Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

It’s An Eventful Week Ahead

Here’s our take on current events

It's a big week. For us of course, our focus is on the RBNZ’s Monetary Policy Review on Wednesday. After six straight meetings delivering rate cuts, totalling 225bps, the RBNZ looks set to take a breather.

The last time we heard from the RBNZ was, simply put, kind of weird. The May statement read dovish, with forecasts for the Kiwi economy appropriately downgraded. Similar to our house view, the RBNZ were clear to point out that trade uncertainty presents downside risks to growth and inflation. But the communication by RBNZ officials, along with the 1-5 dissenting vote, stopped short in signalling an easing bias consistent with their outlook and OCR track.

Market pricing allows the RBNZ to skip this meeting, and come back in August without causing a stir. Just 3bps of a cut (12% chance) is priced in for Wednesday. For August, the market is pricing in 16bps (just shy of a 65% chance) of a rate cut.

Wednesday’s decision is another case of what we think they should do versus what we think they will do. While a hold is the likely outcome, we recommend a cut. The need for lower rates is clear. The RBNZ themselves have signalled the need for further cuts. So why wait? Yes, there is worry right now about the recent spike in inflation we’re experiencing. But monetary policy makers must look through short-term volatility, even if it’s eye-watering.

Monetary policy is set today to influence the medium-term. And risks to the medium-term outlook are skewed to the downside. A global growth slowdown is expected with US tariffs. NZ export prices may come under pressure. Also, significant spare capacity remains within the Kiwi economy. Both these factors are disinflationary. And we’ve seen that in the QSBO survey. There is a net 2% of firms looking to reduce their prices in the coming months. History tells us that pricing behaviour like that only happens during recessions. All up, the real risk is that inflation undershoots the RBNZ’s 2% midpoint.

While the RBNZ may not pull the trigger this week, we expect them to maintain a dovish bias due to the balance of risks.

Beyond the RBNZ, we’ll also hear from the RBA this week. Meeting tomorrow, the RBA is expected to resume their easing cycle and deliver a 25bp cut to 3.60%. Having been late to hike, the RBA has also been late to cut. A cut tomorrow would mark just the third in this cycle. Compared to the 6 cuts we’ve had here at home. But the tides have turned. While the RBNZ has turned more ambiguous, the RBA has become more dovish. Because Aussie inflation is sitting at the lower end of the RBA’s target band, and the labour market starting to lose its lustre.

And of course, we can’t forget that July 9th (US time) marks the deadline of President Donald Trump’s 90 day pause on reciprocal tariffs. Now, with just 3 deals across the line out of the 70+ countries who were set to come to the negotiation table, an extension of some sort seems likely. That, or a mad dash of deals to the finish line for negotiations. Although we’re now also hearing about a more ‘Dear John’ letter-style approach from Trump with the White House set to send letters to countries outlining its new tariff rate.

Still, as we all know, no one can truly predict Donald Trump’s next move. We expect a route of de-escalation to remain the path forward. But we remain wary of the risks at present. Just last week, Trump threatened Japan with a 30-35% tariff rate, up from their 23% liberation day tariff, if a deal wasn’t reached before the July 9th deadline. Again, maybe it’s just more big talk, but it’s a reminder that no de-escalation is yet set in stone. And in any case, the ante is high over this week as we wait for developments to unfold.

At least in some semi-positive news, a trade deal was struck between the US and Vietnam last week. Under the deal, the US will now impose a 20% tariff on Vietnamese exports, compared to the 46% announced on Liberation Day, but higher than the 10% of the last 3 months. Additionally, the agreement also sees the US implementing a 40% tariff on any products originating from another country sent through Vietnam for final shipment to the US – a shot likely fired towards China. Meanwhile in exchange, Vietnam is giving the US tariff-free access to its markets.

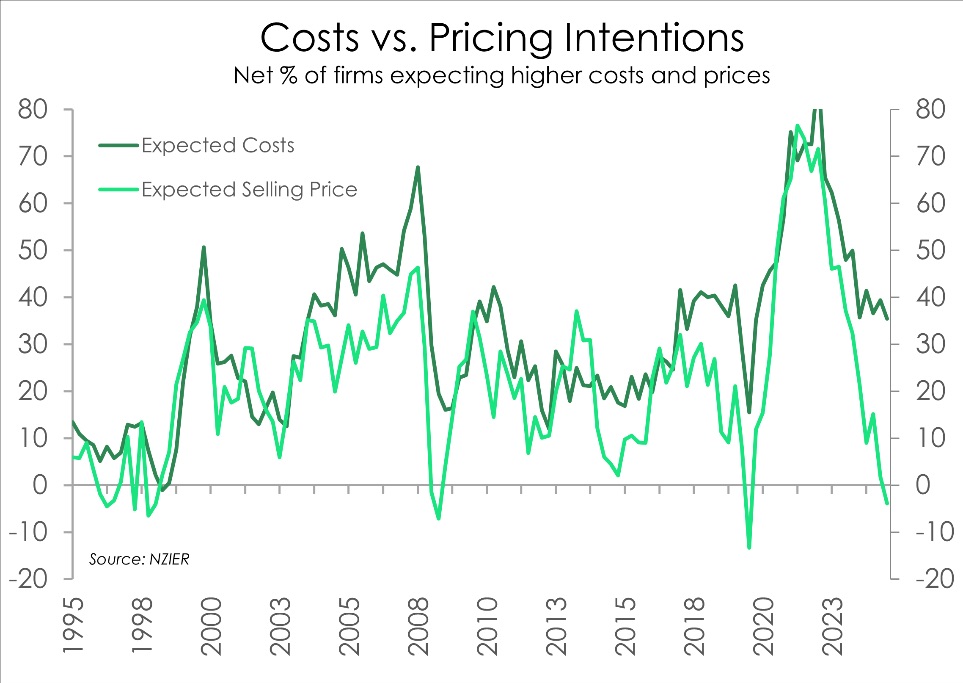

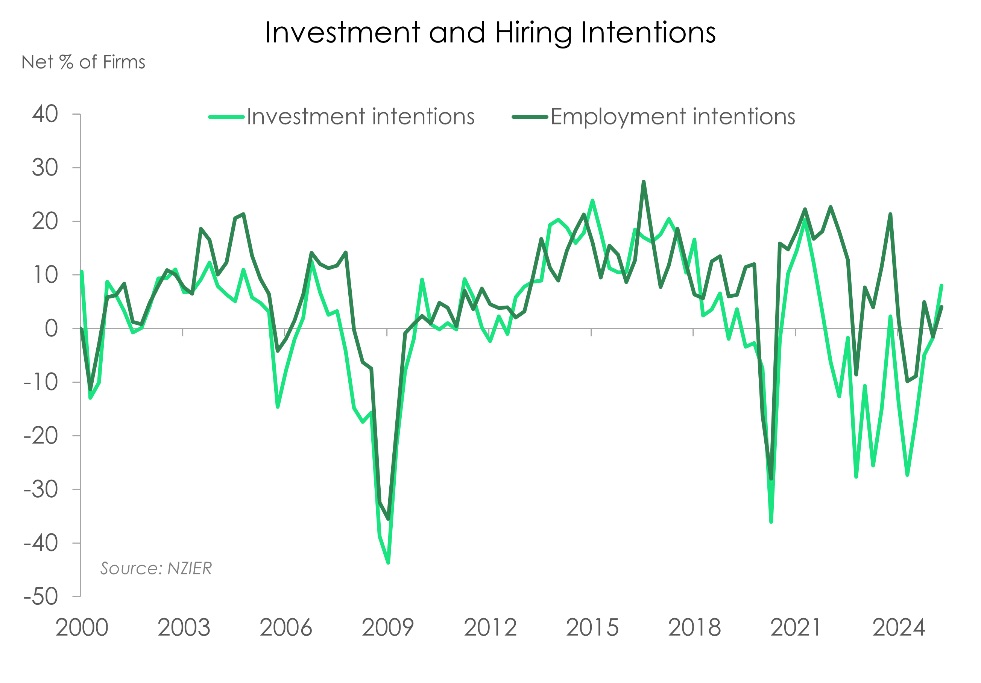

Charts of the Week: The “on the ground” business feel.

Last week’s Quarterly Survey of Business Opinion by NZIER showed that the gap between hopeful optimism and the harsh reality of daily business, continues to widen. Meanwhile firms are saying they are feeling less price pressure and passing on less pressure. The argument for stimulatory monetary policy is unequivocal.

Price-related indicators suggest that inflation remains well-contained. Both cost and pricing indicators eased over the June quarter. Fewer firms reported an increase in costs, from half of firms to a net 42%. The improvement was likely supported by the recent appreciation in the Kiwi dollar after starting the year on the backfoot (trading in the 55-56c range). At the industry level, the experience however is mixed. Fewer retailers experienced higher costs over the quarter, while cost pressures have intensified in the building sector. A net 59% of builders reported increased costs, up from net 35% in Q1). Despite this, the building sector reported the biggest fall in pricing – from a net 3% raising their prices last quarter, to a net 35% decreasing their prices. Meanwhile, pricing across retailers held steady. Overall, the weak demand environment continues to weigh on firms’ pricing power. A net 1% of firms had dropped their prices over the quarter, and a net 2% expect to do the same in the coming quarter. Outside of the Covid pandemic, 2009 was the last time the survey pointed to an expectation for price declines.

Another piece of good news to come out of the survey was the long awaited lift in investment intentions. After 13 consecutive quarters of negative investment intentions (excluding a short-lived blip following the election), investment intentions are finally back in the black. Well, mostly. A net 1% of firms are still planning on reducing investment in buildings. But a net 8% of firms are planning to get back to investing in plant and machinery over the coming year. The Government’s “Investment Boost” scheme has likely helped get some firms off the side lines. But we imagine others will still be holding off until they have more conviction about a sustained recovery in demand. Looking over at hiring, firms continued to cut headcount over Q2, though fewer than over Q1. A net 12% of firms reduced staff numbers in the June quarter compared with the net 17% in the March quarter. Although it seems hiring in the quarter ahead seems more promising with a net 4% of firms looking at expanding headcount.

Check out our full review – Reality bites, as business optimism improves.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention