Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Gold And Silver Gains Warshed Away

- Fed vet and monetary hawk, Kevin Warsh has been nominated by President Trump to be the next Chair of the Federal Reserve. Warsh has softened his stance since 2024, but can a bird really change its feathers? Time will tell.

- Here at home, all eyes will be on the Kiwi jobs report on Wednesday. We expect the unemployment rate to hold steady at 5.3%. There are growing signs that appetite for labour is improving. That’s good news. But for now, those gains are only enough to absorb the growth in labour supply. And with sizeable spare capacity, we expect wage growth to remain subdued at 2.1%.

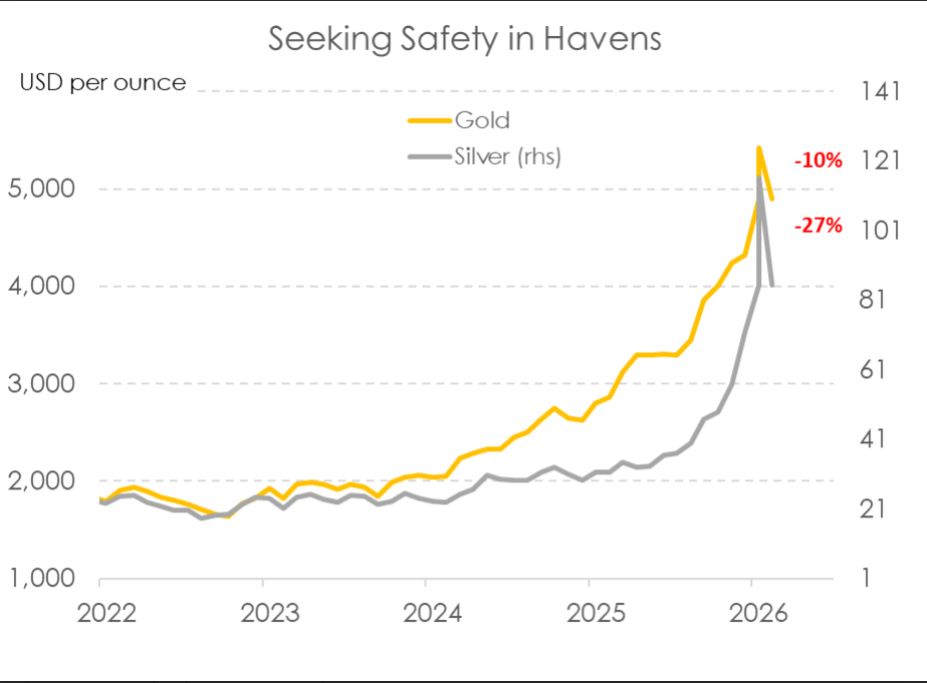

- Our COTW takes a look at the savage moves across precious metals. Gold and silver hit record highs just to come crashing back down around 48 hours later.

Here’s our take on current events

After months and months and months of waiting, President Trump announced his nomination for the next Fed Chair. And the battle of the Kevins has been won by Warsh. Kevin Warsh is a Fed vet, serving as a board member from 2006 to 2011. A critical period. At the time, and in many of his public comments since, he’s built out a reputation to be an inflation hawk. But his tone softened and he began to advocate for lower rates in November 2024. About the same time that Trump won the election. What a coincidence… Warsh’s newfound stance for lower rates however is at odds with his long-standing public argument for a smaller balance sheet. Either reducing or actively selling Treasury holdings only steepens the yield curve. And higher long-term rates would do little to lower mortgage rates. Will he prove to be just a hawk in dove’s clothing? Or has he fashioned himself a new set of tailfeathers? Time will tell. But coloured by Warsh’s past, markets see him as less supportive of deep rate cuts compared to the other Kevin (Hassett) that was in the running for the top job. The USD rallied big time, with Bloomberg’s DXY printing a near 10% rise since the news broke. Against the greenback, the Kiwi is floating back down to 60c after a stunning rise to the highest levels since last July.

Domestically this week our focus is on Stats NZ’s labour market statistics for the December quarter out on Wednesday. We’re expecting the report to reflect a jobs market that is broadly stabilising. And that’s a welcome change from the softening we saw through much of the past year (see our full preview here). Recent indicators suggest an improvement in labour demand and employment growth. The worst should be behind us. That said, labour market conditions are set to remain soft with a meaningful unwind in spare capacity still a while away yet. Because while our economic recovery may indeed be underway, the labour market tends to be the last indicator to turn.

Still, the December quarter should show the market levelling out. Glimpses of a stabilisation were already seen in the last jobs report for the September quarter. Total hours worked lifted for the first time in nearly two years. Meanwhile employment growth, flat over the quarter, had broken a year-long streak of quarterly declines. Since then, monthly filled jobs data has continued to suggest an improvement in the appetite for labour. Despite some volatility, filled job’s trended higher over the December quarter, up 0.2%. Such a lift however keeps total filled jobs around 1.8% below their early 2024 peak levels. 2026 should see further improvements. But it will still be more of a slow burn in job growth given the lagging nature of the labour market reflecting economic conditions from 9-12 months ago. Which no one needs reminding but wasn’t a great time.

There is a conceptual difference between Stats NZ’s filled jobs data and the Household Labour Force Survey (released on Wednesday). The former is drawn from tax data, and the latter is subject to sampling errors. Despite this, the monthly data does a good job in providing a steer on employment. Accordingly, we’ve pencilled in a 0.3% lift in employment growth over the quarter. Such a result would see employment flat on the year.

The recovery in labour demand is now likely just enough to keep pace with growing labour supply. We’ve pencilled in a 0.3% lift in the working age population over the December quarter. Which when put together, should see the unemployment rate hold steady at its 9-year high of 5.3%.

As always, movements in the unemployment rate on the day will be heavily dependent on changes to labour force participation. Much like the rest of the labour market though, we expect the participation rate to have also found some ground, likely holding steady at 70.3%.

In any case, considerable slack in the labour market remains. And even with improvements in labour demand, such slack is set to keep wage growth subdued. We expect to see a 0.5% quarterly rise in wages, keeping the annual rate steady at 2.1%.

Our forecasts for next week are broadly in line with the RBNZ’s. Stronger readings across activity indicators, alongside last week’s hotterthanexpected inflation print, has however seen markets and commentators alike turn their attention to the possibility of rate hikes this year. While we do expect next week’s labourmarket release to show some improvement relative to recent outcomes, the economy still carries a meaningful degree of spare capacity. Spare capacity which will take time to be fully absorbed. We need to see the labour market really turn, not just stabilise, to have confidence in the recovery. We don’t think we’ll see that until the tail end of this year, maybe even early next year. And as such, we remain of the view that rate hikes remain a story for 2027.

Charts of the Week: Buying safety can hurt, a lot. And it’s still hard to dump dollars.

We have seen some savage moves in financial markets. The Anti-Trump, get me out of dollars trade, had seen gold and silver smash record highs… going to levels that were once theoretical only. The price of gold and silver became exponential over the last year. At $2000 per ounce in 2023 and coming into 24, gold surged through $3000, $4000 and burst into the dizzying heights above $5000. A remarkable run. And you can't forget gold’s poorer cousin, silver. Silver skyrocketed 415% from 2024 to $117. Well, we’ve hit a pothole, to put it politely. Gold is down 10% from the $5427 peak… and the price of the more volatile silver plunged 27% to $85.

Is it the end of the run in precious metals? Probably not. Markets get ahead of themselves. Traders push prices as hard as they can for as long as they can. And then there’s a circuit breaker… a dose of reality. Kevin Warsh becoming the next US Fed chair has removed much of the fear within markets around diminished independence. SO, a run of buyers found wanting, and sellers coming to the party, flipped the market. Exhausted buyers, determined sellers, and the market struggled to clear. There’s a lot to be said about liquidity in a market… any market.

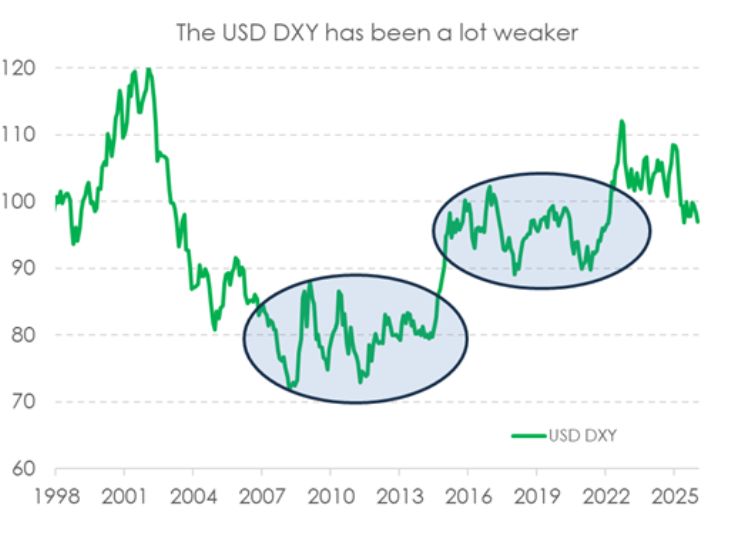

The most liquid bond market, is also the largest, and it’s the US. As we’ve pointed out before, we have seen a rebalancing of funds, not a dumping of dollars. The decline in the US dollar looks dramatic, on a 10-year chart, but it’s not. Go back further, the USD was much lower in the post-GFC period. If there had been a dumping of dollars, the US Treasury yields would be dramatically higher, and they are not. A 10-year Treasury at 4.25% is bang of expectations of fair growth, stable inflation, and a small term premium. No fear here… not yet

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction