Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

There’s No Doubt The RBNZ Should Cut. And They Will. But There Is Doubt That They Will Do Enough.

- The RBNZ’s policy decision is approaching. Will they cut? Yes. Will they signal another cut to come? Yes. Will it be enough? Not quite. There’s no doubt that the Kiwi economy needs support. There’s no doubt the RBNZ needs to stimulate. But there is doubt that they will deliver? They should.

- The weakness in the economy demands stimulus. With all the risks offshore, and the pain still felt onshore, there's a good argument to be made for taking policy into stimulatory territory asap. An argument that is growing in support.

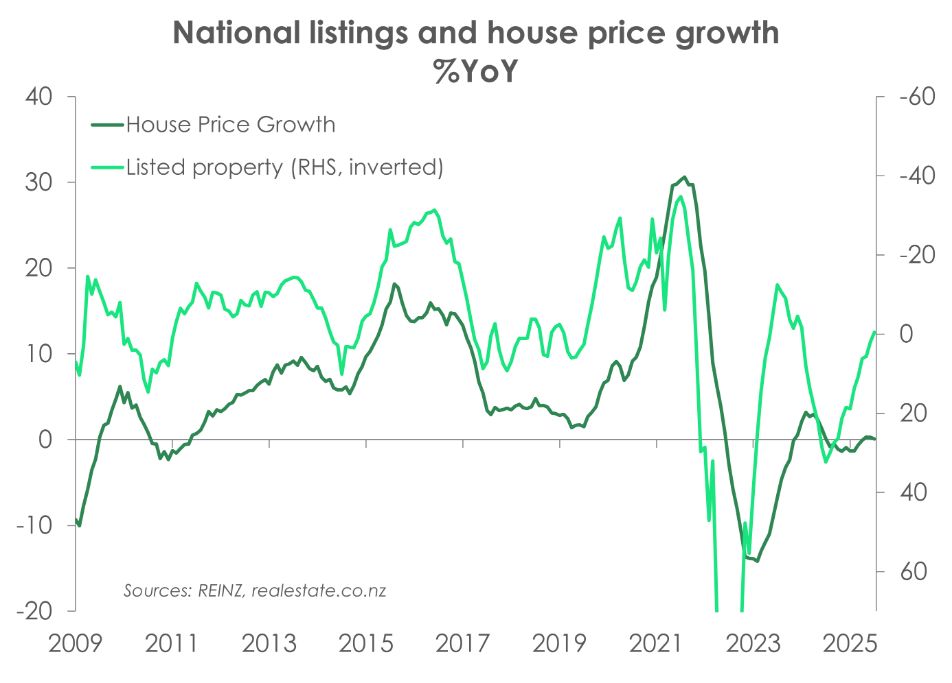

- Our COTW looks at the latest REINZ housing data, which much like the current season, feels stuck in an endless winter. House prices have dipped for a second month in a row. And activity remains subdued.

Here’s our take on current events

From the RBNZ’s perspective, this week’s decision, with updated forecasts, sets the scene for the next 3 months (see our full preview here). And it will help set the trading ranges for financial markets. The economic data and developments since the last MPS have strengthened the case for a more “go for growth” focussed RBNZ. The RBNZ will have removed the restrictiveness of monetary policy… but that is not enough.

Wednesday’s decision by the RBNZ should set a policy path that is right for the recovery. We need a stimulatory monetary policy setting. So, what do we mean?

Estimates of a “neutral” setting – when policy is not hurting but certainly not helping – range from 2.5-3.5%, with 3% being roughly right. So, a cash rate of 3% isn’t stimulatory, and it isn’t encouraging excessive behaviour or inflation. But we need a stimulatory rate if we’re going to encourage businesses to take on risk – by either investing or hiring. And we need a stimulatory rate if we’re going to see embattled households boost discretionary spend. 2.5% is closer to what we need. And the risks are towards a 2% cash rate, not 3%, in our opinion.

That said, the RBNZ has proven to be reluctant, all the way down. A more decisive RBNZ would be viewed positively across the road (Terrace), given the difficulty the Government has in balancing the books. And a more decisive RBNZ would be viewed positively by Kiwi business owners, property investors, and most households with debt.

Unfortunately, it is never straight forward. And there are three likely scenarios that could play out on Wednesday:

The first scenario is the one the RBNZ may find the easiest to deliver. The RBNZ delivers a 25bp cut and leaves the OCR track at 2.85% or thereabouts. This would not go down well. Wholesale market traders would push interest rates higher, again frustrated by the RBNZ’s reluctance in getting the job done. The OCR endpoint priced into the OIS strip would lift from ~2.71% towards 2.85-2.9%. Unhelpful. The pivotal 2-year swap (interest) rate would rise from around 3.06% now to 3.15% (about 15bps). Mortgage rates would barely move… although they had been lowered a little in response to the recent fall in wholesale rates. But the risk then turns towards a slight lift in mortgage rates. Very unhelpful. The Kiwi currency would pop higher, towards 60.50c and possibly 61c in time. Not what exporters want to see with an intrusive 15% tariff from the US.

The second scenario is what we think they will do, with least regret and least resistance. A 25bp cut accompanied by a lower OCR track to 2.7% (or close to). Currently, most economists sit between a low of 2.5% (Kiwibank) and a high of 3%. This scenario will push most economist forecasts to a lower 2.25-2.75% range. Such a move would support current market pricing of a 2.71% terminal rate. The 2-year swap rate should ease back to 3%, supporting current mortgage rates. The short dated mortgage rates may ease a little more, whereas the 3-5 year rates may not move much at all. The Kiwi currency would probably stay around 60c. It’s a move that supports markets, but does not stimulate.

The third scenario is ‘go for growth’ and generate greenshoots. A Doveish Hawkesby should put a 2.5% cash rate firmly on the table. The shock without Orr would see wholesale rates continue their downward spiral. The 2-year swap rate would ease towards 2.8%. All mortgage rates would likely be lowered, as needed. And the Kiwi currency would fall towards 58c, giving a bit of relief to exporters, and helping to offset the US tariffs.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention