Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

New Vehicle Market Stabilises With Modest Growth In 2025

Market Overview

The new vehicle market strengthened in 2025 after a weak start, finishing the year ahead of 2024 despite softer results in December.

Registrations tracked higher year on year from June, with strong spring activity. December’s easing reflects typical year end timing rather than a change in underlying demand. Overall, the year marked a period of stabilisation, with activity recovering from earlier lows but remaining below longer term averages.

Motor Industry Association Chief Executive Aimee Wiley said that after a difficult start, 2025 marked a year of stabilisation for the new vehicle market.

“Activity lifted from mid year and finished ahead of 2024, supported by easing financial conditions and improving confidence, but demand remains measured. Buyers are prioritising value, practicality and suitability, whether that is in their choice of vehicle segment or motive power. What the data shows clearly is a market adjusting, with households and businesses being deliberate about the timing and scale of their purchasing decisions.”

Economic Context

Economic conditions improved through the second half of 2025, providing a more supportive environment for vehicle demand. GDP returned to growth in the September quarter and business investment showed early signs of recovery, including in transport equipment.

Interest rates eased during the year, with the Official Cash Rate reduced to 2.25 percent by November. Lower borrowing costs are flowing through to households and businesses, although labour market conditions remain soft and consumer spending uneven. Confidence improved toward year end, supporting larger purchasing decisions.

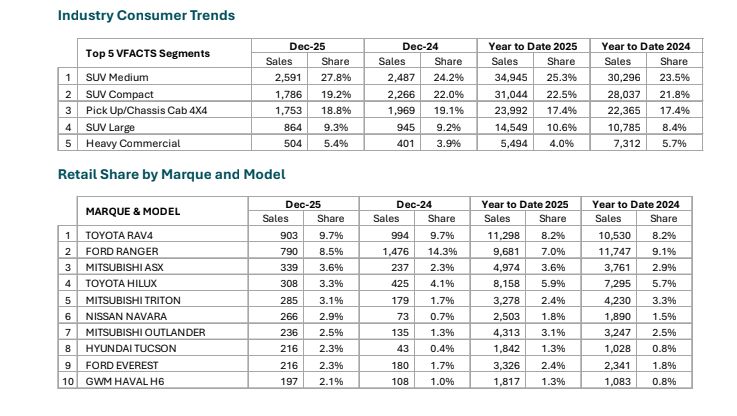

Segment Performance

Passenger vehicle registrations eased in December but finished the year ahead of 2024. Demand improved steadily through the year, moderated by pressure on household budgets and cautious purchase timing.

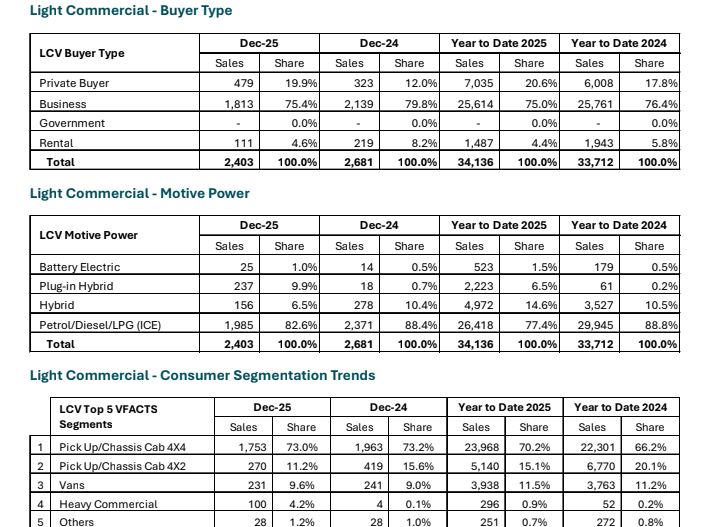

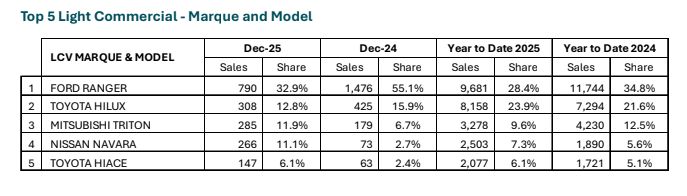

Light commercial vehicle volumes also eased in December but ended the year slightly higher than 2024. Business and fleet replacement demand remained supportive, with regional and

rural activity providing a degree of resilience, resulting in this segment holding up better than more discretionary areas of the market.

Heavy commercial vehicle registrations remained weak across the year. While December recorded a lift from a low base, full year volumes were well below recent levels, reflecting continued caution around large capital investment decisions.

Motive Power Trends

Motive power trends in 2025 differed across passenger and commercial segments, reflecting variations in use cases, cost considerations and operating requirements.

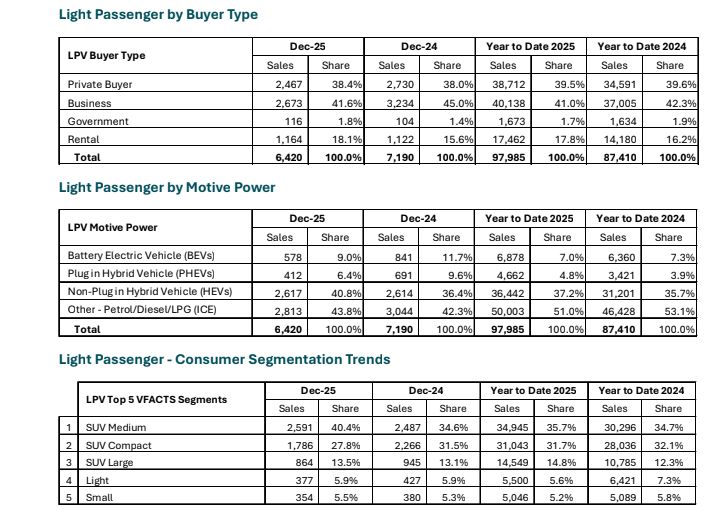

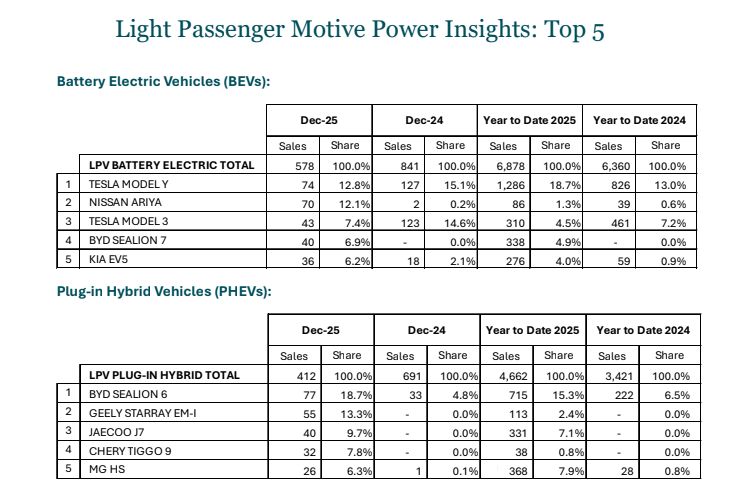

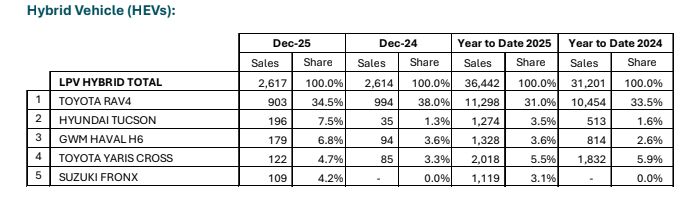

In the light passenger vehicle segment, non plug in hybrids increased their share year on year, while plug in hybrids also recorded a higher share than in 2024. Battery electric vehicle share remained broadly stable.

The growth in hybrid vehicles reflects their increasing availability at lower purchase prices, improved fuel efficiency and suitability across a wide range of everyday uses. As a result, hybrids are emerging as a practical sweet spot for many buyers, delivering emissions reductions without the higher upfront cost, charging or infrastructure considerations associated with full electrification.

In the light commercial vehicle segment, petrol and diesel vehicles remained dominant by share, although their share declined year on year. Hybrid and plug in hybrid uptake increased as new product offerings entered the market, supporting gradual adoption where operating requirements align. Battery electric vehicles also increased share from a low base, reflecting a measured transition as product availability expands and businesses assess suitability, cost and infrastructure readiness.

Summary

The 2025 calendar year did not signal a return to previous market highs, but it did mark a reset to more stable levels of demand. Activity finished clearly higher than in 2024, supported by easing financial conditions and improving confidence. Overall, the data points to a market recovering gradually, with households and businesses remaining selective about the timing and scale of their investment decisions.

Key Industry Insights

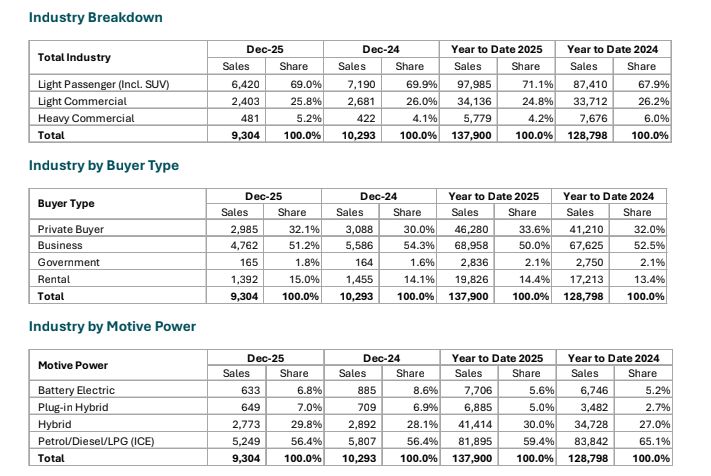

Total Industry Registrations: December 2025

A total of 9,304 new vehicles were registered in December 2025.

This reflects:

- A 9.8% decrease (-1,011 units) compared to December 2024.

- A 7.0% increase (+8,998 units) on a year-to-date basis.

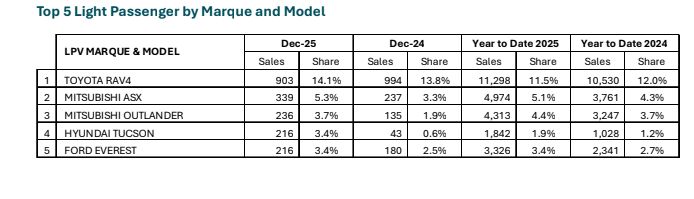

Light Passenger Insights (including SUVs)

Registrations: December 2025

6,420 units registered, an 11.0% decrease (-790 units) compared to December 2024 and a 12.0% increase (+10,548 units) on a year-to-date basis.

Light Commercial Vehicle Insights

Registrations: December 2025

2,403 units registered, a 10.4% decrease (-279 units) compared to December 2024 and a 1.3% increase (433 units) on a year-to-date basis.

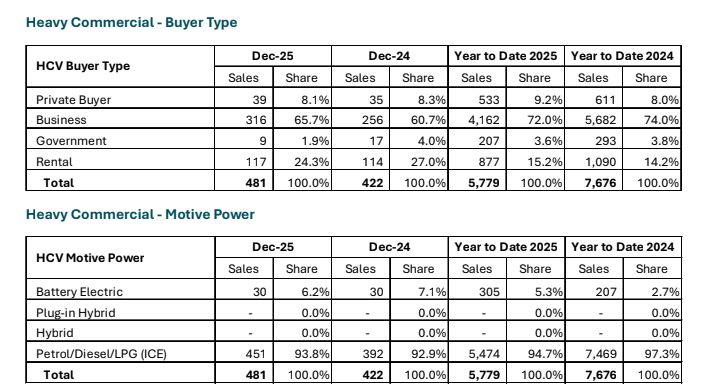

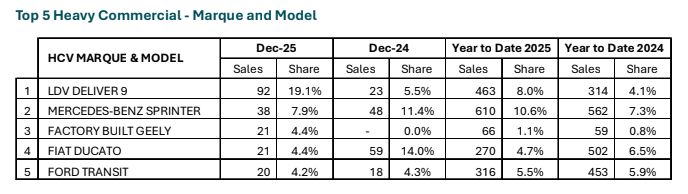

Heavy Commercial Vehicle Insights

Registrations: December 2025

481 units registered, a 13.7% increase (+58 units) compared to December 2024 and a 24.6% decrease (-1,892 units) on a year-to-date basis.

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows