Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

The Kiwi Currency Could Crumble In An Oil Crisis

- We’re fixated on the Middle East. The supply shock is pushing price pressure onto businesses and households already hurting. It’s the impact on demand that has us on edge. The price increase is one thing, a fuel shortage is another. And our economy is weaker than expected at this stage in the recovery. Demand destruction is unfolding.

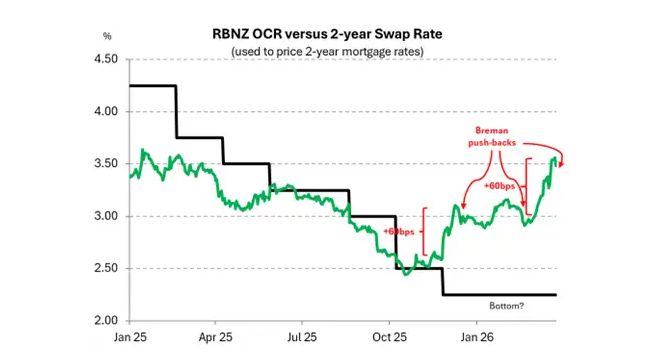

- The new RBNZ Governor has been called upon, for the third time in as many months, to cool things down. And Anna Breman continues to play her role well. Although it’s difficult when markets dry up, banks get faced the same way, and hedge funds vanish.

- As always, risks are abound. Rate hikes are priced in too early. The tightening in market conditions has gone too far. And the RBNZ agree. The Kiwi dollar may face some short-term weakness as market pricing recalibrates. And we might get a more dramatic move south, if the conflict escalates.

We started the year with rate hike expectations already priced in. And such elevated expectations were premature. But they persist. The dramatic disruption and uncertainty surrounding the Middle East conflict is creating immediate inflation pressures. In response, traders have doubled down and factored in even more rate hikes, coming earlier in 2026. But it is the demand destruction that’s missing from interest rate market sentiment. We say it again, rate market pricing is “way too aggressive and premature."

It’s worth pointing out the illiquidity in Kiwi rates markets. Much of the move in wholesale rates has been flow driven. That means banks are facing the same way, needing to pay swap rates, and are unable to find receivers (typically hedge funds) on the other side. Hedge funds are conspicuously absent. Hence, rates have gapped higher.

It will take time, but the fundamentals will eventually override the squeeze. And rates should fall back in line with more rational expectations. The risks to domestic and global demand are heavily weighted to the downside. And the RBNZ understand the risks, all too well.

Our new RBNZ Governor, Anna Breman is encouraging us to keep ice in our bellies, and keep cool, calm and don’t overreact – at least that’s what the RBNZ will do. With wholesale rates pricing in three rate hikes this year (down from almost 4), we think the market has a long way to go. There’s money on the table for traders willing to watch the RBNZ pause until they assess the damage. And that will take time. The war needs to end, and oil prices need to normalise. Something that may take many months.

Our view is that the increased uncertainty and high fuel costs flowing through the economy will cause households and businesses to pull back on spending. We could record another contraction in activity over the second quarter, before we have a chance to recover later in the year. It feels like 2025 all over again. The rise in the cost of petrol will cause inflation to rise, yes, but it’s already hitting wallets much harder. We came into the year expecting inflation to fall, starting in the low 3s. Now we are expecting inflation to stay at low 3s into the end of the year. This is no post-covid (7%) inflation boom. Demand is much softer now.

Just getting to work, and keeping the lights on, will be top of mind for many Kiwi households already weighed down by cost-of-living pressures. With a high unemployment rate (5.4%) and only 2% jobs growth in the last quarter, workers have very little bargaining power to increase their wages. So we don’t expect a wage-price spiral.

Given the risks, we think markets are overpriced, pricing in rate hikes that have a low chance of materialising. We are more likely to see businesses struggling to pass on higher operating costs to already cash-strapped consumers. And we are likely to see a crunching blow to our tourism industry. Both tourism and agriculture are sensitive to fuel price hikes and global trade disruptions. Our other goods exports may also face transport challenges.

Every hour a new headline from Trump speaks to ending the war, peace negotiations and total victory. While news of troops being deployed, more bombs being dropped and conflict escalating peppers the news cycle in-between. There’s been a lot for markets to react to. And yet the VIX index, which measures market volatility, aka market panic, hasn’t gotten anywhere near the levels we saw during covid, Russia’s attack on Ukraine, or liberation day (at least not yet).

We thought we would see more action from the Kiwi flyer (NZDUSD). We had a bumpy start to 2026, with a spread in the year to date of 4 cents (low 0.57 – hi 0.61). NZD was tracking up. We saw a move from a 0.58c year open to a 0.61c peak at the end of January, and we stayed hovering in that range until late February. Just like last year’s Liberation Day tariffs, the Iran conflict and subsequent disruptions to global oil supply served the Kiwi a blow. Oil trades in USD per barrel, so the weaker our Kiwi flyer is, the less oil we can buy with the same dollar. A weak NZD/USD exchange rate increases the cost of oil even further for the Kiwi economy, exacerbating the spikes in oil prices, peaking at $119USD for brent crude so far. This is nowhere near market records or the peak we saw at the beginning of the Russia-Ukraine invasion of $139USD per barrel. We don’t expect we’ve hit the peak in this crisis yet, and if the conflict is protracted, we could see new records being set. For now, all we can do is anxiously wait and see.

We’re seeing another interesting reaction (or lack thereof) in the NZD/AUD. It’s the lowest it’s been since June 2013, (0.82c). This is good news, at least in the short term, as Australia is a big export market for us, and for them NZ just became Briscoes, chronically on sale. With the Aussie economy still heating up according to the RBA, hopefully they can give us a boost on the way up.

Anything short of a quick resolution, a peace deal of sorts, could see the Kiwi falling further. That’s the dominant risk, in our view. A move into the mid-50s seems fair. At 58c today, we see a move back towards 56-57c as likely, given the crisis. 55c seems to be good resistance. But panicked selling into the low 50s, although unlikely at this stage, is not out of the realms of possibility. We would be surprised to see a move back into the 60s. Although that would represent good news.

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report