Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

A Better Headline Masks Dicier Details. The Kiwi Labour Market Deteriorates Further

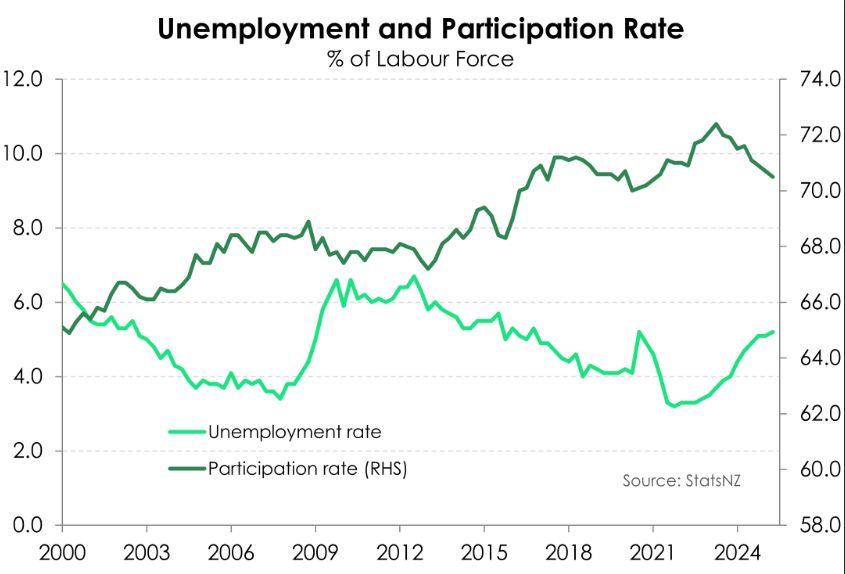

- The Kiwi unemployment rate rose to 5.2% from 5.1%. It would have been higher if not for the steeper-than-expected slide in the participation rate. People are leaving the labour market, and it’s keeping a lid on the unemployment rate. That in itself is a sign of a weak labour market.

- The moderation in wage inflation continued. Annual wage growth slowed to 2.3%, down from 2.5% - the weakest in four years. Weaker wage inflation is helping to drive further easing in domestic inflation. It’s that famous Phillips curve.

- Today’s data reinforces the need for further monetary policy easing. Downside risks to medium-term inflation are growing given the soft labour market and dimming global outlook. We expect the RBNZ to cut the cash rate by 25bps at the August meeting. And they’ll need to go to 2.5% eventually.

At first glance, today’s employment report looked a bit better than expected, but it wasn’t. The unemployment rate came in at 5.2%, slightly below our forecast of 5.3%. It’s the big drop in labour force participation that’s keeping a lid on the unemployment rate. From (a downwardly revised) 70.7% to 70.5%, the participation rate has dropped to a four-year low. That in itself is a sign of a weak labour market. People are leaving the labour market because it is simply not as attractive as it once was. In fact, the labour force shrank over the year. That doesn’t happen often. The 0.4% decline is the deepest since March 2013. Labour demand is soft. The June quarter recorded a 0.1% decline in employment. And the 0.1% gain in the March quarter was revised to flat. On an annual basis, employment growth is running at the weakest rates since the GFC.

The underutilisation rate – a broader measure of untapped labour market capacity – rose to 12.8%, the highest since September 2020. There’s clearly significant slack within the Kiwi labour market.

Hours worked fell 1% over the quarter, marking the sixth straight quarterly decline. That’s a concern for how June quarter GDP might unfold. High frequency economic indicators have already been flagging a marked slowdown, potentially a contraction, in activity. This statistic adds to the list.

Declining hours is being met with easing wage pressures. More and more workers are receiving smaller and smaller pay rises. For example, the number of workers receiving a pay rise above 2% but below 3% has been steadily increasing for the last two years. And the wage bill (private sector Labour Cost Index) rose 2.3% over the year – the lowest in four years. That’s quite the drop from the 4.5% peak. That’s indicative of a weak economy.

Overall, today’s report presents a weaker labour market than the RBNZ had expected back in May. The unemployment rate may have been in line with their forecast, but only because of a deeper slide in the participation rate. Labour demand is clearly weaker than the 0.2% gain the RBNZ had forecast in May. The door remains open for a 25bps rate cut later this month. And the cash rate will need to go to 2.5%, eventually.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention