Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Saying Hej To The Swedes And Yay To The Economic Recovery. We’ve Got A Smörgåsbord Of Good News

- The recent stream of Kiwi data continues to show signs of recovery, particularly across the interest rate sensitive sectors of the economy. It’s what we’ve long been waiting to see. And what we hope to see more of into 2026. Lower interest rates are doing their job. The medicine is working

- The first opening of Swedish furniture giant IKEA, and Swedish central banker Dr Anna Breman commencing her role as RBNZ governor all in one week? Talk about coincidences! Taking the helm last week, Governor Breman appeared in front of the Finance and Expenditure committee and emphasised the Bank’s commitment to staying laser focused on its core mandate: keeping inflation low and stable.

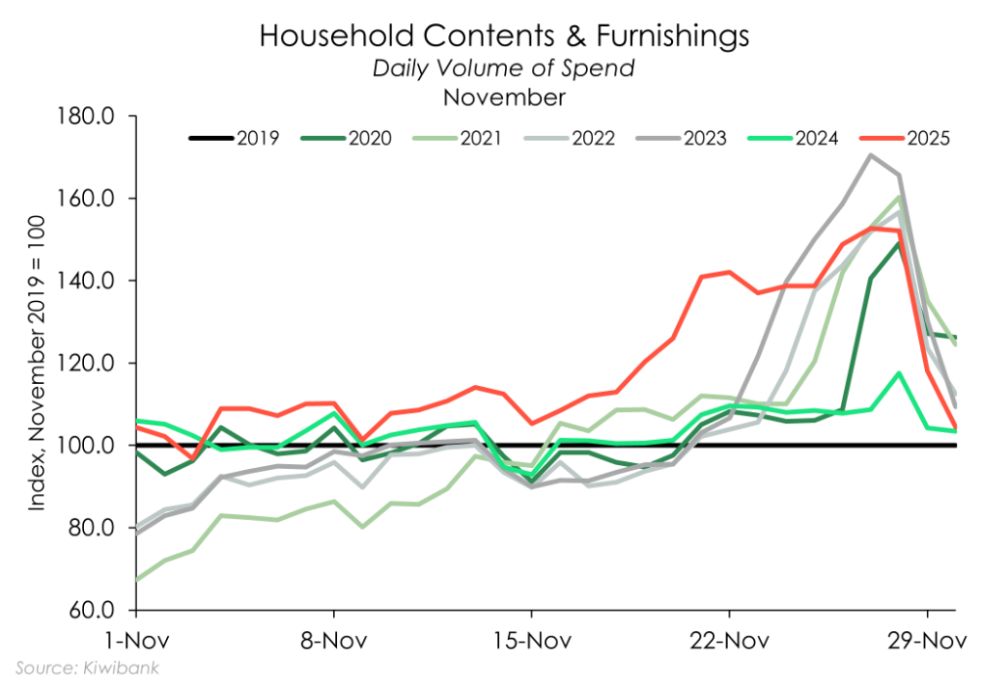

- Our COTW breaks down Black Friday sales. It appears that Kiwi are opening up their wallets, but to select stores. This year, Kiwi are choosing hammers over handbags and books over Bluetooth speakers.

Here’s our take on current events

The end of 2025 is fast approaching. And just in time for 2026, it looks like things are turning. The September quarter looks to have been a strong one for the Kiwi economy. That was always the expectation given the very weak starting point. Although we’d expect the June 0.9% decline in activity to be revised higher. Nonetheless, recent dataflow has been pointing to strong improvement in economic output over the third quarter of this year.

The most recent release of good news came from StatsNZ’s building activity data. The volume of building activity was up 1.5% over the quarter, well above the 0.2% lift expected by markets. Driving growth was the 2.8% uptick in residential volumes. Meanwhile non-residential building activity, down 1.3% over the quarter, continues in a downtrend with September marking the fifth consecutive quarter of declines for the sector.

Altogether, building activity appears to have found a floor. And looking at building consents, a leading indicator for activity, a pickup in construction appears imminent. Consents remain around 25% below from their 2022 highs, but have been on a general upswing since the middle of the year. The fall in interest rates over the year as well as the anticipation of a recovery in the housing market likely underpins the lift.

The strong building data comes hot on the heels of the solid retail sales print for the September quarter. Check out our review of it here if you missed it. But also, be sure to check out our COTW for some fresh Kiwibank data on spending over Black Friday. And by Black Friday, we really mean the whole month of November with sales kicking off well before the official calendar date.

It’s great to see the interest rate sensitive sectors of the economy finally responding. Overall, things are looking brighter as we wrap up the year and head into 2026. And it’s thanks to the steady decline in interest rates since last year. The medicine of lower interest rates is working.

But maybe the arrival of the Swedes helps too…

Talk about coincidences, Swedish furniture giant IKEA opened in Aotearoa the same week that Swedish banker and economist Dr Anna Breman steps into the role of Governor of the RBNZ.

Appearing in front of the Finance and Expenditure Committee (FEC) last Tuesday, Dr. Breman’s first remarks as Governor underscored the RBNZ’s commitment to staying laser-focused on its core mandate. That is, keeping inflation low and stable. Additionally, Governor Breman re-emphasized working towards improving the transparency and openness of the RBNZ. One potential step in that direction could be introducing voting attribution for monetary policy decisions. When asked about this during the FEC meeting, Breman noted it was something she’d like to discuss with the other Monetary Policy Committee members in time… so, we’ll see if that plays out. Nevertheless, whatever the path forward, greater transparency is something we look forward to. And with that we extend a warm welcome to Dr Breman to her role as Governor, and of course to Aotearoa.

Charts of the Week: Breaking down Black Friday

From spam in inboxes to flooded social media feeds, it’s that time of the year again – Black Friday. What began in the United States has gone global with many Kiwi retailers jumping on the bandwagon. The ‘unbeatable’ sales seemed to spring up everywhere you looked. The last Friday of November is officially the date. But with each year, the deals and discounts seemed to be advertised earlier and earlier. Indeed, looking at November monthly spend data for the past five years, the lift in volumes begins earlier in the month with each year – barring 2024 when the recession weighed on wallets.

We trawled through Kiwibank electronic card transactions and uncovered signs of a pick up in discretionary spending. The volume of spend on core retail is still down 1.5% compared to November last year. But by sub-category, it’s more of a mixed read. This year, it looks like Kiwi favoured hammers over handbags, couches over Converse, and books over bluetooth speakers. The volume of spend on clothing and footwear was down 9.7% on last year’s levels, while transactions at department stores fell 3%. Home electronics also recorded a 8.4% decline. But spend was up 1% at hardware stores and up 12% on all things household contents and furnishings. And as Kiwi are lounging on new hammocks, they’re reading the latest literature. The volume of spend on stationery and books is also up 6% compared to last year.

The lift in housing-related spend offers an encouraging sign for the housing market next year. The need for new furniture suggests increasing housing market turnover. While more trips to the hardware store sets up a summer of DIY. A lick of paint here, a mended fence there.

Overall, our data suggests that Kiwi are opening up their wallets more than last year – but they’re more selective with where their money is spent. For now, all things housing are the winners. But secret Santa and stocking stuffers may see more broad-based gains across retail this Christmas. Boxing Day also holds promise for more spending on toys – big and small.

REINZ: Buyer Activity Softens As Living Costs Remain A Consideration Across Key Regions

REINZ: Buyer Activity Softens As Living Costs Remain A Consideration Across Key Regions Better Taxes for a Better Future: Tax Policy Welcome Contribution, But Missed Opportunity To Tackle Wealth Inequality

Better Taxes for a Better Future: Tax Policy Welcome Contribution, But Missed Opportunity To Tackle Wealth Inequality Google Threat Intelligence Group - GTIG: Google Threat Report Warns AI-Driven Cyber Operations Are Scaling Across Global Threat Landscape

Google Threat Intelligence Group - GTIG: Google Threat Report Warns AI-Driven Cyber Operations Are Scaling Across Global Threat Landscape Commerce Commission: Baseline Research Report On The State Of Competition In New Zealand

Commerce Commission: Baseline Research Report On The State Of Competition In New Zealand University of Auckland: Junk Food Designed To Make Us Eat More, Study Finds

University of Auckland: Junk Food Designed To Make Us Eat More, Study Finds Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies