Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

The Pieces Have Fallen Into Place. Lower Rates Are Needed

- The stars, or shall we say data, have aligned for a rate cut by the RBNZ next week. We’ve now had all the key data releases in the lead up to the Reserve Bank's upcoming meeting. And all of them have supported the case for lower rates.

- Adding to an already tall pile of evidence that our economy needs stimulus, was the June quarter Kiwi jobs report. Unemployment lifted to a five-year high. And it would have been higher if not for the steeper-than-expected slide in the participation rate. Meanwhile, details under the headline rate portray an even weaker reality.

- Inflation expectations remain comfortably within the RBNZ’s 1-3% target band. The RBNZ should feel comfortable looking through this near-term rise in inflation. See our COTW for more.

Here’s our take on current events

Since the RBNZ paused in July there were three key data releases we knew would be carefully picked apart before the August meeting. The first was June quarter Kiwi inflation, which showed weak underlying price pressures, despite a lift in the headline rate to 2.7%. Then last week, we saw the remaining two key data prints: the Kiwi labour market report and the RBNZ’s survey of inflation expectations. Both of which support the case for further rate cuts. A 25bps cut next week to 3%, followed by an eventual move to 2.5%.

At first glance, the June jobs report looked a bit better than expected. But under the microscope, the Kiwi labour market is clearly soft. The unemployment rate came in at 5.2%, slightly below our forecast of 5.3%. But it’s the deeper slide in labour force participation that kept a lid on the unemployment rate. From (a downwardly revised) 70.7% to 70.5%, the participation rate has dropped to a four-year low. That in itself is a sign of a weak labour market. People are leaving the labour market because it is simply not as attractive as it once was. In fact, the labour force shrank over the year. That doesn’t happen often. The 0.4% decline is the deepest since March 2013. Labour demand is soft. The June quarter recorded a 0.1% decline in employment. And the 0.1% gain in the March quarter was revised to flat. On an annual basis, employment growth is running at the weakest rates since the GFC.

The underutilisation rate – a broader measure of untapped labour market capacity – rose to 12.8%, the highest since September 2020. There’s clearly significant slack within the Kiwi labour market.

Hours worked fell 1% over the quarter, marking the sixth straight quarterly decline. That’s a concern for how June quarter GDP might unfold. High frequency economic indicators have already been flagging a marked slowdown, potentially a contraction, in activity. This statistic adds to the list.

Declining hours is being met with easing wage pressures. More and more workers are receiving smaller and smaller pay rises. For example, the number of workers receiving a pay rise above 2% but below 3% has been steadily increasing for the last two years. And the wage bill (private sector Labour Cost Index) rose 2.3% over the year – the lowest in four years. That’s quite the drop from the 4.5% peak. That’s indicative of a weak economy.

Overall, the labour market is weaker than the RBNZ had expected back in May. The unemployment rate may have been in line with their forecast, but only because of the drop in the participation rate. Labour demand is clearly weaker than the 0.2% gain the RBNZ had forecast in May. Alongside contained and anchored inflation expectations (see COTW), the door remains open for a 25bps rate cut later this month. And the cash rate will need to go to 2.5%, eventually.

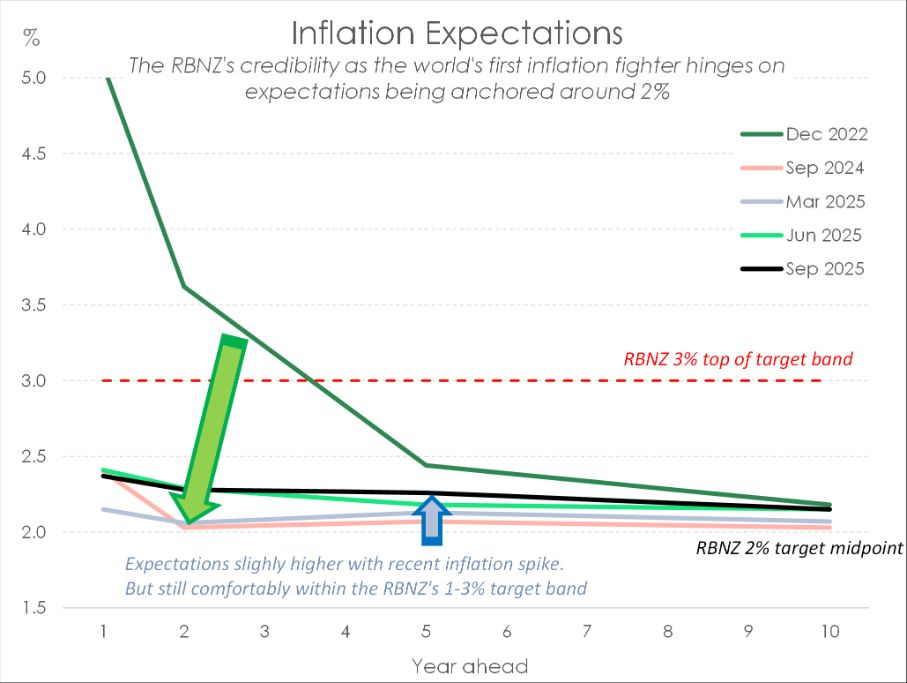

Chart of the Week: Inflation expectations holding steady as she goes

Inflation expectations tend to follow actual inflation. So when we saw the headline rate accelerate from 2.5% to 2.7% over the June quarter, it was almost a given that we’d see a lift across inflation expectations. That wouldn’t have gone down too well at the RBNZ. Remember the 5-1vote at the May MPS? The argument to hold rates was grounded in concerns around rising inflation expectations. Thankfully, the latest round of the RBNZ’s survey of inflation expectations showed expectations comfortably contained within the RBNZ’s 1-3% target band.

In fact, inflation expectations for 1-year ahead dropped 4bps to 2.37%. The 2-year ahead measure – key horizon to consider for setting monetary policy – also dropped by 1bp to 2.28%. We like to see that. And we’re sure the RBNZ was pleased with the move lower too. Especially in the face of the temporary inflation spike we’re seeing right now.

Further out, there was a bit more movement in the 5-year ahead measure, up 8bps to 2.26%. While the 10-year ahead measure remain unchanged at 2.15%. On balance, all measures remain comfortably within the RBNZ’s target band. It confirms that there remains little risk this bout of high inflation will persist. As we’ve seen in NZIER’s Quarterly Survey of Business Opinion, firm’s pricing power is evaporating. And spare capacity in our deteriorating labour market is another disinflationary force. The bigger risk continues to be inflation undershooting the 2% midpoint over the medium term. Hence our call for a lower more stimulatory 2.5% cash rate.

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction