Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

The RBNZ Need To Do More. And More We Will Get

- We’ve changed our call. We now expect a 50bps cut in October, followed by a 25bps cut in November. The cash rate should end the year at 2.25%. Why? because it has become crystal clear that the Kiwi economy is not recovering. In the wise words of Nike, “Just do it”.

- We need to have a serious discussion around a further move to 2%. It will depend on how the economy evolves over summer. We think there's about a 50/50 chance that the economy may require further support. We need the RBNZ’s foot firmly on the accelerator.

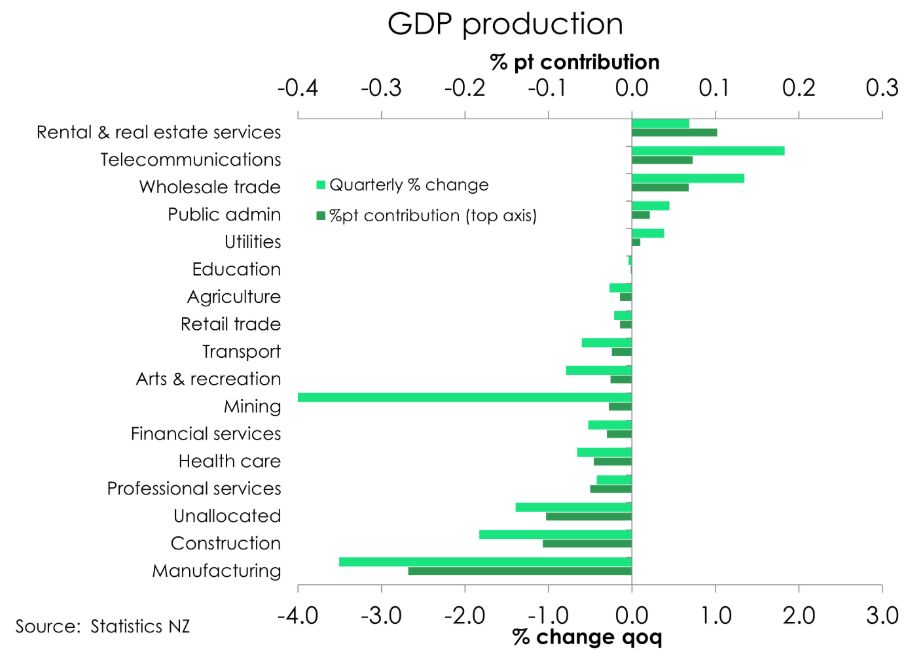

- Our COTW looks at the details of the Kiwi GDP numbers. Weakness was broad based with 10 out of the 16 industries in decline. It’s simply not what you’d expect a year after the severe recession. We should be recovering by now.

Here’s our take on current events

It has become crystal clear that the Kiwi economy is not recovering. The Reserve Bank need to do more. And more we will get. We now expect a 50bps cut in October, followed by a 25bps cut in November. The cash rate should end the year at 2.25%. From there, we think there’s about a 50/50 chance of a further move to 2% in February. It will depend on how the data and recovery plays out. This summer will be an important time for data watching. Will the housing market pick up? Will consumer confidence lift into consumption? And will business confidence translate into activity? It will all feed into the February decision. We hope it will.

Our change in call stems from last week’s shocking GDP figures. The Kiwi economy slammed into reverse, contracting 0.9% over the June quarter. This compares to our and the Reserve Banks forecast of a 0.3% contraction.

It’s saddening to see an economy still contracting after last year’s deep and destructive recession. We fell into a hole last year. And we’ve only dug ourselves deeper. Over the year, the economy has shrunk a further 0.6%. And as usual, things are even bleaker on a per capita basis. Economic growth on a per person basis contracted 1.1% over the quarter alone and is down 1.3% from June last year.

Taken at face value the significant drop-in activity proves, once again, that the RBNZ has not yet delivered the appropriate monetary policy setting. We have been advocating for a 2.5% cash rate for over 2 years. And now it is crystal clear that current monetary policy settings, with a 3% cash rate, are not enough. We are advocating and expecting a 50bp move in October. Get it done. Get to 2.5% asap. No more time for mucking around. Then get to 2.25% by year end. And keep your mind open. A further move to 2% remains a possibility.

A reminder to our readers, the RBNZ’s August rate decision came to a historic 4-2 vote, with two committee members favouring a 50bps cut. The seed has already been planted. And the recent flow of weak, uninspiring economic data could very well be the water that sees the dissenting view grow to become the consensus view. Plus, the data follows recent comments from Hawkesby that “While our central projection for the OCR is to fall to around 2.5% by the end of the year, that could occur faster or slower.” Well, it’s obviously going to have to be faster and deeper.

It’s time for leadership out of the RBNZ. And we’re due to learn of the new RBNZ Governor. Who we hope will focus on transparency and credibility.

Financial markets were also kept busy by a trio of central bank announcements. The US Federal Reserve and Bank of Canada have both returned to the cutting party. As widely anticipated, the FOMC cut rates for the first time this year. The 25bps cut takes the upper bound of the fed funds rate to 4.25%. There was a single dissent by new Governor Stephen Miran, who favoured a 50bps cut. The updated dot plot shows another 50bps of cuts this year, which was more than expected. Markets initially interpreted that as quite dovish, triggering a rally in bonds. But cool, calm and collected comments from Powell that the Fed are in no rush to cut rates, tempered the rally. All in all, there were some pretty whipsaw moves in markets on the day.

North of the border, the Bank of Canda cut to 2.5% after holding since April. The BoC’s return easing follows concerns that US-imposed tariffs are slowing growth and hiring in the Land of the Maple Leaf. There was no forward guidance but the market is still pricing in about 20bps of easing by the end of the year.

Finally, across the pond, the Bank of England voted 7-2 to hold the bank rate at 4%. They’re keeping a watchful eye on inflation. Policy guidance remains the same, with Governor Bailey noting “I continue to think that there will be some further reductions, but I think the timing and scale of those is more uncertain now”. The BoE also announced a slowing of the pace of QT – quantitative tightening – amid recent volatility in the gilt market. Through a combination of sales and maturing debt, the BoE will reduce its balance sheet by £70bn pounds per annum, down from £100bn.

Chart of the Week: Broad based weakness

Overall, the 0.9% fall in activity over the June quarter was broad-based with falls in output across 10 out of the 16 recorded industries. And by high level sectors, two of the three sectors, the goods producing and primary sector, recorded quarterly declines. While the services industry remained flat.

The goods producing sector was the biggest drag on the economy. Contracting 2.3% overall, a 3.5% and 1.8% decline across manufacturing and construction weighed heavily on the sector. Despite having seen a lift in activity over the start of the year, falls across both industries came with little surprise. For construction, the still subdued housing market alongside unenticing interest rates has done little to incentivise activity across the industry. Indeed, the latest REINZ data released last week showed house prices have risen just 0.4% since the Reserve Bank started cutting rates last year. While since correcting 18% lower between late 2021 to mid-2023, house prices are up just 1.5%. And it’s these lacking gains which continue to weigh on demand and momentum across the construction industry.

Similarly, the strength in manufacturing at the start of the year quickly evaporated over the June quarter. Weak business confidence and tariff uncertainty weighed heavily on new orders and overall demand across the sector. Manufacturing for transport and machinery equipment plunged 6.2%, while food and beverage manufacturing declined 2.2%, driven by a 1.2% drop in export volumes - particularly in dairy and meat.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention