Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

What Are The Consequences Of New Zealand’s 20+ Year Complacency Toward Financial Crime?

Asia Pacific AML – Kerry Grass

New Zealand’s government is now reporting that the country is suffering from financial crime, experiencing a significant increase in corruption within the public sector and an infiltration of transnational organised crime. But how effectively has the New Zealand government performed in protecting its citizens from these harms?

A study of New Zealand’s 20+ year history reveals that the country has consistently turned a blind eye to the threats posed by serious fraud, corruption, transnational crime, and money laundering. Unfortunately, this complacency continues today.

What is the Harm of Financial Crime in New Zealand?

Financial crime—including fraud, scams, bribery, corruption, and money laundering—causes harm that extends well beyond direct financial losses. It erodes trust, distorts markets, funds other criminal activities, and can destabilise institutions. Effective risk management is a practical approach the government can take to translate broad legal obligations into consistent, defensible actions. However, the application of risk management to combat serious fraud, corruption, and transnational crime has been consistently overlooked by New Zealand’s leaders and the chief executive officers of relevant government agencies.

Data Science and Risk Management Are Essential to Combat Financial Crime

Protecting against financial crime requires a comprehensive approach, similar to any harm mitigation strategy. This includes the use of data science and a technology-driven "Risk Management" framework designed to maintain continuous vigilance against emerging threats.

Risk management acts as a control system that ensures a program to combat financial crime is auditable and proportionate. Such processes are critical when threats and vulnerabilities shift rapidly, as is often the case in financial crime.

Data drives the identification, monitoring, and reporting processes within a risk management framework. Utilising technology to process data transforms noise into prioritised actions and measurable outcomes, improving loss prevention and providing a focused investigative approach.

At a national level, effective risk management of financial crime helps to:

- Identify where financial crime is prevalent across the country.

- Assess and prioritise the likelihood and consequences of financial crime exposures.

- Establish necessary controls to mitigate identified risks.

- Implement ongoing monitoring and reporting to detect, prevent, and respond to known financial crime threats.

However, New Zealand has lacked these fundamental control measures, allowing financial criminals, including organised domestic and transnational groups, to target the country.

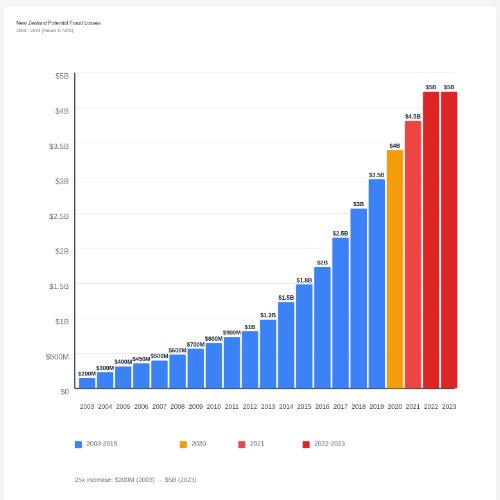

It therefore should come as no surprise that New Zealand has experienced a 25-fold increase over 20 years in crimes linked to serious fraud:

When no controls are in place to deter or monitor the risk levels of transnational crime, the consequences are that New Zealanders will suffer an increased rate of harm, and government agencies will fall prey to domestic and international organised criminals.

The data above shows that in 2003, the Serious Fraud Office (SFO) reported expected serious fraud levels at $200 million. By 2023, this figure had risen to $5 billion. This 25-fold increase over two decades illustrates the consequences of the Serious Fraud Office and other New Zealand government agencies failing to adopt technology-driven fraud prevention strategies and maintain continuous vigilance against emerging threats.

Analysis of New Zealand’s Increase in Financial Crime

2003-2019: Steady Growth Period

Fraud losses gradually increased from $200 million to $3.5 billion over 17 years, representing a 17.5-fold increase. This period reflects consistent growth as digital fraud became more prevalent and sophisticated.

2020: Escalation Begins

A significant jump to $4 billion marked the beginning of a critical escalation. The 14% increase from 2019 to 2020 signals a turning point, likely influenced by increased digital activity during global disruptions.

2021: Critical Increase

Fraud losses surged to $4.5 billion, a 12.5% jump from 2020. This rapid acceleration indicates an urgent need for enhanced fraud prevention measures and cybersecurity investments.

2022-2023: Peak Level

Expected fraud losses plateaued at $5 billion, representing the highest levels recorded. This peak reflects the maturation of fraud schemes and the need for systemic improvements in the fraud detection and prevention framework.

Evidence of New Zealand’s “Blind-Eye” Approach to Serious Fraud, Corruption, and Transnational Crime

Demonstrating New Zealand’s hands-off approach to preventing this economic crisis is not difficult.

As a member country of the United Nations, New Zealand has a contractual commitment to ratify conventions established by the United Nations Security Council (UNSC).

One only needs to refer to New Zealand’s delayed efforts in appointing an “Anti-Corruption Agency” under the United Nations Convention Against Corruption which was issued in October 2003. Had New Zealand acted responsibly, it would have established an Anti-Corruption Agency well before 2015. When New Zealand’s politicians did label a government agency as “Anti-Corruption” and “Anti-Bribery,” they merely rebranded the existing Serious Fraud Office without providing additional resources.

At that time, the Serious Fraud Office investigated less than 5% of complaints received, rendering parliamentary efforts to reduce harm ineffective and lacking integrity.

Adding more responsibilities to an already overwhelmed agency was meaningless and created more harm than good. This appointment merely created the illusion that New Zealand was operating with an Anti-Corruption Agency, while the reality was quite different.

What Does the Financial Crime Horizon Look Like for New Zealand?

The most powerful tool in New Zealand’s arsenal to protect its citizens from harm arising from domestic and international serious crime—including fraud, corruption, and money laundering—is the country’s Anti-Money Laundering and Countering Financing of Terrorism Act. However, for this tool to be effective, it must be tested to ensure it meets its intended function and maintained for ongoing performance.

Despite having decades to prepare for an effective AML/CFT compliance framework, recent responses to Official Information Act requests have confirmed that New Zealand has not implemented simple data-technology solutions to manage an AML/CFT supervisory framework.

As the Department of Internal Affairs (DIA) is set to become New Zealand’s single AML/CFT supervisor, all New Zealanders should be concerned that this regulatory function is not supported by data-driven technology systems. Consequently, the outlook for financial crime in New Zealand appears bleak.

Establishing a new ministry to consolidate the powers of government departments will not effectively manage the risks, especially when starting without adequate technology systems for data processing, monitoring, and reporting. Existing issues will likely persist in the new ministry, should it be established.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention