Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

2025 In Review – How New Zealand’s Property Market Shifted From 2024

The New Zealand residential property market in 2025 was characterised by growing confidence and a return to stability and participation. Nationally, house prices remained broadly stable, and underlying market activity strengthened, reflecting improved confidence as interest rates eased and OCR reductions flowed through to buyer behaviour.

Data from the Real Estate Institute of New Zealand (REINZ) shows that national sales counts increased strongly compared to 2024, up 10.3% to 80,655, indicating that more buyers were willing and able to transact as borrowing conditions gradually improved.

However, that renewed activity did not translate into price acceleration, and prices remained largely steady. The national median house price edged slightly lower, down 0.6% year-on-year to $775,000.

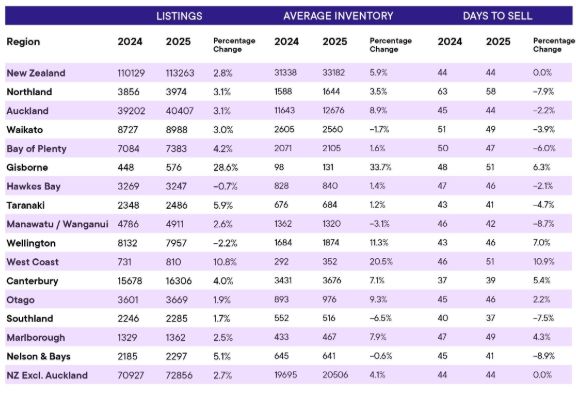

This combination points to a market where buyers re-engaged cautiously rather than competitively. First-home buyers in particular remained focused on affordability and value, and were unwilling to exceed the price considered reasonable and aligned with market value. At the same time, higher inventory levels nationwide shifted negotiating power toward buyers. Average inventory increased by 5.9% nationally, from 31,338 properties in 2024 to 33,182 properties in 2025, giving buyers more choice, reducing urgency and allowing them to act within their intended price range.

“Market activity strengthened in 2025, with a higher number of transactions, reflecting growing confidence compared to overall in 2024, influenced by factors such as lower interest rates. More sellers decided it was time to list their properties as well, so as buyers returned to the market, they had more choice and more negotiating power overall. Vendors who were willing to meet the market attracted strong buyer interest, while those who were slower to adjust experienced longer time on the market before revising their expectations to match market conditions,” says REINZ Chief Executive, Lizzy Ryley.

At a regional level, outcomes diverged depending on affordability and the balance between supply and demand. Stronger performance was evident in Southland, Otago and Canterbury, where demand proved more resilient and median prices lifted year-on-year. REINZ data show Southland’s median sale price increased by 6.3% to $489,000, Otago’s increased by 2.9% to $700,000, and Canterbury’s increased by 2.2% to $700,000 between 2024 and 2025. Lower price points in these regions meant buyers were less affected by borrowing constraints, allowing buyers to re-enter the market earlier and with greater confidence, even while interest rates remained elevated.

Supply conditions adjusted in parallel as sellers responded to improved market stability. Listing and inventory data supplied by realestate.co.nz show that more sellers returned to the market during 2025, including many who had previously delayed decisions amid market and economic uncertainty. New listings increased by 2.8% from 110,129 to 113,263 properties. While this expansion in supply helped keep overall price growth in check by giving buyers more choice, outcomes varied by region depending on how demand responded to the additional stock.

“Supply conditions further shaped market outcomes. realestate.co.nz data indicate that while listings and inventory increased nationally, supply-demand balance differed across regions. In Southland and Otago, inventory growth was more contained relative to demand, limiting downward price pressure. In Canterbury, although listings increased, demand recovered in parallel, supporting both a higher number of transactions and moderate price growth,” says Ryley.

Selling times reinforced the picture of a market that was functioning more evenly. Median days to sell were unchanged at 44 days nationally in both 2024 and 2025, according to REINZ historical market indicators. This stability reflects a market without the urgency of overheating or the prolonged delays typical of downturns. While some regions recorded faster selling times as demand improved, others experienced more measured conditions as supply rebuilt.

Looking to the latter part of 2025, sales counts, prices, and days to sell remained broadly steady through October, November, and December. This consistency is significant, as stable conditions tend to reduce uncertainty and support confidence among both buyers and sellers. Buyers continued to prioritise affordability, value, and location, particularly given elevated borrowing costs compared to historical levels. For sellers, stable late-year conditions reduced the incentive to delay further, as expectations became better aligned with market realities.

“Overall, 2025 marked a year of stabilisation rather than acceleration. The consistency observed through the final quarter of 2025 suggests that confidence had become more firmly embedded, rather than being driven by short-term reactions to individual economic events. This behavioural shift will be a welcome change for buyers and sellers, and provides an important foundation for understanding the market’s positioning as it moves into 2026,” adds Ryley.

Looking ahead to 2026, the market appears well-positioned for a more balanced phase, where any easing in interest rates could support gradual price growth built on already improving sales activity, rather than triggering rapid or unsustainable increases. The outlook suggests a balanced, sustainable property market phase rather than a return to previous volatility.

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies

Spark: New Report Sets Out Outcomes-Led Approach To Lift Rural Connectivity Using The Right Mix Of Technologies Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows