Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Just What We Don’t Need… More Inflation

- The war in the Middle East has thrown yet another (huge) spanner in the works. Economists and analysts are scrambling to assess the likely damage from oil production cuts, global supplies, and ultimately… global growth. It’s not good.

- A spike in the petrol prices acts like a tax on the consumer. Household budgets are yet again, under strain. The cost-of-living crisis has been relentless, unforgiving and many years in the making. Consumption represents around 60% of our economy… and the petrol price spike (like a tax) will take its toll.

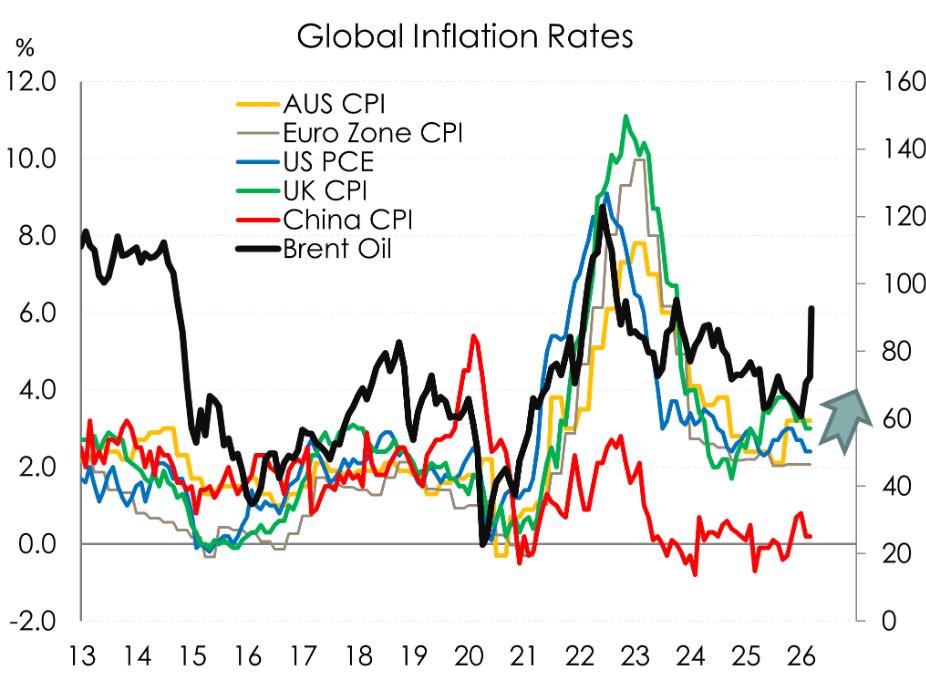

- Our COTW looks at the near 30% jump in Brent Crude over the last week. Still at just over $90USD a barrel (at time of writing) things are likely to get worse before they get better. It’s going to hurt at the pump. And beyond that, we’re keeping a watchful eye on supply chain pressures which will be next to come under pressure.

Here’s our take on current events

Well, there’s been no shortage of headlines to keep markets busy over the past week as the conflict in the Middle East has escalated (to put it politely). Yet despite the sheer scale of strikes and retaliation across over a dozen countries, markets have remained relatively calm.

Of course, there have been some moves in markets. But we’ve not seen the frenzied or violent reaction that other conflicts have induced.

The VIX, a measure of panic and volatility in markets, is still sitting at only half of what it was in the aftermath of Liberation Day last year. US Treasuries have sold off on fears of higher inflation, but not by much. The USD has strengthened a bit, with the DXY up ~1% over the last week. Traders have slipped back into treating the USD as the safe haven it has always been (recent anti-trump trades aside).

Bigger reactions, to no surprise, have been concentrated in oil markets. And even then, the move in Brent Crude above $90USD a barrel came slower than expected. (See our COTW for more).

After one volatile shock after another, it’s not surprising to see markets less reactive. However, with the conflict now spreading across several countries and no signs of deescalation, we don’t think this muted market backdrop will last.

Unfortunately, things are likely to get worse before they get better. We’re bracing for much higher volatility, with a bigger market reaction in the near term. Our hope that markets rebound quickly once the dust settles, as they did in 2022 following the Russia and Ukraine crisis period.

Contemplating the global fallout, the risks ahead are pronounced. With disruptions to oil, gas, and shipping, a lift in near term global and kiwi inflation is all but a done deal. But the downside risks to global and domestic growth cannot be ignored either. And ultimately, under this kind of supply shock induced inflation, it’s the damage to demand that is likely to dominate.

For households, higher petrol prices at the pump will just add to the cost-of-living crisis we keep hoping (and thinking) will end. We know increases in essentials, like petrol, act like a tax on household consumption. They squeeze disposable incomes and pull spending away from everywhere else. It’s something the Kiwi consumers and the broader economy has already been grappling with amid the surge in prices across household utilities. But now add to that higher prices at the pump, and Kiwi household budgets are about to become even more constrained, with areas of discretionary spending set to bear the brunt further.

Indeed, input costs are going to go up across the board for firms. But in an already fragile demand environment, not all businesses will be able to pass on the costs to consumers. It will be uneven. Sectors like retail and construction, which are amongst the weakest, will struggle to pass through higher costs.

Mixing together tighter margins, falling profitability, and a shell shock wave of uncertainty, businesses will be more likely to pull back on investment, hiring, and growth-oriented decisions… reinforcing a weaker growth environment.

So where does this all leave the path of interest rates then? Well for us the idea of rate hikes anytime soon looks more premature now than before the war. Yes, inflation will likely spike further in the near term. But central banks, the RBNZ included, will need to (and are supposed to) look through the near-term noise. Looking to the mediumterm instead, where monetary policy is targeted towards, the weakening growth outlook simply matters more. We suspect Central Banks, and the RBNZ in particular, may well have to tolerate higher inflation in the short run to avoid tightening into a slowing global economy.

Charts of the Week: Oh ship! There’s going to be pain at the pump.

Shipping traffic remains at a standstill at one of the world’s most strategically important oil choke points. Around a fifth of the worlds global oil and liquified gas passes through the narrow body of water between the Persian Gulf and Gulf of Oman, known as the Strait of Hormuz. And amid the escalating Middle Eastern conflict, passage across the strait has essentially come to a halt.

In response, oil prices have pushed higher, to no surprise. Brent Crude finished the week at $92.69 USD per barrel, jumping nearly 30% over the past week alone. Even so, the move was a touch slower than we might have expected. For most of the week, prices chopped around in the $80–$85 USD range—certainly higher than the low$70s we were trading at before the conflict, but still not particularly high in the context of broader oil market history.

But as the conflict has dragged on, we’ve seen a series of supplyside pressures emerge. The UAE, Kuwait, and Iraq have begun reducing production due to storage constraints. And China has halted oil exports… fuelling the push higher in the Brent Crude price.

And unfortunately, we don’t think it’s over yet. Things are likely to get worse before they get better. A move above $100 USD, and potentially into the $115–$120 USD range, similar to the levels reached during the RussiaUkraine crisis, looks increasingly plausible in the coming weeks. Our hope is that, as with 2022, prices retreat quickly once tensions ease.

For now though, it's going to hurt households at the pump. And to add to that inflation pressure, the Kiwi dollar has softened. The NZD has slipped from the high59s/low60s into the mid58s to mid59s. It’s not a dramatic fall, but with oil moving the way it has, every cent counts.

Beyond oil prices, attention will also turn to what happens with shipping costs. Because higher oil prices is one thing, but we’re also likely to see supplychain pressures build from rising shipping insurance premiums, longer transit routes as vessels avoid the conflict zone, and broader delays as global logistics networks adjust. That’s where we’ll feel a secondround bite of pain.

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students

University of Auckland: Research To Address Equity In STEM For Māori, Pacific And Female Students Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report

Stats NZ: Economic Impacts On New Zealand From Conflict In The Middle East – Report Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising

Advertising Standards Authority: ASA Annual Report 2025 - Platform-Neutral Regulation Keeps Pace With Digital Advertising Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction

Science Media Centre: Lead Pipes Banned For New Plumbing – Expert Reaction New Zealand Young Physicists Trust: Auckland To Host The ‘World Cup Of Physics’ In 2027; Search Begins For Student-Designed Tournament Logo

New Zealand Young Physicists Trust: Auckland To Host The ‘World Cup Of Physics’ In 2027; Search Begins For Student-Designed Tournament Logo