Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

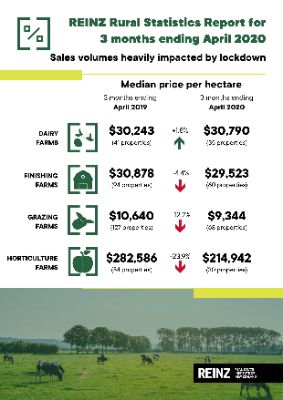

Sales Volumes Heavily Impacted By Lockdown

Data released today by the Real Estate Institute of New Zealand (REINZ) shows there were 111 less farm sales (-30.7%) for the three months ended April 2020 than for the three months ended April 2019. Overall, there were 251 farm sales in the three months ended April 2020, compared to 281 farm sales for the three months ended March 2020 (-10.7%), and 362 farm sales for the three months ended April 2019. 1,167 farms were sold in the year to April 2020, 19.0% fewer than were sold in the year to April 2019, with 28.8% less Dairy farms, 19.9% less Grazing farms, 29.6% less Finishing farms and 17.2% less Arable farms sold over the same period.

The median price per hectare for all farms sold in the three months to April 2020 was $22,660 compared to $22,624 recorded for three months ended April 2019 (+0.2%). The median price per hectare increased 7.2% compared to March 2020.

The REINZ All Farm Price Index rose 0.2% in the three months to April 2020 compared to the three months to March 2020. Compared to the three months ending April 2019 the REINZ All Farm Price Index fell 8.8%. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors.

Two of the 14 regions recorded an increase in the number of farm sales for the three months ended April 2020 compared to the three months ended April 2019, namely Otago (+3) and West Coast (+2). Bay of Plenty recorded the most substantial decline in sales (-23) followed by Taranaki (-16). Compared to the three months ended March 2020, four regions recorded an increase in sales with the biggest increases being in Otago (+7) and Taranaki (+3).

Advertisement - scroll to continue readingBrian Peacocke, Rural Spokesman, at REINZ says: “Just as March 2020 will be remembered for the start of the COVID-19 constraints, April 2020 will be remembered as the month when, throughout most of New Zealand, sales volumes plunged, particularly when compared to the same period in 2018.

“The reductions from 2018 to 2020 for the period are as follows: dairy (-47%); finishing (-45%); grazing (-38%); arable (-24%); horticulture (-42%)."

“The 3-month figures referred to above camouflage the direct impact for the month of April alone compared to April 2018 alone which are: - dairy (-58%); finishing (-31%); grazing (-50%); arable (-28%); horticulture (-85%)."

“In other respects, the lockdown has had less impact on the farming community in that being an essential industry, day-to-day activities have continued as opposed to workplaces which were deemed to be non-essential, being shut down throughout the rest of the country.

“Export prices have reflected the mix of market access restrictions and drought-induced access to meat processing facilities, the latter being exacerbated by Level 4 constraints which required separation between members of the workforce, which in turn reduced throughput by up to 50%.

“The future well-being of the rural sector will now be even more influenced by climatic factors which have exposed the vulnerability of the sector, albeit the reduction in interest rates and the reduced exchange rate will be of benefit.

One of the key determining factors for the future, however, will be the response from the trading banks regarding supplying sufficient capital for the requirements of the primary industries,” he concludes.

Points of interest from around the country, inevitably constrained, are as follows:-

- Northland/Auckland - very light sales activity in the dairy and drystock markets, although several strong sales of finishing units were recorded I the Rodney and Franklin districts

- Waikato/Bay of Plenty - hard work in the dairy sector with 2 moderately-priced sales and a reduced number of sales of finishing and grazing units in the Waikato and King Country; minimal activity throughout the Bay of Plenty/Rotorua regions with just one avocado orchard being sold

- Gisborne/Hawke’s Bay - tough times throughout the eastern portion of the North Island where drought conditions are causing real grief with no sales of pastoral properties recorded

- Taranaki - improved activity on the western side with several dairy farms and grazing properties being sold, although prices reflected variable quality

- Manawatu/Wanganui - sales recorded in the drystock and arable sectors with the more consistent activity again showing up in the Tararua district

- Wairarapa/Wellington – light activity in grazing and finishing categories

- Nelson/Marlborough - lean times in this region with just one smaller grazing property sold

- Canterbury/West Coast - a light smattering of activity throughout the province with 2 grazing sales in the north and 2 solid sales being a dairy unit and an arable property in the Ashburton district; no farm sales recorded on the West Coast

- Otago - one of the two brighter spots in the South Island with a cross-section of healthy sales of dairy, finishing, grazing and arable sales evenly spread over the central and eastern districts with Dunedin and Clutha taking the honours

- Southland - the second of the bright spots in New Zealand with strong activity at healthy prices in all categories with finishing units being particularly strong in price and volume.

Grazing farms accounted for the largest number of sales with a 27% share of all sales over the three months to April 2020, Finishing farms accounted for 24%, Dairy accounted for 14% and Horticulture accounted for 12% of all sales. These four property types accounted for 77% of all sales during the three months ended April 2020.

Dairy Farms

For the three months ended April 2020, the median sales price per hectare for dairy farms was $30,790 (35 properties), compared to $30,299 (37 properties) for the three months ended March 2020, and $30,243 (41 properties) for the three months ended April 2019. The median price per hectare for dairy farms has increased 1.8% over the past 12 months. The median dairy farm size for the three months ended April 2020 was 123 hectares.

On a price per kilo of milk solids basis the median sales price was $32.97 per kg of milk solids for the three months ended April 2020, compared to $32.55 per kg of milk solids for the three months ended March 2020 (+1.3%), and $31.78 per kg of milk solids for the three months ended April 2019 (+3.8%).

The REINZ Dairy Farm Price Index rose 3.2% in the three months to April 2020 compared to the three months to March 2020. Compared to April 2019, the REINZ Dairy Farm Price Index rose 2.5%. The REINZ Dairy Farm Price Index adjusts for differences in farm size and location compared to the median price per hectare, which does not adjust for these factors.

Finishing Farms

For the three months ended April 2020, the median sale price per hectare for finishing farms was $29,523 (60 properties), compared to $29,372 (67 properties) for the three months ended March 2020, and $30,878 (94 properties) for the three months ended April 2019. The median price per hectare for finishing farms has fallen 4.4% over the past 12 months. The median finishing farm size for the three months ended April 2020 was 32 hectares.

Grazing Farms

For the three months ended April 2020, the median sales price per hectare for grazing farms was $9,344 (68 properties), compared to $9,663 (79 properties) for the three months ended March 2020 and $10,640 (127 properties) for the three months ended April 2019. The median price per hectare for grazing farms has fallen 12.2% over the past 12 months. The median grazing farm size for the three months ended April 2020 was 132 hectares.

Horticulture Farms

For the three months ended April 2020, the median sales price per hectare for horticulture farms was $214,942 (30 properties), compared to $220,718 (31 properties) for the three months ended March 2020 and $282,586 (54 properties) for the three months ended April 2019. The median price per hectare for horticulture farms has fallen 23.9% over the past 12 months. The median horticulture farm size for the three months ended April 2020 was 7 hectares.

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction New Zealand Young Physicists Trust: Auckland To Host The ‘World Cup Of Physics’ In 2027; Search Begins For Student-Designed Tournament Logo

New Zealand Young Physicists Trust: Auckland To Host The ‘World Cup Of Physics’ In 2027; Search Begins For Student-Designed Tournament Logo Oxfam Aotearoa: Top CEO Pay Increased 20 Times Faster Than Workers’ Pay In 2025

Oxfam Aotearoa: Top CEO Pay Increased 20 Times Faster Than Workers’ Pay In 2025 Bill Bennett: TUANZ Report - Networks Built, Value Missing

Bill Bennett: TUANZ Report - Networks Built, Value Missing