Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Air NZ Doesn't See A Competition Problem – Regional New Zealand Does

Comments today from Air New Zealand at the Transport and Infrastructure Select Committee that the airline does not see the lack of competition in New Zealand aviation as a problem will come as another blow to regional travellers and businesses, New Zealand Airports Association Chief Executive Billie Moore says.

"Regional New Zealand is living the reality of this every day. It looks like:

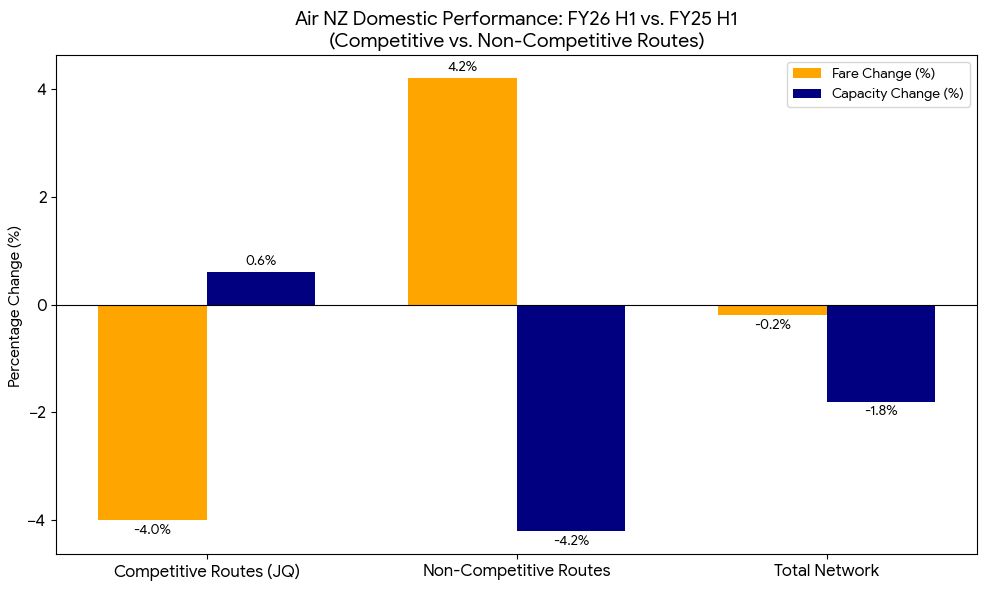

- More expensive regional routes. Air New Zealand is increasing fares on non-competitive domestic regional routes to offset pressure from Jetstar. Regional airfares are up 4.2% for this half of the year while available seats fell 4.2%. On routes with Jetstar competition, Air NZ dropped fares by 4% and increased capacity by 0.6%.

- Capacity cuts and full planes. Air New Zealand has reduced capacity at all but five of its domestic ports – and four of those five exceptions are airports where Jetstar operates. The airline is investing where it faces competition.

- The withdrawal of commuter flights that regional businesses depend on. With over 80% domestic market share, there is little risk another airline will step in to challenge Air NZ's decisions to cut early morning and evening flights. Regional businesses lose the flight times they need, with no alternative.

- No new planes for regional routes. There has been no meaningful fleet investment for the regional network. The Q300 turboprop fleet is aging and utilisation of these aircraft has declined to 62% of historical levels. This means far less flying, fewer seats in the market and higher costs being passed through to consumers.

- A less efficient airline. Without competitive pressure, Air New Zealand is carrying higher internal costs than international airlines operating in competitive markets.

- Managed decline for regional New Zealand. Domestic seat growth has been less than half the rate of economic growth since 2014. The network still has 1.5 million fewer seats than we had in 2019.

“We talk about competition not just because it drives lower airfares, but because it creates stronger businesses and less vulnerability for consumers.

“There’s no quick fix to get more airlines competing in the regions. But competitive disciplines can be applied through transparency and regulation, including airfare monitoring and Commerce Commission oversight.”

New Zealand operates the most concentrated domestic aviation market in the world among markets of comparable size, with Air New Zealand holding over 80% of domestic capacity and a monopoly on 80% of domestic routes.

“In this context, it is deeply frustrating to see Air New Zealand continue to point to airport charges as a reason for rising fares.

“Airports must invest in the essential infrastructure that the airlines need to run their businesses. Airport charges make up 7% of airline operating costs on average. A 10% increase in airport charges changes fares by 0.35-0.7%. Fuel, labour and aircraft costs have far greater impact. Airport charges simply do not drive airfare increases.”

NZ Airports welcomes Air New Zealand's statement today that it has no plans to withdraw from any of the 20 airports it currently serves.

"That commitment is important and we acknowledge it. It means we now need to work together to get the network into growth mode – with the investment, frequency, and service levels that regional New Zealand needs and deserves."

Notes:

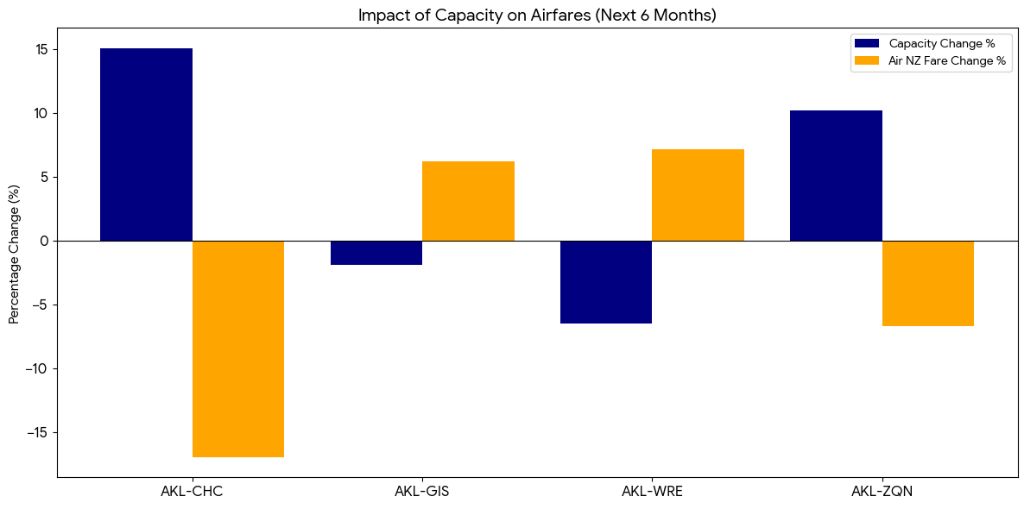

The below charts compare airfares and capacity between the first half of the year 2025 and 2026. Airfare reductions are almost exclusively linked to competitive pressure from Jetstar.

- Market capacity on Auckland-Christchurch is set to grow significantly, with Jetstar projected to increase its seat count from ~491k in 2025 to ~611k in 2026.

- Correspondingly, Air New Zealand's fare for this route has dropped by 16.9%.

- In regions where Jetstar does not operate, we see yield management. For example, Auckland-Gisborne is seeing a 6.2% increase in fares while capacity is being cut by 1.9%.

- Where Jetstar provides a choice, Air NZ has increased capacity (+0.6%) and dropped fares (-4.0%).

- On routes where New Zealanders have no choice, the airline has reduced capacity (-4.2%) and increased fares (+4.2%).

- The "total network" figures (-0.2% fare change) mask the pricing behaviour on regional and non-competitive routes.

Stats NZ: Petrol And Diesel Prices Continue To Rise In April 2026

Stats NZ: Petrol And Diesel Prices Continue To Rise In April 2026 Priority one: Regional Deal Strengthens Confidence In The Western Bay Of Plenty

Priority one: Regional Deal Strengthens Confidence In The Western Bay Of Plenty REINZ: Buyer Activity Softens As Living Costs Remain A Consideration Across Key Regions

REINZ: Buyer Activity Softens As Living Costs Remain A Consideration Across Key Regions Better Taxes for a Better Future: Tax Policy Welcome Contribution, But Missed Opportunity To Tackle Wealth Inequality

Better Taxes for a Better Future: Tax Policy Welcome Contribution, But Missed Opportunity To Tackle Wealth Inequality Google Threat Intelligence Group - GTIG: Google Threat Report Warns AI-Driven Cyber Operations Are Scaling Across Global Threat Landscape

Google Threat Intelligence Group - GTIG: Google Threat Report Warns AI-Driven Cyber Operations Are Scaling Across Global Threat Landscape Commerce Commission: Baseline Research Report On The State Of Competition In New Zealand

Commerce Commission: Baseline Research Report On The State Of Competition In New Zealand