Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Demand For Workers Is Improving, But We Have A Long Way To Go

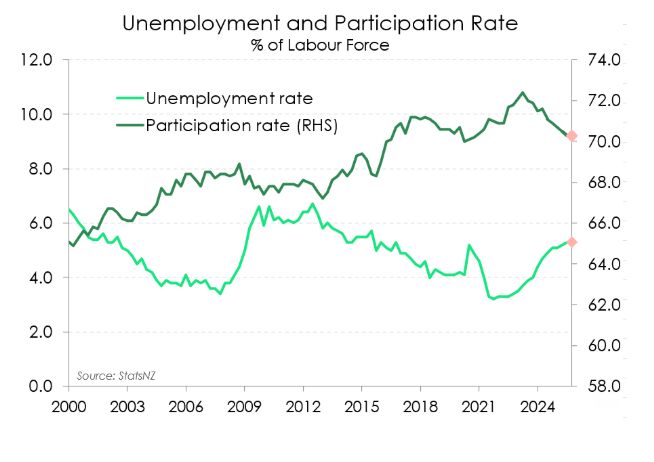

- With the Kiwi economy turning, the labour market is finding its feet and stabilising. Conditions remain soft, but the period of deterioration looks to be behind us. We expect the Kiwi unemployment rate held steady at 5.3% to close out 2025.

- There are growing signs that appetite for labour is improving. That’s good news. But for now those gains are only enough to absorb the growth in labour supply. And with sizeable spare capacity, we expect wage growth to remain subdued at 2.1%.

- While markets are increasingly pricing in the risk of rate hikes this year, we remain unconvinced. We need to see the labour market really turn, not just stabilise, to have confidence in the recovery and in order to see spare capacity get soaked up. We don’t think we’ll see that until the tail end of this year, maybe even early next year. And as such, we remain of the view that rate hikes remain a story for 2027.

Domestic data as of late has reflected an economy that is well and truly in recovery. Business sentiment has improved, and activity indicators are up. So, naturally with the release of Kiwi jobs data just around the corner, the question is, are we set for some more good news?

In a broad sense, we think we are. We expect next week’s labour market statistics from StatsNZ to reflect a jobs market that is stabilising. And that’s a welcome change from the softening we saw through much of the past year. Recent indicators suggest an improvement in labour demand and employment growth. The worst should be behind us. That said, labour market conditions are set to remain soft with a meaningful unwind in spare capacity still a while away yet. Because while our economic recovery may indeed be underway, the labour market tends to be the last indicator to turn.

Still, the December quarter should show the market levelling out. Glimpses of a stabilisation were already seen in the last jobs report for the September quarter. Total hours worked lifted for the first time in nearly two years. Meanwhile employment growth, flat over the quarter, had broken a year-long streak of quarterly declines. Since then, monthly filled jobs data has continued to suggest an improvement in the appetite for labour. Despite some volatility, filled job’s trended higher over the December quarter, up 0.2%. Such a lift however keeps total filled jobs around 1.8% below their early 2024 peak levels. 2026 should see further improvements. But it will still be more of a slow burn in job growth given the lagging nature of the labour market reflecting economic conditions from 9-12 months ago. Which no one needs reminding but wasn’t a great time

Our forecasts for next week are broadly in line with the RBNZ’s. Stronger readings across activity indicators, alongside last week’s hotterthanexpected inflation print, has however seen markets and commentators alike turn their attention to the possibility of rate hikes this year. While we do expect next week’s labourmarket release to show some improvement relative to recent outcomes, the economy still carries a meaningful degree of spare capacity. Spare capacity which will take time to be fully absorbed. We need to see the labour market really turn, not just stabilise, to have confidence in the recovery. We don’t think we’ll see that until the tail end of this year, maybe even early next year. And as such, we remain of the view that rate hikes remain a story for 2027.

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction