Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

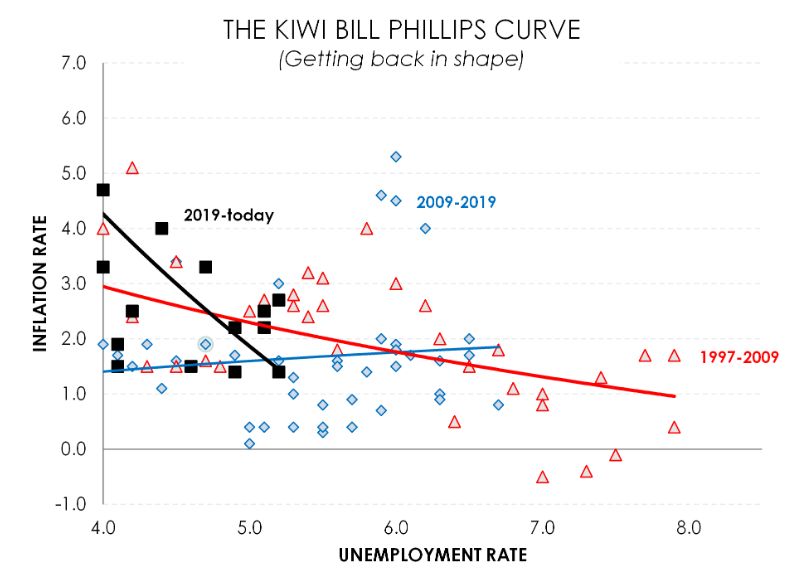

It’s All About Unemployment And Inflation: Phillips Said It Best

- All eyes were on the US jobs market report last week. It received a bit more attention following last month’s claims by Trump that the data were “rigged” and “wrong”. And he fired the Bureau Commissioner. Well, it was weak, again. Although the July figures were revised up, funnily enough, the others were revised down, and the headline print for August was soft. So who does he fire now?

- The weak US economy supports calls for lower US interest rates. And they will come. Just as further rate cuts elsewhere, and here, will come. Although the Aussie’s are not as convinced. Consumer spending is already picking up with limited rate cuts to date. It is the lucky country.

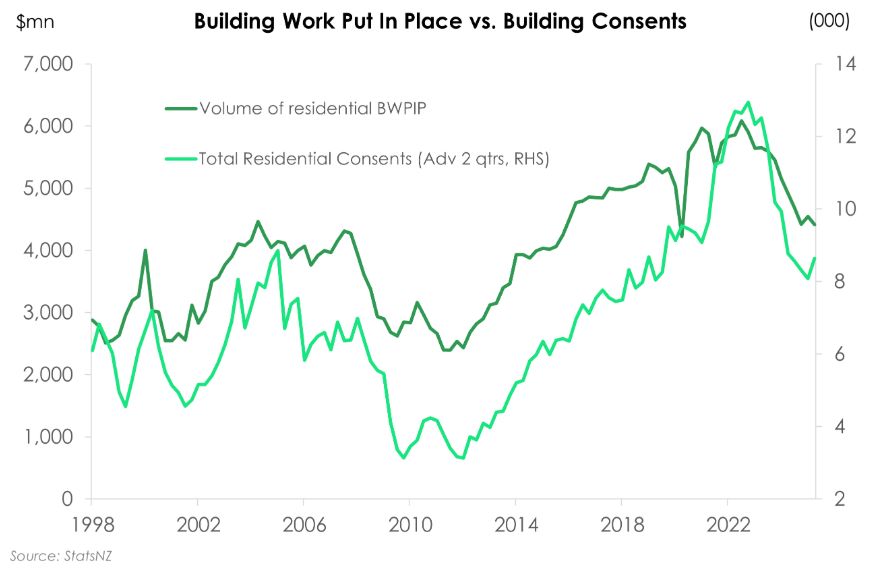

- Our COTW looks at construction activity over the June quarter. With the housing market still depressed and interest rates not yet at enticing levels, construction activity continues to decline. Though lower rates on the horizon and a warmer housing market into spring should help the industry find its feet again.

Here’s our take on current events

It's all about the Phillips curve. Famous Kiwi economist Bill Phillips put it best. There’s a relationship between rising unemployment, and inflation. And unemployment rates are rising. Market traders waited eagerly last week for the latest US non-farm payrolls report, for August. July’s shockingly weak print led Trump to fire the Chief of the Labor Statistics Bureau… Trump claimed the figures were “rigged” as they reflected poorly on his administration. By no surprise, new head of labour statistics or not, August’s data offered no reprieve. The US labour market is weakening.

Following July’s weakness, the bar for jobs growth was set low with just 75k jobs expected in August. And even that proved too high. Only 22,000 jobs were added. And revisions to prior months showed the US labour market was weaker than previously thought. July’s “rigged” figures were revised up slightly by 6,000 jobs to a still weak 79k. But June’s data were revised down sharply, showing a net loss of 13,000 jobs… the first monthly decline since 2020.

The US unemployment rate rose to 4.3% - the highest level since 2021. Hiring has stalled, and spare capacity is building. And the slack is already feeding through to wages, which are cooling faster than expected. Average hourly earnings grew just 3.7% over the year, down from 3.9%, undershooting forecasts and reinforcing the narrative of a softening labour market.

Overall, the weak payrolls report solidified expectations for a 25bps rate cut from the Fed next week. Markets had priced in a 75–80% chance of a cut before the payrolls release, which has now moved to be fully priced. And there’s even a small probability being priced in for a larger 50bps cut. However, higher producer and consumer price inflation data out this week is expected to cool talks of a 50bps rate cut.

Closer to home, the Australian economy grew 0.6% over the June quarter, after a slow start to the year. The Aussie economy is 1.8% bigger over the year. A 0.9% increase in consumer spending underpinned the rebound. It was the strongest increase since late 2022. For a while, households have held back spending in a cost-of-living crisis. But with the RBA’s cutting cycle and falling inflation, real disposable incomes are growing and encouraging spending. The usual holidays like ANZAC Day and Easter, as well as better weather conditions helped boost activity. Other key expenditure components, however, remain subdued. Business investment declined in the quarter with capex intentions suggesting the softness will continue.

Following the data, RBA Governor Michelle Bullock cautioned future rate cuts. If consumer spending continues to rise rapidly, then “there may not be many interest rate declines yet to come. But it depends”. The market trimmed the amount of easing to 21bps by November, compared to around 26bps ahead of the data. In the land of currency, the Kiwi Aussie cross (NZDAUD) continued on its glide path lower. The Kiwi Aussie cross (NZDAUD) continued to glide lower, hitting a low of 89.69.

At home it’s been a bit quieter with just some partial GDP data out over the week. Building activity, intrinsically tied to the housing market, remained weak over the June quarter (see our COTW for more). But on a brighter note, despite the mass uncertainty and waves of tariff announcements over the June quarter, our trade sector has held up well. Total exports fell just over 2% in the June quarter compared to March, though March was an exceptionally strong base. And over the year, our Kiwi exports are still up 10%. Even better, our terms of trade rose 4.1% over the quarter—more than double the consensus forecast of 1.9%. Export prices for goods edged up 0.2%, while import prices fell 3.7%.

Chart of the Week: Construction still finding its footing

With the housing market stuck in its endless 2-year winter, and interest rates not yet at enticing levels, the construction sector continues to struggle. Data from StatsNZ last week showed total building activity fell 1.8% over the June quarter, nearly double the contraction that had been expected.

Falls in activity came from both the residential and non-residential sector where building work declined 2.9% and 0.4% respectively. Residential building consents - which typically lead actual construction activity - have started to lift off their lows. However, they remain more than 30% below their COVID-era highs, underscoring the significant depth of the downturn seen across the industry over the past few years.

For now the construction sector is still in a period of stabilisation rather than recovery. However, as more rate relief filters through and the housing market begins to stir with the arrival of spring, the construction sector should gradually regain some momentum.

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction