Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

More Deals Done. We Need That. Because We’re Struggling With Uncertainty Across The Motu

- The focus remains on U.S. trade policy as the August 1st deadline approaches. There’s been meaningful progress, with major deals announced from Japan and the EU over the last week. But even as tariff rates ease from their Liberation Day highs, we’re still heading into a world that’s less open than we’ve seen in the last century.

- Our COTW looks at weakness in domestic inflation. Construction costs in particular have been growing at lower rates reminiscent of the GFC. Administered inflation, frustratingly, remains elevated.

- It's one of our favourite times of the year where we've done a deep dive into the performance of our regions. On average economic scores continued to defrost across the motu. But our regional heatmap is still mostly flashing 3s and 4s out of 10.

Here’s our take on current events

The next tariff deadline looms. August 1st is now just around the corner. And it’s the date marked in our calendar where we’re set to see Trump’s vast number of reciprocal tariffs applied onto US imports. Though slipping in before the curtain falls, more trade deals surfaced over the last week.

Among them, Japan and the US revealed an agreement that sets Japan’s reciprocal rate at just 15%. That’s down from its “liberation day” rate of 23%, and well below the more recently threatened rate of 30-35%. But the real headline was that the 15% rate would also extend to automobiles and car parts, rather than facing the universal 25% levy on the automotive sector. While in exchange, Japan is set to further open its economy for US imports along with investing $550bn USD into the United States.

And after months of difficult negotiations, the EU and US finally announced a deal over the weekend too. Like Japan, the EU will now receive just a 15% tariff rate that will also extend onto the automotive sector. While again, in exchange, the EU is set to invest $600bn USD into the United States and zero tariffs on US exports.

Despite the progress made and additional trade deals secured, this Friday will still mark a significant step up from the baseline10% tariff all countries have faced. But at the very least, it’s clear that the worst appears to be behind us in terms of uncertainty and erratic policy shifts. That alone should help businesses move forward from here.

Domestically, our focus was on the Kiwi inflation print last week. As expected, Kiwi inflation accelerated over the June quarter. Annual headline inflation rose to 2.7% from 2.5%. It’s a move in the wrong direction. But context is key. A strengthening in imported inflation is driving headline higher. But domestic price pressures, on balance, continue to cool. Yes, stubborn inflation persists across administrative prices, from council rates, energy and insurance costs. But these are all areas that largely fall outside the Reserve Bank’s control. Meanwhile, the interest rate-sensitive components of the consumer price basket remain notably weak (see our COTW for more).

So, while headline inflation may be rising, the underlying momentum is softening. And that distinction is crucial for the Reserve Bank. Spare capacity within the Kiwi economy is keeping downward pressure on domestically generated inflation and is set to keep inflation within the RBNZ’s target band over the medium term. And overall, with core inflation contained and interest rate-sensitive components of the CPI basket still weak, the June print reinforces the case for an August rate cut. And rightly so. Because the Kiwi economy still isn’t where it should be…

We recently conducted our annual deep dive into the regions and found that while most regions are performing better than last year, they’re still far from their best. The average score across the motu lifted from a 3 out of 10 to 4. The full report is well worth a look at. It’s one of our favourites to put together and is packed with insights from our business bankers across the country. But summing it up, the South Island continues to outperform the North. Otago joined Southland as the top two performing regions, with activity boosted by a bounce back in tourism. While Auckland’s activity is still weak, despite strong population growth. And for different reasons, economic scores for Northland, Gisborne and Taranaki deteriorated. Meanwhile, Wellington is thawing from its Jack Frost score of just 2 last year.

Without a doubt, it’s still tough for many to navigate the tumultuous economic environment. And there’s now an added challenge of a tariff-induced slowdown in global growth. The good news is that interest rates have fallen a long way from this time last year. There’s a Nazaré-type wave of mortgage refixing due. The move onto lower rates should help improve household disposable incomes, boosting consumption, supporting the housing market and wider business activity. But we may have to wait until summer for things to heat up.

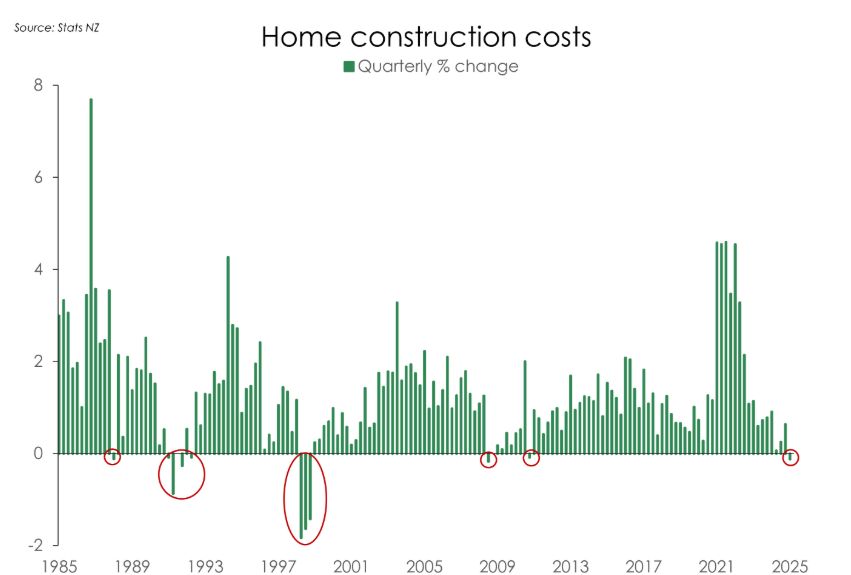

Charts of the Week: Cheaper construction costs

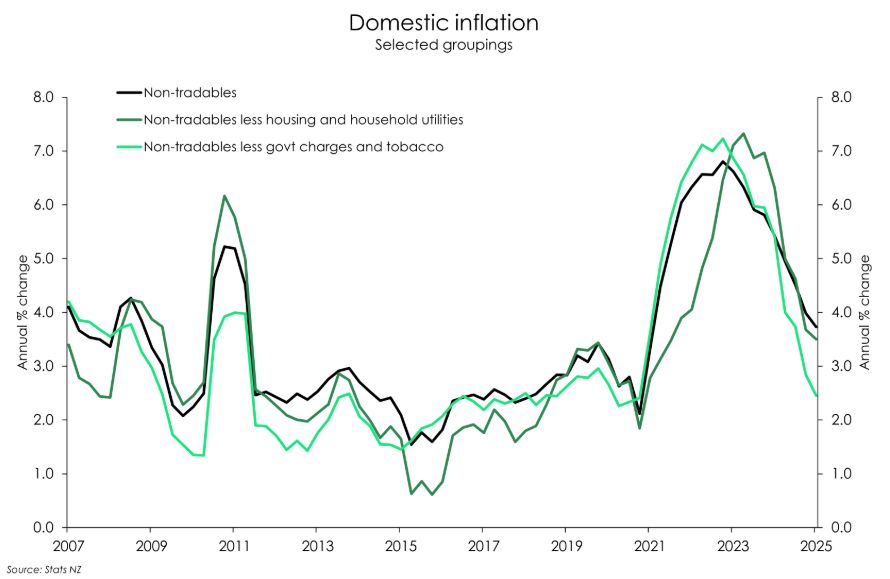

Domestic inflation continues its (slow) move south. Annual non-tradables inflation pierced below 4% for the first time in four years to 3.7%. Within that, housing-related inflation was significantly weak. Building costs fell 0.1%qoq – the first decline since March 2011. And over the year, costs are up just 0.8% - that’s the lowest we’ve seen since the GFC (Dec 2009). Those in the industry cited competitor price-matching as well as lower component and fitting costs as reasons for price weakness. Falling materials costs, like steel, match the anecdotes were hearing from developers. And wages within the industry have softened also. There’s less work. Such pricing weakness was flagged in the latest NZIER QSBO report, where the building sector reported the biggest fall in pricing – from a net 3% raising their prices to a net 35% decreasing their prices.

In some good news for builders, developers, and home DIYers, the Govt has given the “green light” on selected overseas building products that would otherwise have not been permitted for use in NZ – from plasterboard to external doors. While construction costs are now increasing at a more modest pace, it is still around 50% more expensive to build compared to pre-covid. The looser restrictions should see greater competition and better price regulation. 20% increases in building costs should (hopefully) be a thing of the past.

Domestic inflation has fallen some way from its 6.8% peak in 2023, but it is still sitting high above the long-term average (~3%). And that’s despite such a weak domestic economy. Such persistence is due to the lingering strength in administered prices. Council rates and insurance costs are running well above historic averages, up 12.2%yoy and 6%yoy, respectively. And households are now contending with high electricity charges, climbing to 9.1%yoy. If we exclude housing-related inflation, domestic inflation prints at 3.5% - the lowest since December 2021. Given excess capacity still sloshing in the economy, domestic inflation should continue to head lower. But the pace of easing is being dictated by factors largely outside of the RBNZ’s control. That’s a frustration.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention