Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Slacklining Into 2026. Walking The Stagflation Tightrope

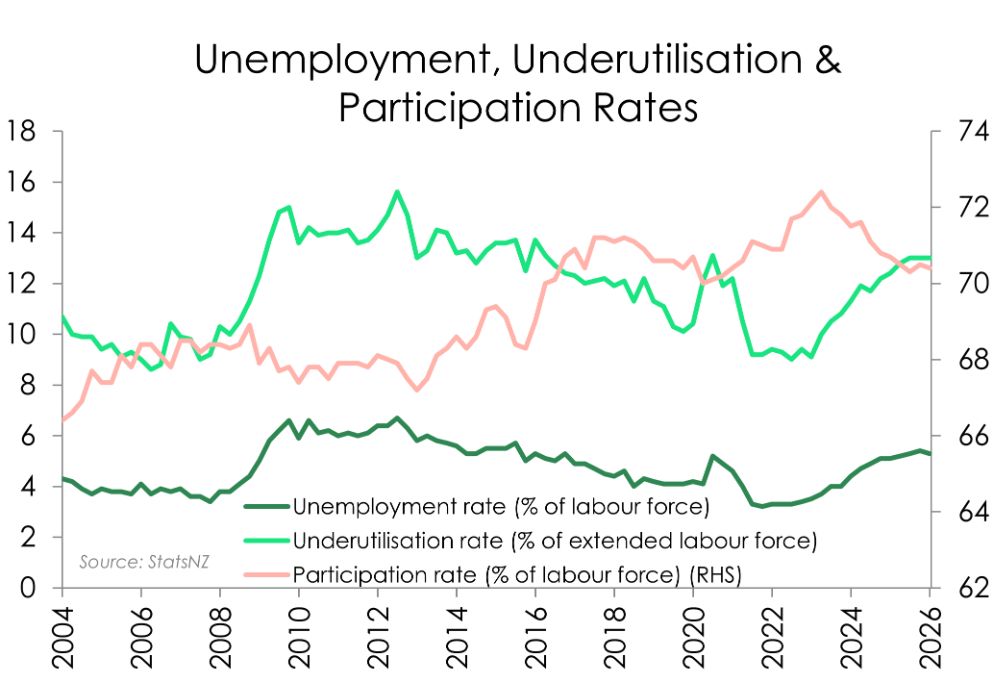

- The unemployment rate fell slightly from 5.4% to 5.3% in the March quarter. The labour force grew/shrank 0.1% over the quarter while the participation rate dropped to 70.4% from 70.5%. The underutilisation rate held steady at 13% (12.9% to be precise).

- Slack in the labour market is driven by business confidence, investment, hiring expectations, inflation expectations, uncertainty, and consumer confidence. All of which boils down to ordinary Kiwis and what they can and can’t afford to buy right now. And how much longer the war in the Middle East drags on for.

- The Kiwi labour market has a productivity problem (old). It’s likely to add stagflation to the mix (new). Prices are going up while demand is weak. With slack in the labour market, we aren’t likely to see wages go up. The RBNZ doesn’t need to hike rates to tighten. The economy is contracting all on its own.

We were expecting the Kiwi unemployment rate to hold steady at 5.4% in the March quarter. The data is out and it reads 5.3%, a tiny drop, but not much change.

The labour force grew 0.1% over the quarter while the participation rate dropped to 70.4% from 70.5%. The underutilisation rate held at 13% (12.9% exactly, in fact).

The news is neither too good nor too bad. The employment rate stayed the same, 66.7%, today. Momentum was building off the back of growth we saw in December of 2025. And employment growth lags behind a lift in greater economic activity, especially after a downturn.

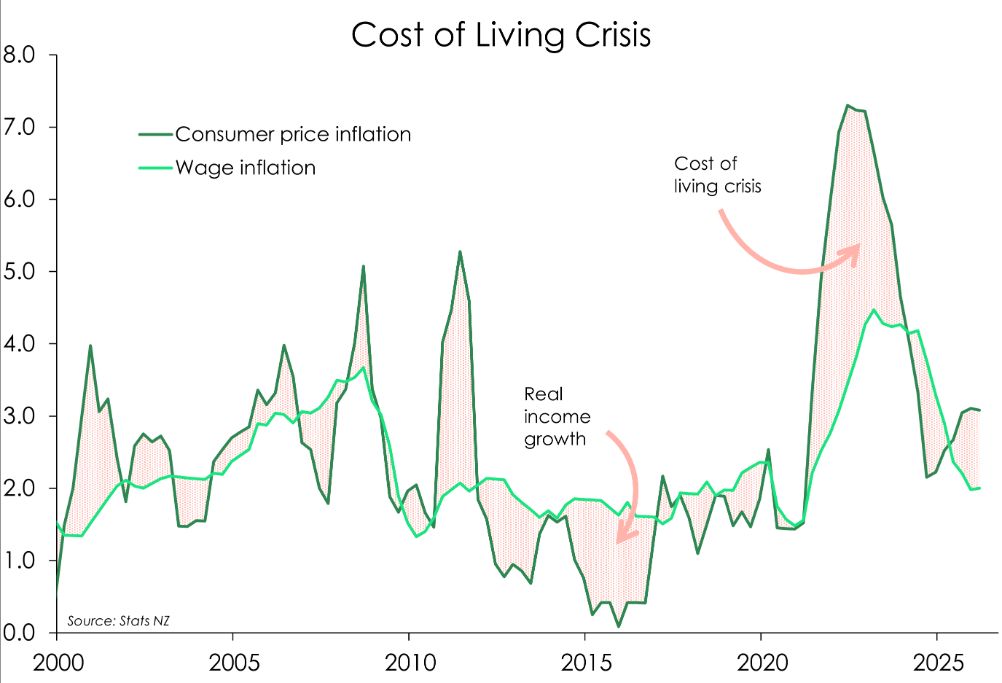

There’s still substantial slack left in the labour market. The underutilisation rate is still uncomfortably high. Wage growth stayed level at 2% as well, with most wage increases sitting in the 1-2% range. Remember the 4.3% wage increases of 2023? Well, despite the wage run rate sounding better, it came at a time of inflation bouncing between 6-and-7%. Our “cost-of-living crisis” has been with us for many a year. Far too many.

The spare capacity in the labour market plays a big role in how inflation gets passed on throughout the economy. And inflation remains uncomfortably above the RBNZ’s target band, while demand is being destroyed. Business confidence has taken a sharp fall, and Kiwi spending on non-essentials is down. The slack in the Kiwi labour market effects the RBNZ’s inflationary outlook. But there’s more to life than inflation…

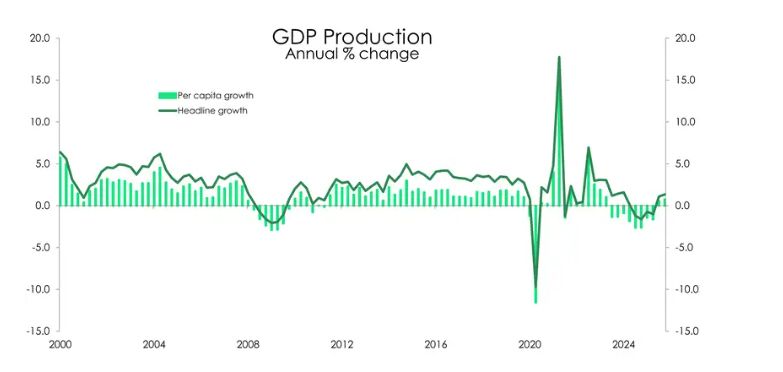

If we want to look at the health of our economy, we can also look at how much value we are producing per Kiwi (per capita GDP). Per capita GDP dipped following the GFC. The Kiwi economy experienced a long, drawn-out recession. During Covid we saw a very sharp dip again, as only essential services were open, and many industries (e.g. tourism) shut down.

Kiwis came out of lockdowns to record low interest rates, valuing their homes a lot more, and healthy savings thanks to government subsidies. This caused a massive spike in GDP as borders opened and people could leave the house again. To rein in the spike in demand, and demand driven inflation, the RBNZ embarked on the most aggressive tightening cycle seen in a generation. And yes, they drove the economy into another recessionary period. And we’ve been trying to claw our way out it ever since.

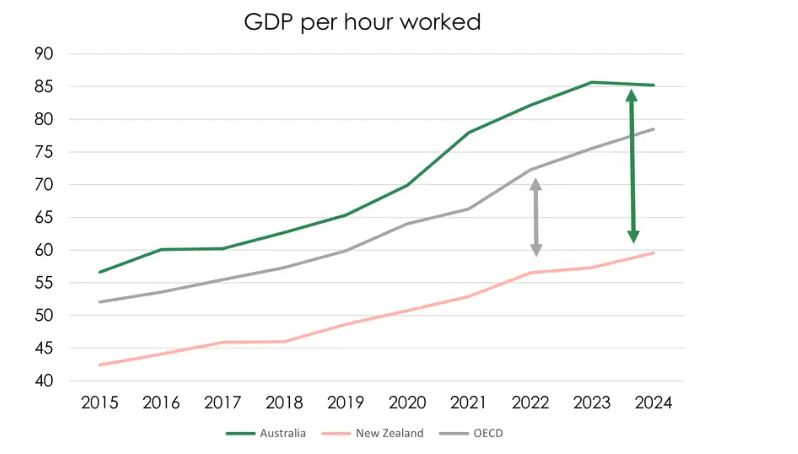

Another measure, our labour market productivity, tells us how well we’re making use of the Kiwi work force. One measure of productivity is how much value the Kiwi economy generates for every hour worked. New Zealand has ranked in the bottom half of OECD countries in this measure since 2000 and has fallen to the bottom 25% since 2020. But it gets worse! We’ve never peeked above the OECD average, compared to the Aussies who have never dipped below it. Ouch!

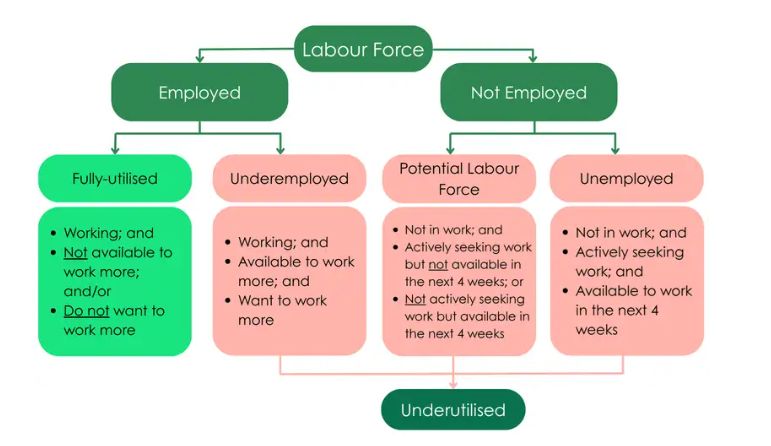

So why is our underutilisation rate so high and our productivity so low? To answer this, we first break down the labour force:

1 Fully-utilised workers – working Kiwis who either don’t want more hours or aren’t available to work more;

2 Underemployed workers – working Kiwis who aren’t only available to work more, but also want more hours;

3 Potential labour force – Kiwis that aren’t in work and either aren’t looking for work or aren’t available to start work in the next four weeks;

4 Unemployed – Kiwis that aren’t working but are available to start work in the next four weeks and are actively looking for work.

The underemployed, potential labour force and unemployed make up the underutilised workforce. These are the individuals who make up the “slack” we mentioned earlier.

Official statistics, like the ones out today, focus on this group, or on the unemployed. But the underemployment rate is at 5.0%, down slightly from last quarter, but still on the high side. So why are so many working Kiwis looking for more work? Do we have a shortage of hours?

Although many underemployed workers claim “not enough work available” as the main reason for their underutilisation, the statistics hint at a different story.

Underemployed workers are only working one hour per week less than their fully-utilised counterparts. For those working full-time, this equates to 40 hours worked by the underemployed Kiwi compared to 41 hours worked by a Kiwi who’s fully-utilised.

The key difference between the underemployed and the fully-utilised is not hours worked, but income. Part-time underemployed workers earn 28% less than their fully-utilised counterparts (33% for full-time workers).

The issue isn’t that underemployed individuals aren’t working enough hours, but that they can’t increase their incomes while working a 40-hour week.

Low-paying jobs tend to also be low-productivity jobs.

More low-paying jobs thus dilute productivity measures, such as GDP per hour worked. If the goal is to lift NZ’s productivity, reducing underemployment by offering Kiwis more low-wage hours won’t cut it. The Kiwi economy will benefit from growing the skills of underemployed workers so they can move into higher-paying roles – and, of course, making sure those jobs exist for them to move into.

How many high-paying jobs are being created ties directly into business confidence, which is anchored by inflation and (in)stability expectations. At present, uncertainty is high. The cost of running machinery, shipping and packaging has gone up due to the war in the Middle East. And the demand for their goods and services has gone down because households have less free money to spend. Will businesses put their prices up?

That’s where the RBNZ comes in…

The RBNZ is chiefly tasked with keeping inflation (price growth) low and stable, between 1% and 3%, with the 2% mid-point being the sweet-spot. To decrease inflation, the RBNZ can raise the official cash rate (OCR), making borrowing more expensive for businesses and regular Kiwis.

If the RBNZ lifts its rate, all borrowing costs (including mortgage repayments), gets more expensive. Business owners are less likely to borrow money to expand their operations, Kiwi mortgage holders are forced to spend more of their income on paying their loans, leaving less available for everything else – driving down demand for goods and services in the Kiwi economy.

But Kiwi households are already cutting back on spending where they can. The cost of essentials like electricity, food, rates and insurance have all gone up, and now we have petrol on top.

Due to increased prices, businesses are also cutting back on their own spending, not hiring new staff, not expanding their operations, not giving out bonuses or pay increases. Wage growth will be stifled, and unemployment and underutilisation will remain relatively high, if not increase.

So why would the RBNZ need to hike rates? The economy is contracting all on its own. Stagflation is the word for this situation. Low to no growth, but high inflation.

These effects don't happen overnight. In 6 to 12 months we’ll see the impact on the wider economy. That's the horizon the RBNZ is looking at. The labour market data from the March quarter of 2026 won’t influence the OCR in either direction. It’s still a wait and see situation.

The current crisis – and a thought experiment

Imagine you are a business owner, whose cost of operating just went up substantially due to petrol costs rising. You’re facing some tough decisions, how much of this cost can you shoulder before your business runs out of money? How much of this cost can you pass on to the already cash-strapped Kiwi consumer who’s already shouldering two years of a cost-of-living crisis? You’re stuck between a rock and a hard place.

Now imagine your workers comes to you for a pay rise (or more hours), citing the increased cost-of-living and the cost of getting to work. In times like these, employers simply can’t afford to increase wages. They may look to that pool of underutilised Kiwis, desperately looking for an income (or a higher one). Chances are they will find some very brilliant and qualified Kiwis in that pool… Kiwis willing to work for a lot less than that pay rise their employees are asking for. They’re unlikely to cave to any pay-rise demands. They might even replace existing workers with someone who is more qualified and desperate to have any income at all – that’s the effect of the slack in the labour market.

This example is being played out across the motu, and it illustrates why, when prices go up due to a supply-side shock and we have a lot of slack in the labour market, we aren’t likely to see wages go up. Therefore, we aren’t going to see inflation pass through into higher wages that will keep operating costs elevated after the oil crisis ends.

That’s one of the chiefly reasons why, the RBNZ targets medium-term inflation, not short-term. Sometimes we have inflation spikes driven by short-term price increases that don’t drive demand up. They therefore fade out of the economy quickly. It would make no sense for the RBNZ to hike to OCR today (or next month or even the month after that). Only after the conflict in the Middle East is resolved, and oil prices settle back down to (a new) normal, will they be able to truly measure if inflation is going to stick around.

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction New Zealand Young Physicists Trust: Auckland To Host The ‘World Cup Of Physics’ In 2027; Search Begins For Student-Designed Tournament Logo

New Zealand Young Physicists Trust: Auckland To Host The ‘World Cup Of Physics’ In 2027; Search Begins For Student-Designed Tournament Logo