calling for, demanding, a 50bp cut this week. See:A deep economic contraction: The RBNZ is once again behind the eight ball. The economy needs stimulus.

Priority one: Regional Deal Strengthens Confidence In The Western Bay Of Plenty

Priority one: Regional Deal Strengthens Confidence In The Western Bay Of Plenty REINZ: Buyer Activity Softens As Living Costs Remain A Consideration Across Key Regions

REINZ: Buyer Activity Softens As Living Costs Remain A Consideration Across Key Regions Better Taxes for a Better Future: Tax Policy Welcome Contribution, But Missed Opportunity To Tackle Wealth Inequality

Better Taxes for a Better Future: Tax Policy Welcome Contribution, But Missed Opportunity To Tackle Wealth Inequality Google Threat Intelligence Group - GTIG: Google Threat Report Warns AI-Driven Cyber Operations Are Scaling Across Global Threat Landscape

Google Threat Intelligence Group - GTIG: Google Threat Report Warns AI-Driven Cyber Operations Are Scaling Across Global Threat Landscape Commerce Commission: Baseline Research Report On The State Of Competition In New Zealand

Commerce Commission: Baseline Research Report On The State Of Competition In New Zealand University of Auckland: Junk Food Designed To Make Us Eat More, Study Finds

University of Auckland: Junk Food Designed To Make Us Eat More, Study Finds