Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

They Love Their Burgers. And We Love Tariff-Free Meat. It’s Another Positive… With Fewer Negatives

- It was a big week out of the US. The longest Government shutdown in history came to an end. And the US has dropped their tariffs on meat. They love their burgers. They serve dinosaur sized porterhouse steaks. And hot dogs are big in baseball. It’s good news for us… our largest export to the US is meat.

- Domestically, a number of higher frequency data points painted a mixed picture of how the economy is progressing. Overall though, the data reflects an economy that is simply stabilising from weak levels.

- Our COTW takes a look at the RBNZ’s latest Survey of Inflation Expectations. It’s a bit of a nothing to see here report with expectations anchored around 2%.

- We had the pleasure of hosting Professor Prasanna Gai, RBNZ board member, at a Kiwibank event. It was a great opportunity to gain some insight. And we discussed plenty. See our Event of the Week for more.

Here’s our take on current events

After 43 long days, the US Government shutdown finally came to an end last week. President Trump signed off on a temporary funding bill, securing funding up until the end of January. There’s risk of another shutdown early next year, but we’ll cross that bridge when we get there. For now, US Government workers returned to work on Friday, and back payments of the month’s missed wages commenced over the weekend. But despite the resumption of government operations, damage has been done. And a full return to normal is expected to take days, even weeks in some areas. Just a few weeks ago, the Congressional Budget Office had estimated that a six-week government closure would reduce US real GDP by 1.5%pts for the December quarter. A rebound in activity is expected to recoup most of these losses into next year. But the matter of economic data lost to the void remains.

Six weeks delayed, the US Bureau of Labor Statistics is set to release September’s missed payrolls report later this week. However, the release of October data will be a little more complicated given the absence of data collection over the month. We’ll likely get payrolls but because the household survey wasn’t run, we won’t get the unemployment rate for October. We also won’t get October CPI inflation. Two-thirds of prices in the CPI are collected by in-person visits, which clearly did not take place with the govt shut down over the month. Statisticians will likely resort to imputation methods to fill the blanks. But such estimates may still lack reliability. And overall has added some extra fog for the Fed as they approach their final meeting of the year in which markets continue to pare back on expectations of a further cut.

On a more positive note, President Trump signed an order to remove reciprocal tariffs on a number of agricultural imports. The move comes in response to growing US consumer concerns around rising food costs. And there’s a big win in it for us with beef products among the list of newly exempt imports. What can we say, Americans just love their burgers. And we love tariff-free meat. Meat is our largest export to the U.S. It’s another positive with fewer negatives leading to a more optimistic outlook into 2026.

Okay, enough about America…

At home, alongside the release of the RBNZ’s Survey of Inflation Expectations (see our COTW for more), a number of high frequency data points painted a mixed picture of how the economy is tracking. Short term visitor arrival numbers for September have recovered almost 90% of pre-covid peak levels. So hopefully it’s signalling towards another strong summer of tourism activity as it was last year. Though at the same time, we’re still seeing persistently weak levels of net migration and a large number of Kiwi departures – taking away from the economy’s demand pool and no doubt keeping the housing market subdued.

Another green shoot was seen with the Manufacturing PMI recording its fourth consecutive month at expansionary levels. Though at 51.4, where 50 marks the threshold between expansion and contraction, activity remains relatively subdued. Nevertheless, the sign of stabilisation in manufacturing is encouraging. The services sector still has a while to go yet. The PSI lifted to 48.7 from 48.3. So, largely a stabilisation at weak levels is the theme. Meanwhile consumer spending continues to disappoint. Retail spend was up just 0.2% in September. And most of that gain came just from elevated supermarket spending. Discretionary spend instead remains weak with spend on durables, apparel and hospitality all recording declines over the month. Households are being forced to prioritise costlier essentials over discretionary goods, and it shows. Looming job insecurity and the absence of a wealth effect certainly isn’t helping either.

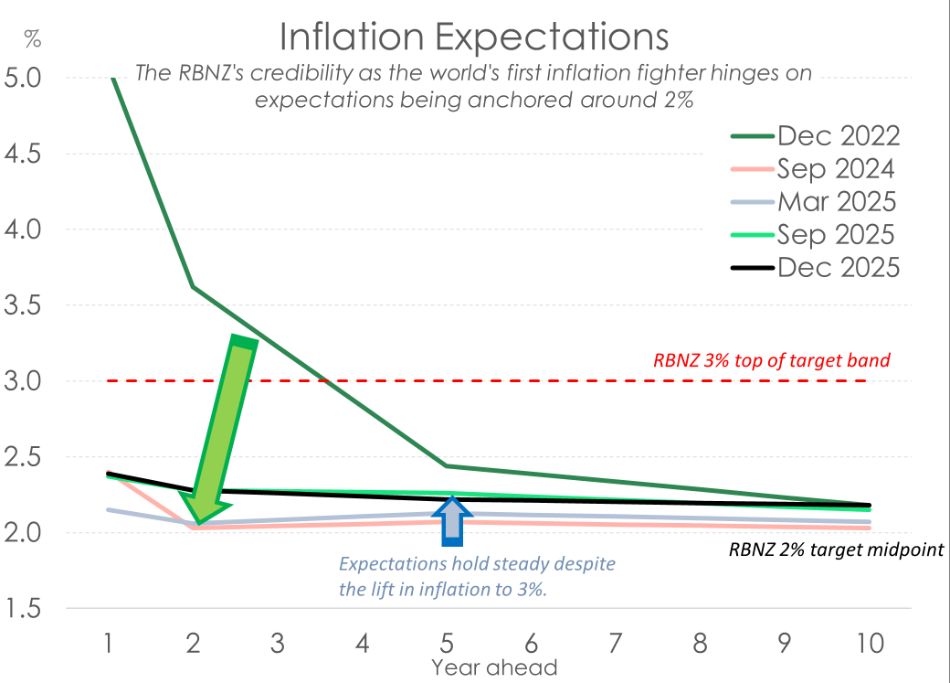

Chart of the Week: The anchoring of inflation expectations holds strong.

Expectations of inflation tend to follow actual inflation. So, with Kiwi inflation recently hitting 3% -the top end of the RBNZ’s target band - there was a risk that inflation expectations could follow suit and head higher too. That would have been unhelpful, and certainly not what the RBNZ would have wanted to see. And thankfully, they didn’t have to. The RBNZ’s latest Survey of Inflation Expectations showed inflation expectations well anchored around 2%.

Expectations for where inflation would be in 2 years time were unchanged at 2.18%. Meanwhile, expectations of inflation in 5 years time dropped 4bps to 2.22%. There were some marginal moves higher in the 1 and 10 year ahead measure. However at 2.39% and 2.18% respectively, the slight moves remain of no concern. All measures of expectations remain soundly within the RBNZ target band and close to 2%.

It's a result the RBNZ would have taken comfort in. And it further supports the delivery of a 25bps cut next week.

Event of the Week: Lunch with Professor Prasanna Gai.

It’s not everyday that we get to hear from a member of the RBNZ Monetary Policy Committee. But last week, we had the pleasure of hosting Professor Prasanna Gai at a Kiwibank client event. It was a great opportunity to gain some colour around how he views the current challenges our economy faces. We discussed plenty, with topics ranging from macroeconomics, monetary policy, financial markets, geopolitics and central bank independence.

Some of the key takeaways:

- Tariffs have acted as a negative demand shock. And the precautionary behaviour by businesses and households in response to the shock has offset some of the monetary easing delivered by the RBNZ.

- Pointing to a recent speech, central bank communication is critical, especially in times of heightened uncertainty. Central banker influence extends well beyond the policy rate and to the beliefs that govern private action.

- Ideally, a temporary spike or fall in inflation should both be looked through. But the initial conditions matter. The current state of the real economy influences to what degree a deviation from target inflation can be discounted.

- Theoretical concepts like a neutral rate or the non-accelerating inflaiton rate of unemployment (NAIRU) are difficult to draw on in practice. Because guesstimates can be so wide-ranging. In reality, you don’t know when you’ve reached these levels, until you’re past it. It will be the data that provides that discernment. For instance, just because the cash rate is in ‘stimulatory’ territory, doesn’t mean more is not needed if the economy has not responded.

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising