Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Inflation Has Spiked, But Will Recede. The RBNZ Will Cut, To Plant The Seed

- Kiwi inflation has climbed to the top of the RBNZ’s target band. But it shouldn’t linger. The more cyclical components of CPI are soft and should see inflation return to the 2% sweet spot in 2026. Beyond that, there’s risk of sub-2% inflation given excess capacity within the economy.

- The US and China are closing in on a trade deal. Sounds familiar… Both sides have reportedly landed on a “framework” to be discussed by President Trump and President Xi later this week. Shiny commodities stole the limelight last week. But traders are back playing in the more risky corners of the market.

- Home is where the heat is. Inflation heat that is. Our COTW takes a closer look into the details of September’s inflation report where sticky administrated costs under the housing group (think council rates, insurance and electricity charges) are keeping domestic inflation elevated.

Here’s our take on current events

Last week was all about Kiwi inflation. At 3%, Kiwi inflation has climbed back to the top of the RBNZ’s 1-to-3% target band. Over the quarter, consumer prices rose by 1%. There was little in the latest inflation report that surprised. The factors driving inflation higher, like food and administered costs, should prove temporary. While the more interest rate sensitive components of CPI, like rents and construction costs, are clearly soft. For now, we think the risk that this bout of inflation will persist is low. Because there is significant spare capacity still sloshing in the economy, and keeping downward pressure on medium-term inflation. More importantly, inflation expectations remain well anchored to the 2% target midpoint. (See our full review here): https://www.kiwibank.co.nz/business-banking/thrive-hq/kiwi-economics/commentary-insights/up-up-but-not-away-inflation-is-not-here-to-stay/

The September quarter will likely mark the peak in inflation. The current December quarter is typically the weakest quarter for inflation with seasonally weak food prices as well as the usual retail discounting into Christmas. With that in mind, we expect inflation to fall back below 3% from here. And the risks further out are still tilted to the downside.

September’s inflation report was largely in line with the RBNZ’s forecast. The move to 3% is unwanted. But inflation shouldn’t stand in the way of the RBNZ delivering further rate cuts. They should take comfort in underlying inflation, which remains subdued. Core measures of inflation strip out the volatile price movements. And encouragingly, core inflation fell from 2.7% to 2.5% - the lowest since March 2021. It is the RBNZ’s job to look through volatile movements and set policy for the medium term. And in 2026, inflation is set to slow below the mid-point of the target band (2%). We continue to expect an RBNZ rate cut to 2.25% next month.

In the world of financial markets, the shiny commodities lost some of their sparkle last week. This week, traders are back playing in the riskier corners of the sandpit as the US and China reportedly close in on a trade deal (sounds familiar…). Equities are recording record highs, again, and the Kiwi has lifted. Of course, these trade meetings have come and gone before with little to show. But there’s a bit more optimism this time around. Talks between trade officials on both sides have reportedly landed on a “very successfully framework” that’s to be discussed by President Trump and President Xi later this week in South Korea. The agenda supposedly covers everything from China’s control of rare earth metals to US’s tariffs on Chinese imports and even the fate of TikTok. Will it be a success? We’ll have to wait and see…

Amongst all this, the US government shutdown continues. At nearly four weeks, it’s the second longest shutdown in US history. And it sets the backdrop for the US Federal Reserve rate decision this week. The shutdown has delayed key data releases, including payrolls for September. Without the data, the proudly data-dependent central bank has effectively been flying blind into this rate decision. Despite this, the Fed is expected to press on and deliver a rate cut as signalled in their recent dot plot and as almost fully priced by financial markets.

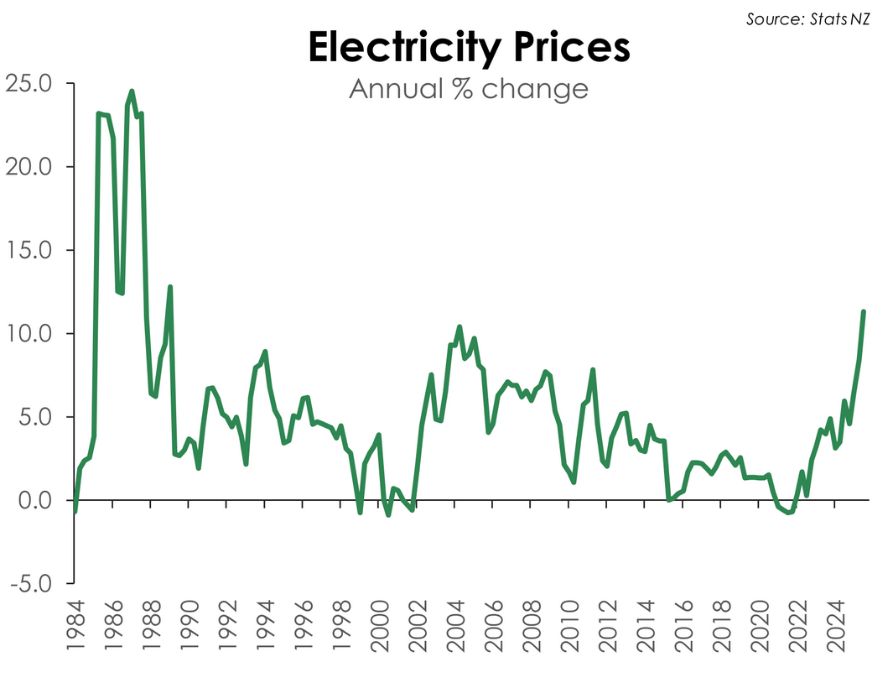

Charts of the Week: Home is where the heat is.

Taking a deeper look into the details of September’s inflation report, domestic inflation, continues its (slow) move south. Annual non-tradables inflation has fallen to 3.5% from 3.7%. Domestic inflation has fallen some way from its 6.8% peak in 2023, but it is still sitting above the long-term average (~3%). And that’s despite such a weak domestic economy.

Such persistence is due to the lingering strength in administered prices. Most of which is coming through the housing group. Contributing close to 45% of the lift in prices over the quarter and 35% over the year, the housing and household utilities group is where most of the inflation pain is being felt. Within that, council rates and electricity prices are the biggest upward drivers. Over the quarter council rates, up 8.8%, accounted for 30% of the quarterly lift in prices. Meanwhile, electricity prices up 11.3% over the year are the highest since the late 1980s. The price effect is showing up in our internal card spend data. In our latest look into consumer spending ("Splurging on Essentials") , we saw that total dollars spent on household utilities has increased an eye-watering 19.3% in the September quarter compared to last year.

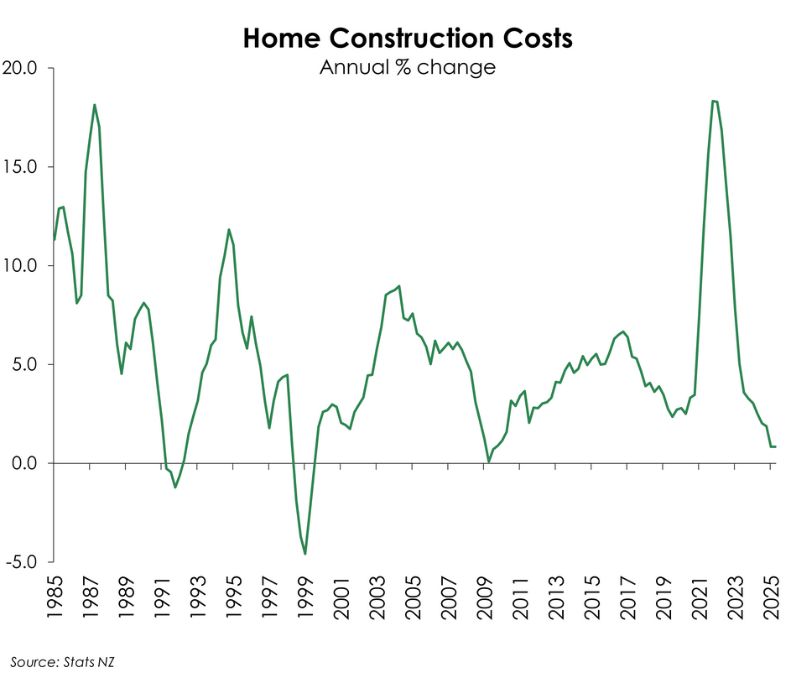

These so-called cost-push inflation movements are being offset to some extent by weak price growth in other components of housing-related inflation. Construction costs are still running at the weakest rate since the end of 2009 (0.8%yoy), while rental inflation fell to sub-3%. Our dormant housing market as well as weak migration flows are having a clear impact.

If we exclude these government administered costs, domestic inflation sits at a 2.6%. And that’s a better reflection of the current weak state of the economy.

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students