Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

The Economy Still Needs Economic Shock Treatment (EST). Another Cut Will Help

- The RBNZ’s final monetary policy decision for the year is fast approaching. A 25bps cut is widely expected. The focus is acutely on what the RBNZ will say and signal for next year.

- The recovery remains fragile. Greenshoots are emerging but are few and far between. We hope a 2.25% cash rate will be enough for activity to spread. But we may need more.

- The OCR track will have to be lowered. And we'd expect a lower terminal rate with the RBNZ keeping the door open to more easing. See our COTW for more.

Here’s our take on current events

The RBNZ will take the stage for the last time this year on Wednesday (see our full preview here). We’re expecting a 25bps cut to bring the cash rate down to 2.25%. The meeting will also mark Christian Hawkesby’s swansong as Governor of the RBNZ. Hawkesby passes the reins to Dr Anna Breman on December 1st. Though it’s not until February next year that she will make her mark on monetary policy.

A cut to 2.25% this week is perfectly priced by markets and requires little justification. The Kiwi economy still needs more support. Yes, the RBNZ has delivered a significant amount of easing. 300bps to be exact. But for the majority of this year, the cash rate remained at restrictive levels. It is only after the cut to 2.5% in October that policy moved beyond neutral ground and into more stimulatory territory.

We had long advocated for such a move to 2.5%. But the move came too little too late from the RBNZ. And the delay has cost us. The recovery we anticipated for this year stalled, activity lost momentum and Kiwi households and businesses have suffered further. All of which has put the Reserve Bank in a position of needing to do even more. They didn’t do enough, the economy stalled again, and now they’re having to do more to mop up the mess.

So why not another 50bp move? Why not, indeed. It’s certainly within the realms of possibility, and should be on the table for discussion by the RBNZ’s MPC. Another “surprise” 50bp move gets the cash rate to 2%, without the long wait until February’s decision. A 50bp move to 2% would clear the decks, and clean the slate for incoming Governor, Dr Anna Breman. The RBNZ’s mistakes over the past 2 years have been centred around the inability to recognise the recession, and an inability to respond to the recession after it became painfully clear.

Is 2.25% really going to be enough? We’d hope so. Is 2% required? Maybe. But why not get us there, cut with confidence, to fuel confidence. It’s just the sort of shock treatment the economy needs. So even if we’re not calling for it, and hope with fingers crossed that a 2.25% cash rate will do enough… we certainly like the idea to getting another outsized move to crank things up a bit. And if it works, you just start hiking again, a little earlier than expected.

Beyond the cut itself, attention will fall to the RBNZ’s set of refreshed forecasts and OCR track. Given the RBNZ has already delivered more than the previous track implied, and in October the RBNZ signalled further ‘reductions’, we’d expect a lower terminal rate with the RBNZ keeping the door open to more easing. And it's the move in the track which will drive and set markets up for the remainder of the year. See our COTW for more on the OCR track.

Along with setting the scene for rates, Wednesday’s RBNZ decision is also pivotal for the NZD. The Kiwi dollar has tracked decisively lower over the past few weeks but got battered last week. Risk-off sentiment coupled with fading expectations of further Fed rate cuts this year, saw the Kiwi dollar drop below 56c – back to the April lows. Dovish remarks from the New York Fed President, John Williams, on Friday has since helped the Kiwi stage a slight recovery back above 56c. But in its fragile state, the key to any sustained move for the Kiwi remains on the messaging out of the RBNZ on Wednesday.

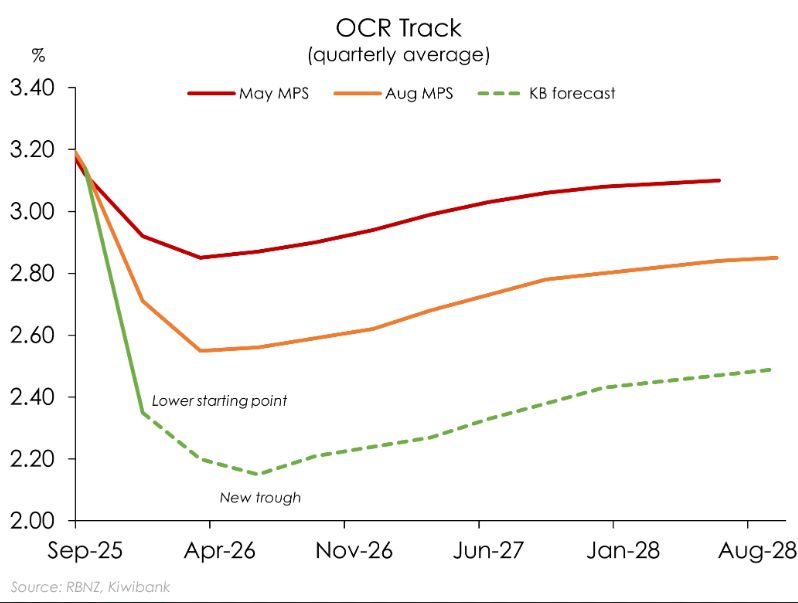

Charts of the Week: Keeping the door open to more

Accompanying the decision will be a fresh OCR track – the RBNZ’s forecast of the cash rate. We expect the track to be lowered (again) for two key reasons. First, the track must be lowered simply because of the October 50bps cut. The previous track troughed at 2.55%. The October cut took the cash rate below that to 2.5%. And this week’s cut would take it even lower. So naturally, the new track begins with a lower starting point. Secondly, let’s not forget the RBNZ’s forward guidance at the last meeting – “The Committee remains open to further reductions in the OCR”. The key word here being “reductions” – plural. With this grammatical nugget in mind, we’d expect the RBNZ to keep the door open to further rate cuts in 2026. We expect the terminal rate to drop to about 2.15%, implying a modest easing bias. Anything below that would signal firm intention to cut below 2.25%.

A track that troughs at 2.15% would largely be delivering on current market pricing. The OCR endpoint priced into the OIS strip currently sits at 2.12%. So 2.15% is not too different. The overall reaction in financial markets should be fairly muted.

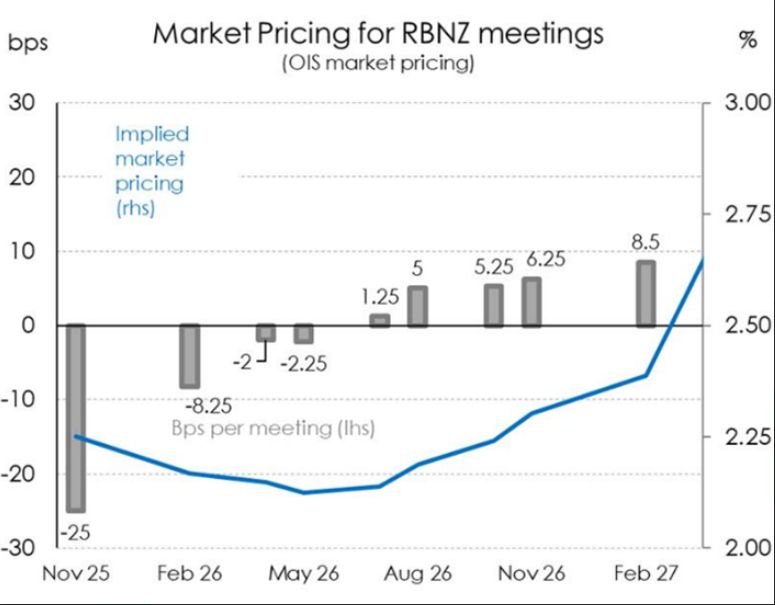

But if the RBNZ’s statement still highlights the need for optionality, and possible cuts (plural), then swap rates can fall back a bit. The 2yr swap rate has recently climbed to above 2.60%, unwinding the post-October MPR fall to be 15pts above the cycle-low. A dovish tone from the RBNZ could send rates back to those October lows. And arguably, that’s the right (needed) reaction to anchor retail rates at current levels, or even pull them lower. A track that signals a more aggressive easing bias in 2026 would certainly trigger a 10-20pt rally in wholesale interest rates, and the Kiwi dollar’s wings would be clipped as the RBNZ pulls even further away from its peers.

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction