Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Disney Earnings: The Case For Keeping Hulu [Parrot Analytics]

Disney reports its first earnings of 2023 with on-again, off-again CEO Bob Iger back in the saddle as the company stands at a fundamental strategic crossroads.

Some of the questions facing this century-old institution include: whether to shutter linear channels, whether to license content to competitors to juice revenue, where to debut animated movies, what happens to ESPN, and what to do about Hulu.

To mention nothing of certain activist investor demands.

Despite all the outside noise, Parrot Analytics continues to view Disney as one of the best-positioned players to monetize the demand of its streaming and linear content, especially if it holds onto Hulu and buys out Comcast’s remaining stake in the platform.

Above all else, Disney remains the market leader in corporate demand share — which serves as a proxy for both long-term streaming success, and short-term licensing revenue potential.

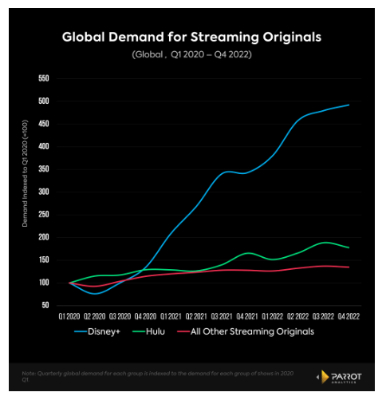

Demand for original series on Disney+ has driven Disney’s global streaming success over the last three years. Since early 2020, the global demand for Disney+ Originals has grown 380%. This has helped lead to a 390% increase in global subscribers over the same time, showing the key link between demand for original series and SVOD subscription growth.

However, as the US and global streaming markets approach a potential saturation point, subscriber retention will be equally critical to the long-term viability of today’s entertainment giants. This is where Hulu comes into play.

Hulu should be a key part of Disney’s strategy because it accounts for the most in-demand TV catalog of any other streaming service with US audiences, even beating out Netflix. Hulu is in second place in total catalog demand (TV & movies), and when combined with Disney+ would beat out both Netflix and a potential combo of HBO Max and Discovery+ for first place. This library content is exactly the kind of material that drives subscriber retention.

Furthermore, Hulu fills in the audience demographic gaps that Disney+ currently lacks: namely, older and more female audiences. The two platforms combined would create the ultimate four-quadrant service.

Regardless of whether Disney shifts Hulu into a tile on the Disney+ app or keeps it as a standalone piece of the Disney Bundle, the data is clear: demand for both exclusive and licensed content on Hulu provides immense short and long-term value to the Disney streaming and entertainment empire.

Demographic Data: Four-Quadrant Service

- Looking at the audience for both Disney+ and Hulu originals paints a clear picture of two complementary platforms that, combined, have something to offer everyone.

- While Disney+’s flagship Marvel and Star Wars series have audiences that skew younger and male, many of Hulu’s most in-demand originals appeal to an older and more female audience.

- Disney+ and Hulu combined create the proverbial ‘four-quadrant service’ that today’s entertainment leaders are chasing.

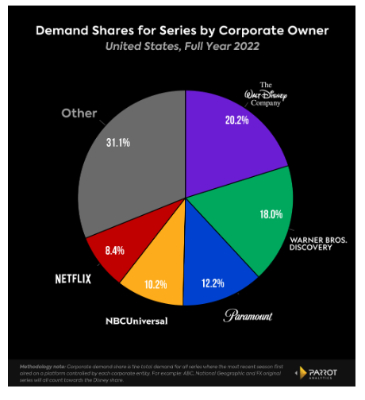

Corporate Demand Share: US, 2022

- Corporate demand share assesses the long-term viability of the top media companies as they look to consolidate their original content’s availability exclusively onto their own platforms.

- However, with Wall Street’s mandate to focus back on profits, this view of the entertainment landscape can also be used to assess which companies have the most valuable content to license out, rebooting one of the original revenue streams in the TV business. It can effectively help value a conglomerate’s legacy and library content in aggregate.

- As the leader in corporate demand share, Disney stands to earn the most additional revenue if and when it decides to sell off content to competitors.

- Disney was the only

legacy media conglomerate to increase its corporate demand

share in 2022. The changes for the top five US media

corporations from 2021 to 2022 were:

- Netflix: 7.7% to 8.4% (+0.7%)

- Disney: 20.1% to 20.2% (+0.1%)

- NBCUniversal: 10.8% to 10.2% (-0.6%)

- Warner Bros. Discovery: 18.9% (WarnerMedia + Discovery) to 18.0% (-0.9%)

- Paramount Global: 13.4% to 12.2% (-1.2%)

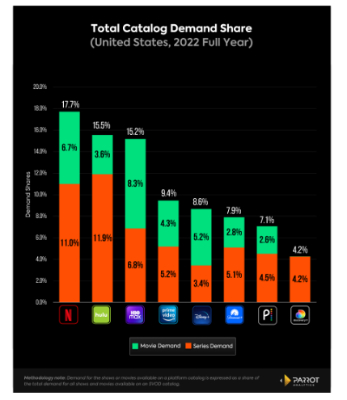

Total Catalog Demand Share (TV & Movies Combined): US, 2022

- As the global and US streaming market approach saturation levels, subscriber retention will be increasingly crucial to the future viability of major streaming services.

- Catalog content drives customer retention, and assessing the total catalog demand share (all TV and movies available on a platform) is a good indicator of which SVODs consumers are most likely to use as a default ‘streaming home.’

- This chart shows why Hulu is such a crucial asset to Disney’s streaming endgame: there is more demand for Hulu’s TV catalog than that of any other in the business, even Netflix.

- While Netflix currently leads this category, a hypothetical combo of Hulu and Disney+ would easily be number one (24.1%), well ahead of Netflix’s 17.7%, and even outpacing a potential HBO Max-Discovery+ combined SVOD at 19.4%.

Total Global Demand for Streaming Originals: Disney+ & Hulu vs All Others

Note: Jan-Mar 2020 to Oct-Dec 2022

- When it comes to demand for streaming original series — a key leading indicator of subscriber growth for SVODs — Disney+ has been the runaway leader in growth over the last three years.

- From the Jan-Mar 2020 quarter to Jul-Sep 2022 quarter, the total global demand for Disney+ Originals grew 379.8%. Over the same time period, Disney+’s global subscriber count increased from 33.5M to 164.2M, a 390.1% gain, showing the remarkable link between demand for original content and SVOD subscriber growth.

- Hulu Originals have grown at a more modest pace, up 78% since Jan-Mar 2020. That is still more than double the rate of growth for originals from all other streamers, 34.6%.

- On top of bridging the audience demographic gap, Hulu also has the ability to both bring in new subscribers with its originals, and keep them in the Disney streaming ecosystem with its vast catalog.

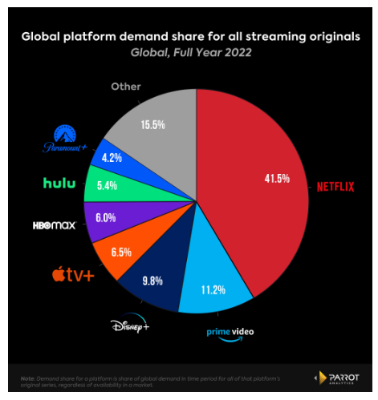

Global Streaming Original Demand Share Full Year 2022

- Disney+ has been the fastest-growing streamer in global demand for streaming originals two years in a row, growing from 3.6% in 2020 to 7.4% in 2021 to 9.8% in 2022.

- Over the last

three years, no streaming service has gained more global

market share than Disney+. From the Jan-Mar 2020

quarter (Apr-Jun 2020 for HBO Max) to Oct-Dec

2022:

- Disney+ grew from 4.2% to 10.2% (+6.0%)

- Apple TV+ grew from 3.8% to 6.4% (+2.6%)

- HBO Max grew from 3.3% to 4.8% (+1.5%)

- Paramount+ grew from 4.1% to 4.2% (+0.1%)

- Hulu shrank from 5.8% to 5.3% (-0.5%)

- Amazon Prime Video shrank from 11.8% to 11.1% (-0.7%)

- Netflix shrank from 55.7% to 39.6% (-16.1%)

- In the Oct-Dec 2022 quarter, Disney+ reached a new milestone with a record 10.2% global demand share. This was the first time it hit double digits, and the first time Disney+ has been within one point of Amazon Prime Video (11.1%) globally.

- Based on their current trajectories, Disney+ will likely leapfrog Amazon Prime Video for second place in global originals demand in 2023.

- This chart also shows the benefits of combining Hulu and Disney+. Together they would account for 15.2% of the global demand for original content, far ahead of Prime Video for second place behind Netflix.

Parrot Analytics

Global television demand measurement

Parrot Analytics is the leading global content demand analytics company for the multi-platform TV business. With the world's largest TV audience demand datasets, the company currently tracks more than 1.5B daily expressions of demand in over 100 languages from 200+ countries to reveal the content consumers engage with and watch the most across platforms.

As a trusted partner to some of the biggest media companies and content creators in the world, Parrot Analytics optimises content workflows in real time. The company's TV analytics products result in better production, distribution, acquisition and marketing decisions, as well as accelerated SVOD platform success.

Bill Bennett: Fixed Voice Rules Head For Deregulation

Bill Bennett: Fixed Voice Rules Head For Deregulation UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP

UN Department of Global Communications: United Nations Proposes New Global Dashboard To Measure Progress Beyond GDP Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman

Banking Ombudsman Scheme: Fraud Check Delays Well Worth The Inconvenience, Says Banking Ombudsman Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality

Asia Pacific AML: NZ’s Financial Crime Gap - Beyond The 'Number 8 Wire' Mentality Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows

Westpac New Zealand: Kiwi Households Adapting Despite Widespread Cost Pressure Concerns, Westpac Survey Shows University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention

University of Auckland: Kids’ Screen Use Linked To Long-Term Deficits In Self-Control And Attention