Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

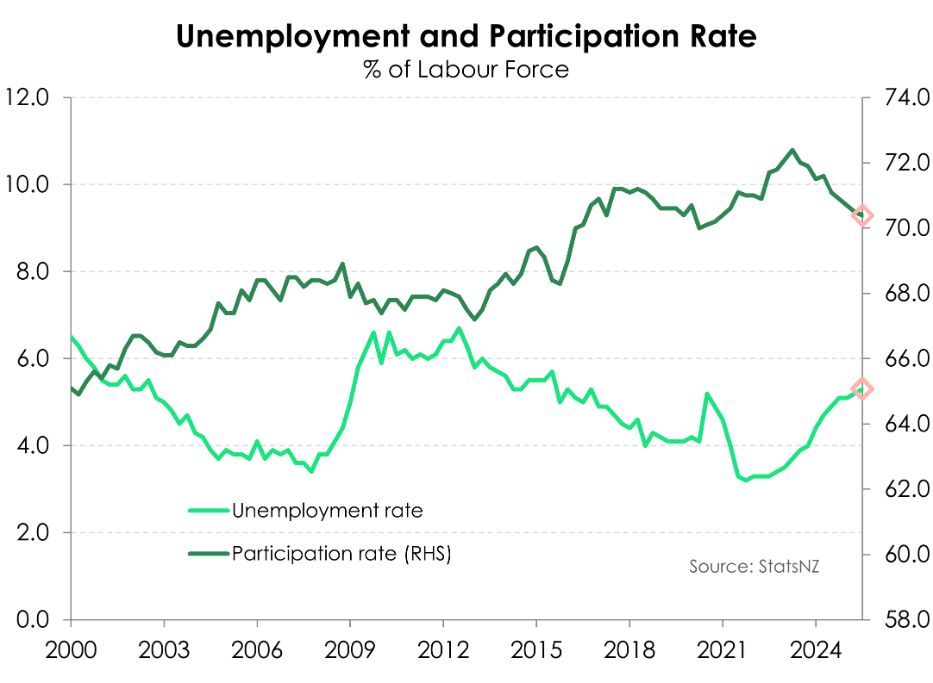

Trick Or Treat Or Turnaround? What Will The Kiwi Labour Market Reveal Next Week

- Stats NZ’s suite of labour market data is out on Wednesday. The Kiwi labour market likely loosened a little further over the September quarter. We expect the unemployment rate to increase to 5.3% from 5.2% - the highest in over eight years. But there are growing signs that we may be at the peak.

- The moderation in wage inflation likely continued. Annual wage growth likely slowed to 2.1%, down from 2.3% - the weakest in four years. Weaker wage inflation is helping to drive further easing in domestic, specifically services, inflation. It’s the famous Phillips curve at work.

- Next week’s data should reinforce the need for further monetary policy easing. Downside risks to medium-term inflation are growing given the soft labour market and dimming global outlook. We expect the RBNZ to cut the cash rate by 25bps at the November meeting.

Hot on the heels of the September quarter inflation update, next week’s attention turns to the Kiwi jobs market. We expect that conditions in the labour market loosened a little bit further over the quarter. In some good news, there are signs that the market is beginning to stabilise. 2026 should be a better year. But right here, right now, labour demand is not yet strong enough to absorb the extra supply entering the market.

Monthly employment data suggests that the appetite for labour is slowly improving. Filled jobs appears to have hit a trough in July. Since then, filled jobs began to tick higher with a decent (albeit likely overstated) 0.3% in September. However, even with such a lift, total filled jobs remain 1.9% below the March 2024 peak. Given current weak economic activity, we don’t expect labour demand to take off like a horse bucking. But the September quarter likely marked the turning point in employment growth, with monthly jobs growth averaging around a flat print.

At the same time, the working age population likely grew 0.3% over the quarter. Labour demand may be recovering, but labour supply continues to outpace. With this dynamic, the unemployment is set to hit the highest level since December 2016, rising from 5.2% to 5.3%.

Growing slack within the labour market should also see wage growth continue to moderate. The private sector Labour Cost Index (LCI) hit a series high of 4.5% in early 2023, as rising inflation expectations and labour shortages bolstered wage demands. But the balance of power has shifted back to employers. We expect to see a 0.4% quarterly rise in wages, pulling down the annual rate from 2.3% to 2.1%.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention